LB Takeaway | BYD and Li Auto price target raised by double digit, Lyft has 200% upside?

Citi maintains AMD's "neutral" rating, reduces price target by 13% to $96 from $110. Credit Suisse maintains Lyft's "outperform" rating, cuts price target by 17% to $50 from $60.

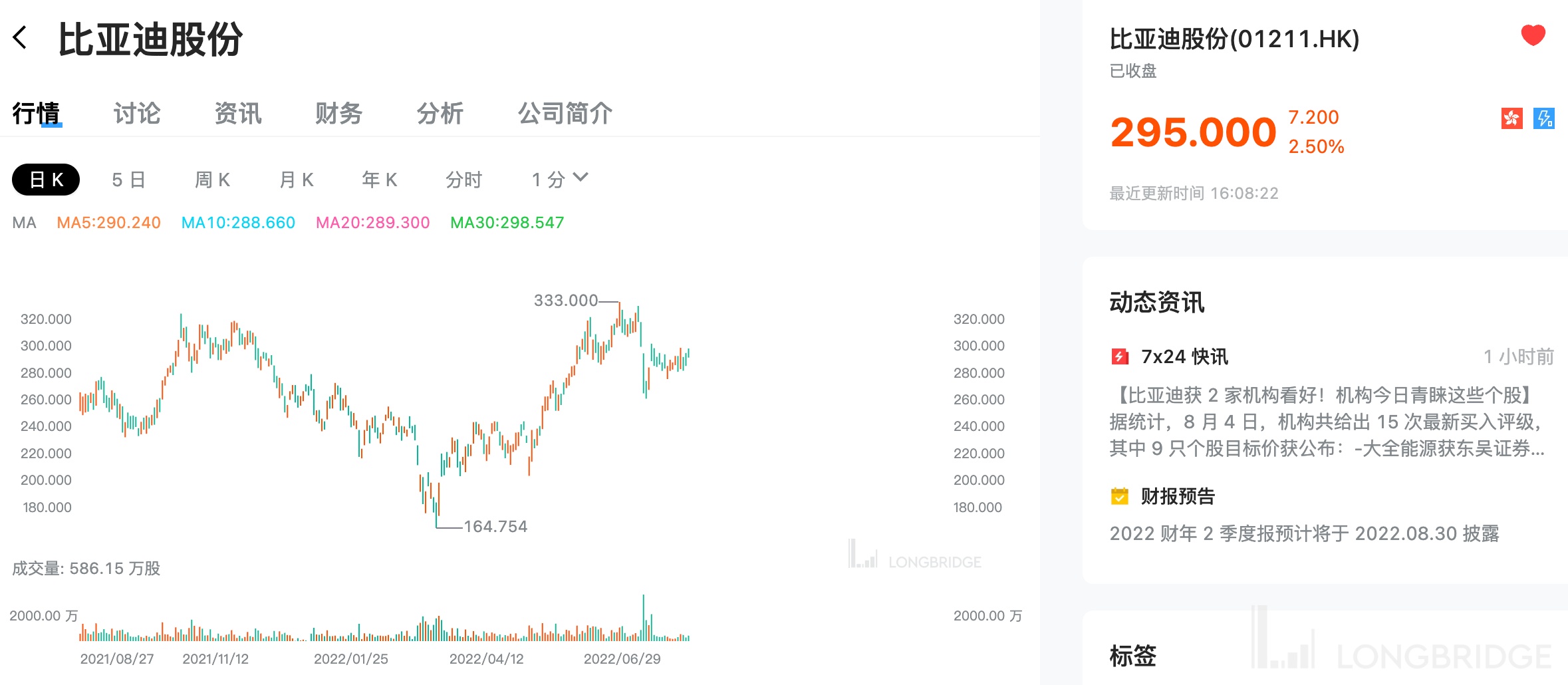

Citigroup: Reiterate "Buy" rating on BYD shares, target price of HK $640

Based on today's closing price of HK $295, this price means that there is still 117% room for growth!

The bank expects the company to produce 280,000 units per month in December this year, implying an 11% month-on-month increase for the remainder of 2022, with full-year sales reaching 1.9 million units, up from the current forecast of 1.6 million units.

Macquarie: Maintain BYD's "outperform" rating, target price rises 29% to HK $357

If calculated at today's closing price, this price means that there is still 21% room for growth!

The bank believes that BYD, as the market share leader of new energy vehicles, has the advantage of an integrated supply chain, and its market share increased by 8 percentage points to 26% in the first half of the year, mainly due to its leading plug-in hybrid vehicle (PHEV) strategy and full-price product portfolio. The bank expects the company's market share to further increase to 30% in the second half of the year and 32% in 2023.

Macquarie: Maintain Li Auto -W "Outperform" rating, price target up 12.9% to HK $142.6 from HK $126.3

If calculated at today's closing price of HK $134.3, this price means that there is still 6% room for growth!

The bank believes that the company's sales have rebounded strongly since May, and believes that the demand in the luxury car market is relatively stable. The new model L9 will be launched in August, providing growth opportunities in online cities and the luxury car market, and forecasts sales of 10 7,000 units in the second half of the year. However, the bank is still bearish on ideal ONE sales in the second half of the year.

UBS: Maintain Xiaomi Group's "Buy" rating, cut its price target to HK $14 from HK $14.6

If calculated at today's closing price of HK $12.12, this price means that there is still 16% room for growth!

The bank predicts that Xiaomi will sell 38 million smartphones in the second quarter of this year. It believes that Xiaomi is actively carrying out promotional activities during the "6.18" shopping festival to clear channel inventory with discounts, which is expected to lead to greater-than-expected smartphone gross margin pressure. Gross margin is forecast to be 8.9%, compared with 9.9% in the first quarter of 2022.

The bank believes that the inventory of Xiaomi's business in China is close to normal levels, but it may take another quarter for the business in Europe to reach normal levels.

Goldman Sachs: Maintain "Buy" rating on MINISO, target price of HK $23.2

If calculated at today's closing price of HK $12.76, this price means that there is still 82% room for growth!

When the company announces its fiscal fourth quarter results at the end of this month, the bank will monitor the progress of its business recovery in different regions, branch expansion, pricing strategy and cost saving plans.

The report quoted the company's Yingxi, which expects the adjusted net profit for the quarter ended June 30 to be no less than 200 million yuan, an increase of no less than 40% year over year, which is about 24% higher than the bank's original forecast. MINISO's management attributed the increase in adjusted net profit to higher gross profit margins due to a higher overseas business portfolio, increased profit margins on IP products, and effective cost control responses. The bank believes that the company's overseas and domestic businesses will gradually recover, and operations have bottomed out, while brand upgrades, improved product and geographic mix also lead to higher gross profit margins.

Citi: Maintain AMD's "neutral" rating, reduces price target by 13% to $96 from $ 110

At yesterday's closing price of $98.09, this price implies a 2% downside.

The bank believes that AMD reported mixed results, but guidance was below consensus, and that the recession is affecting AMD despite repeated gains in its stock price. "AMD is likely to experience more declines when the data center market slows, although this may provide us with an opportunity to upgrade the stock," analysts said.

Credit Suisse: Maintain Lyft's "outperform" rating, cuts price target by 17% to $50 from $60

If calculated at yesterday's closing price of $16.71, this price means that there is still room for 200% upside!

The West Coast continues to lag most of the U.S. in terms of the relative pace of recovery in the U.S., with Lyft more focused on those markets, while at the end of March, the San Francisco market recovered 50% compared to the overall average of 70%, the bank said. Additionally, the bank chose to assume an acceleration in early 2023 given the slower recovery in demand in key regions. The bank also expects Lyft to continue increasing driver incentive spending for the remainder of 2022 to provide a better customer experience.