TSMC: Capital expenditure remains unchanged, maintaining original plan (FY23Q4 conference call minutes)

On the afternoon of April 18, 2024, Beijing time, before the U.S. stock market opened, TSMC (Taiwan Semiconductor Manufacturing Company) released its financial report for the first quarter of 2024 (ending April 2024). Here are the key points from the earnings call:

For a detailed interpretation of TSMC's 2024 first quarter financial report, please refer to " Taiwan Semiconductor: iPhone underperforms, NVIDIA saves the day 》

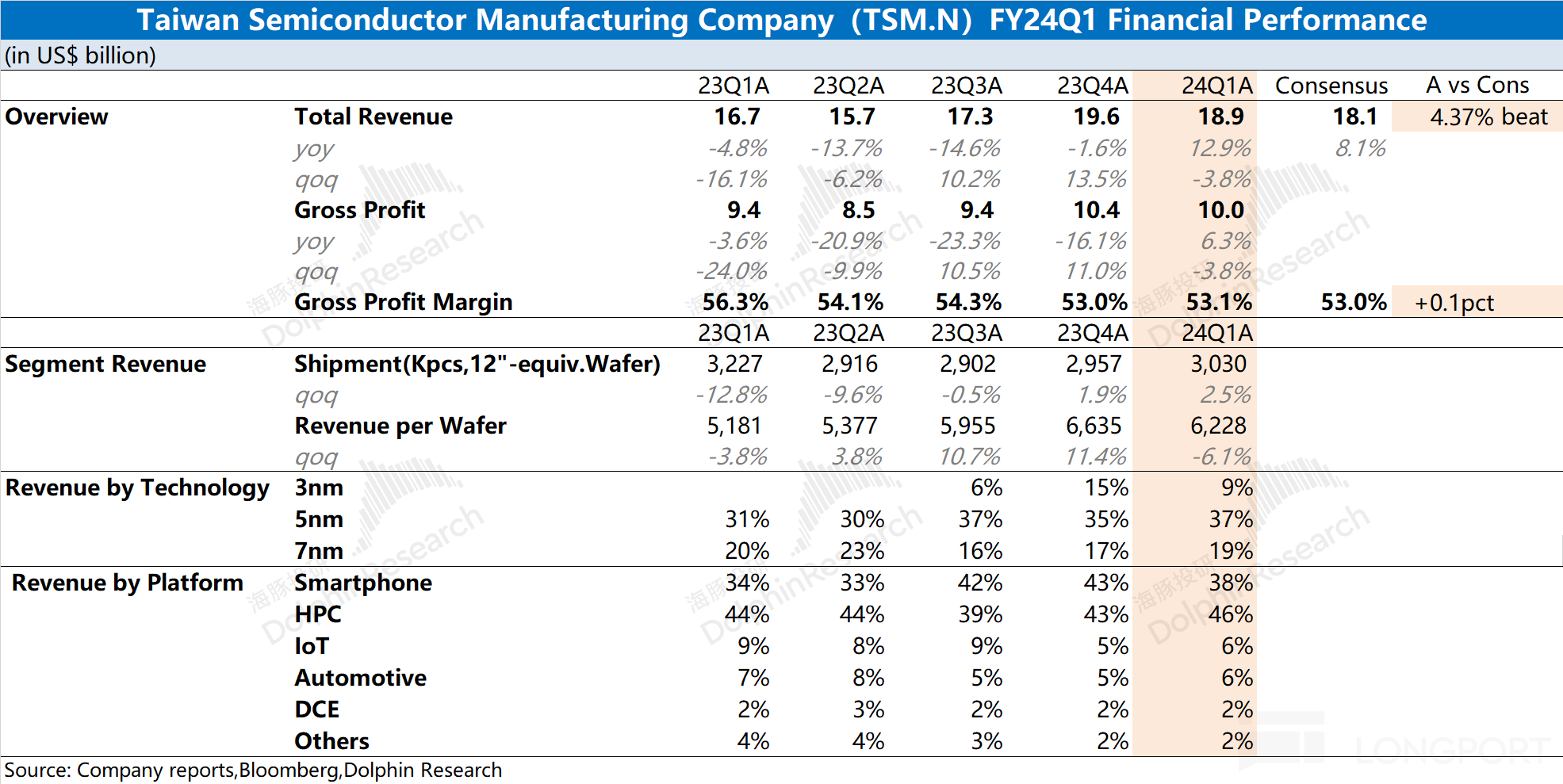

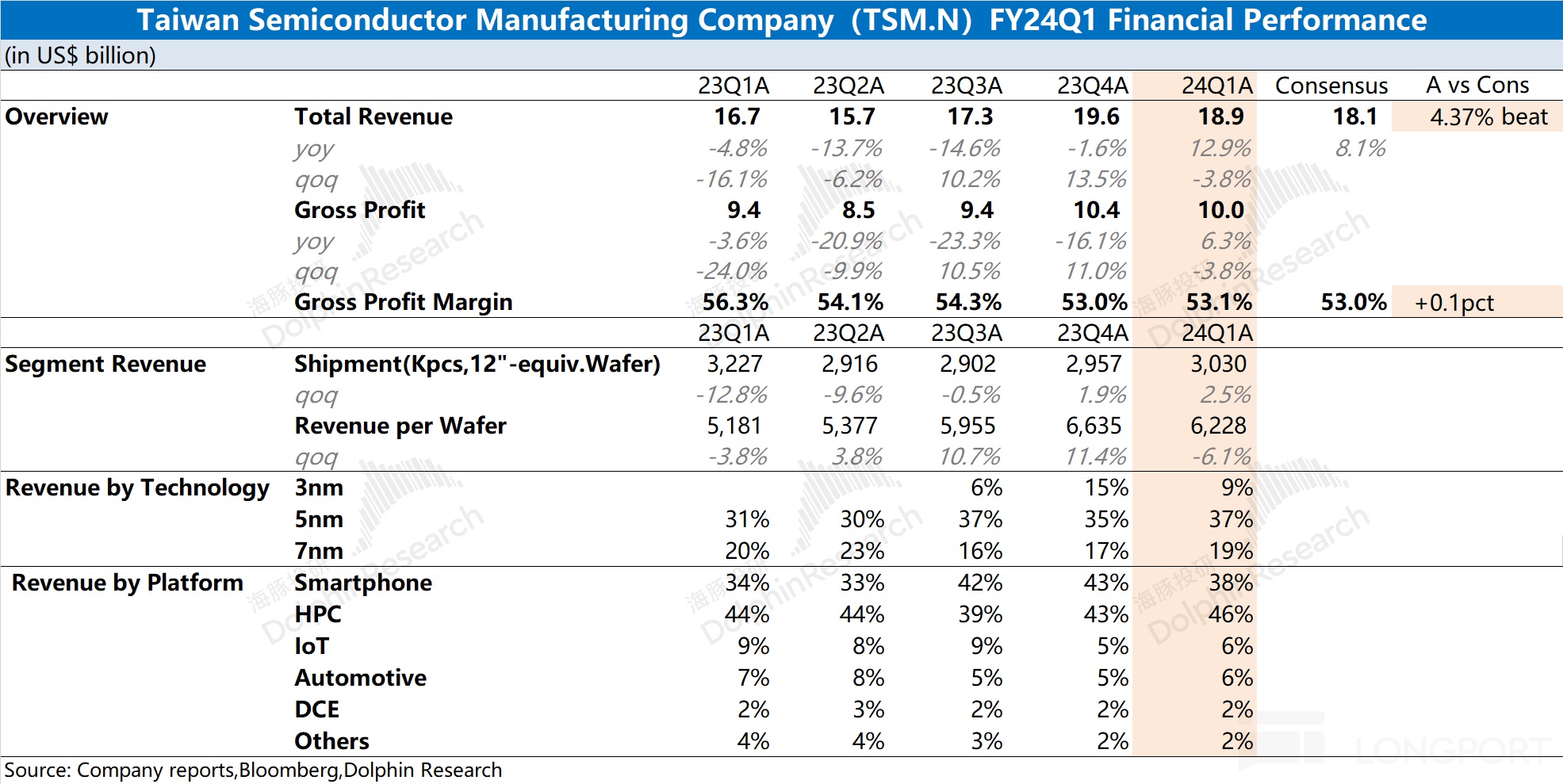

1. $Taiwan Semiconductor.US Financial Highlights:

2. Details of TSMC's Financial Conference Call

2.1. Key Points from Executive Statements:

- Guidance for the Second Quarter:

a. Revenue Forecast: Expected to be between $19.6 billion and $20.4 billion, a 27.6% increase compared to the same period last year. Revenue is partially offset by the seasonal adjustment in the smartphone market but is supported by sustained demand for high-performance computing;

b. Gross Margin: Expected to be between 51% and 53%. Includes special events: earthquake-related wafer scrap leading to a negative impact of approximately 50 basis points; electricity price increases having a negative impact of around 70-80 basis points on gross margin;

c. Operating Profit Margin: Expected to be between 40% and 42%;

d. Tax Rate: Expected to be slightly above 19% for the second quarter, and will subsequently decrease to 13%-14%.

Capital Budget:

Total Budget: The total budget for 2024 is expected to be between $28 billion and $32 billion (unadjusted);

Capital Allocation: 70% to 80% to be invested in advanced process technology, 10% to 20% for special technologies, and around 10% for advanced packaging, testing, mask manufacturing, etc.

- Global Factories:

a. North America: Planning to build three factories in Arizona to support the US market, expected to enhance economies of scale;

b. Asia: Establishing a specialized technical factory in Kumamoto, Japan, to support specific customer needs in consumer electronics, automotive, and other fields;

c. Europe: Building a factory in Dresden, Germany, focusing on automotive and industrial applications.

d. Overseas Strategy: TSMC's overseas expansion is based on customer demand and government support, managing overseas cost differentials through strategic pricing and government cooperation 4) Outlook:

a. Performance: It is expected that the global semiconductor market (excluding memory) will gradually recover moderately by about 10% in 2024, with the foundry industry expected to grow in the mid to high single-digit percentage range. The company's full-year revenue growth is expected to be in the lower to middle range of 20%.

b. Technology: The N2 technology is expected to enter mass production in 2025, focusing on high density and energy efficiency, with significant demand expected in the AI market.

2.2 Q&A Analyst Q&A

Q: Where do we see demand growth slowing in which areas or applications? Additionally, how do we view this demand shift in terms of artificial intelligence and traditional servers, and what impact does it have on TSMC?

A: Demand in the smartphone market is gradually recovering but not very rapidly. The personal computer market is saturated, with a slow recovery pace. However, data center demand related to artificial intelligence is very strong. Traditional server demand is relatively weak, IoT and consumer markets remain inactive, and automotive inventory is still adjusting. For TSMC, the shift in budgets of large players towards AI servers is very favorable for us, as we can capture most of the semiconductor content in the AI server field, such as GPUs, AC network processors, etc. Our market share is lower in the traditional low CPU server field. Therefore, we expect our growth to be very healthy.

Q: What major changes have we seen in the overall end market compared to three months ago? Are there any specific areas that have shown significant changes?

A: Three months ago, we expected growth in one of our automotive platforms this year, but now we expect it to decrease. So I think this is an area where we have noticed a difference.

Q: Is the weakening or dragging of our gross margin by N3 more severe than past nodes like N5 and N7? With the arrival of N2, will we face a similar situation, and how is the gross margin situation for N2?

A: It takes longer for N3 to reach the enterprise gross margin than N5 or N7, partly because of the increased complexity of N3's process and our company's average gross margin has also increased. Another reason is that we set the pricing for N3 early on but experienced cost inflation pressures in the following years. Therefore, N3 will take longer to reach the company's average gross margin. As for N2, we have done better in terms of cost and value pricing, and the gross margin situation for N2 is expected to be better than N3.

Q: Does TSMC feel that we have received fair or correct value returns? How should we price for artificial intelligence?

A: We have been working hard to ensure that our value is fully reflected, and we are pleased to see that customers have achieved good results. This is a win-win situation for both us and our customers.

Q: Demand for our mature nodes (12 nanometers and above) has decreased compared to the same period last year. How is the outlook for the recovery of mature nodes in the second half of the year? A: The demand for mature nodes is currently relatively weak due to the slow recovery pace of the entire semiconductor industry, and it is expected to gradually improve by the second half of 2024. We cooperate with strategic customers to develop professional technical solutions, and create lasting value for customers, so the potential impact of possible excess capacity is relatively small. We believe that our profits and utilization rates on mature nodes can be effectively protected.

Q: When is N2 expected to start generating significant revenue contributions? Also, considering the increase in N2 sampling quantities, how does its potential contribution in the next few years compare to N3 or other nodes?

A: The upward curve of N2 is very similar to N3, due to factors such as cycle time. We expect that production of N2 will start in the second half of 2025, actually in the last quarter of 2025. Due to cycle time and backend processing factors, we anticipate significant revenue to start from the end of the first quarter or the beginning of the second quarter of 2026.

Regarding your second question, our customers work closely with us, and the sampling quantities will increase, leading to intense production growth. Although N2 is a complex technical node, customers may need more time to prepare for sampling, but we still believe that N2 is very important for TSMC.

Q: With such a strong demand for artificial intelligence, what does this mean for our capital expenditures and capacity planning? How does this impact our capital intensity outlook?

A: For TSMC, higher levels of capital expenditures are always associated with higher growth opportunities in the coming years. We work closely with customers to plan capital expenditures and capacity based on long-term market demand structures to meet multi-year megatrends. Capital expenditure plans are regularly reviewed, and as a key driver of artificial intelligence, we will work closely with customers to plan appropriate capacity levels to meet their needs.

Capital intensity has been high in the past few years, but the growth rate of capital expenditures is now trending towards moderation. Therefore, we expect capital intensity to be at around the mid-30% level, but if opportunities arise in the coming years, we will invest accordingly.

Q: Is this year considered a digestion year because we have pushed a lot of 3-nanometer spending in the past few years? Should we view this trend as a lower level or as a normal situation?

A: I wouldn't call it a digestion year. Each year, our investments are based on forward-looking business opportunities, and we constantly review them. So this is our outlook for the future and the use of the funds we are investing in.

Q: Faced with many cost challenges such as rising electricity prices and increased costs of overseas wafer fabs, what is the pricing strategy, and is there a specific percentage range?

A: Our pricing strategy is confidential and entirely between us and the customers. We are facing some cost challenges such as rising overseas costs and electricity price increases. We expect customers to share some of the cost increases with us and have started discussions with them. For the costs of overseas wafer fabs, we hope to share our value, including geographical flexibility Q: Due to the continuous strong demand for CoWoS, the production capacity is extremely tight. How does TSMC decide to allocate production capacity to customers? Will we reserve capacity for large customers while also leaving space for small customers? Additionally, if customers want to choose other suppliers, are we able to accept that?

A: The demand is extremely strong, and we have done everything possible to increase production capacity, but it is still not enough to meet customer demand. We are using partners to supplement capacity, but it is currently insufficient. Our top priority is to ensure customer success, and long-term partners will receive better support. With the surge in demand, we will do our utmost to increase production, and we are not considering giving up market share but rather helping customers succeed.

Q: Regarding artificial intelligence accelerators, they are currently using 5-nanometer technology. Do we expect them to catch up with the most advanced technology? How do we view artificial intelligence accelerators, as well as high-performance computing, as drivers or adopters of TSMC's most advanced technology?

A: Currently, most artificial intelligence accelerators are using 5-nanometer or 4-nanometer technology. My clients are working with TSMC to push the technology to the next generation and even the generation after that. They need to accelerate because AI data centers need to consider energy consumption. Our 3-nanometer technology is more advanced than 5-nanometer, and 2-nanometer technology will further enhance it. It can be said that all customers are actively responding to the technological trend from 4-nanometer to 3-nanometer and then to 2-nanometer.

Q: So, given such strong demand for artificial intelligence, should we expect that the 2-nanometer technology in the next two years will bring more revenue than previous nodes?

A: We expect that the revenue contribution of N2 will be greater than N3 because we believe advanced technology will continue for a longer time, and N2 will be a larger node.

Q: Noting that we generated very strong free cash flow in the first quarter, considering that capital intensity is beginning to stabilize and we paid a high retention tax, would like to know if we will increase dividend payments in the coming quarters? Or what can investors expect?

A: Our dividend policy is to pay 70% of free cash flow as cash dividends in a year, so I would not judge solely based on quarterly free cash flow. However, as we have mentioned before, we are now reaping the benefits of investments made in the past few years, and we expect our dividend policy to steadily increase from the sustainable level of the past few years.

Q: Smartphones and personal computers are increasingly incorporating artificial intelligence. She wants to know our views on this trend and the impact on TSMC?

A: Adding neural processors for artificial intelligence will increase the size of chips. In the future, the replacement cycle for smartphones or personal computers may accelerate. Overall, the integration of artificial intelligence on devices is very positive for TSMC as we will capture a larger market share.

Q: Should we expect a significant increase in demand for N3 in the second half of this year or entering 2025? A: We expect to see a trend of increasing chip sizes, which has already begun. As for the acceleration of replacement cycles, we anticipate it happening, but we cannot provide specific numbers at the moment because it is too early to make predictions for 2025. However, what can be confirmed is that this trend is upward. Additionally, we expect N3's revenue to more than double compared to 2023 this year.

Q: What are the future prospects for advanced packaging solutions and 3DIC solutions in the coming years? Can you comment on TSV and hybrid bonding?

A: 3DIC packaging technology is very complex, and our customers are just starting to adopt it, so there is not yet a large demand, but we expect it to gradually increase starting from this year. It is difficult to determine the scale of it, but I believe it is a trend. Whether it is micro-bonding or hybrid bonding, it depends on the product requirements of the customers. Their products will be launched soon.

Q: Considering that our 7nm process is still underutilized, will you consider transitioning 7nm tools to support stronger demand?

A: We can shift capacity from one technology node to the next because they are adjacent and connected, for example, transitioning from 5nm to 3nm is relatively easy. However, not every node can do this. We currently do not have plans to convert N7 to N5 because we expect the demand for N7 to grow again in the coming years, just like in the 28nm era.

Q: Can you provide a timeline for when smartphone applications will adopt SOIC?

A: HPC products are the first customers to adopt 3DIC or SOIC advanced packaging technology. As for other areas, we are taking a wait-and-see approach.

Q: The revenue in the first half of this year showed good growth, but the full-year guidance remains in the mid-to-low 20% growth range. Is this because of increased caution for the second half or to see how things develop?

A: Our guidance for the quarter outlook has not changed. We have always said that growth between quarters will continue, and the full-year guidance remains unchanged.

Q: Regarding advanced packaging, will there also be plans to build advanced packaging facilities in Arizona? Any plans?

A: The location of packaging services is usually determined by the customers. We are pleased to see that AMCO recently announced the establishment of an advanced packaging facility very close to our AG factory. In fact, we are working with AMCO to support the needs of all customers at our AG factory.

End of Document

Risk Disclosure and Disclaimer for this article: Dolphin Investment Research Disclaimer and General Disclosure