Amazon, Google, Microsoft, are the giant stars falling? The "meteor shower" in US stock market is not yet over

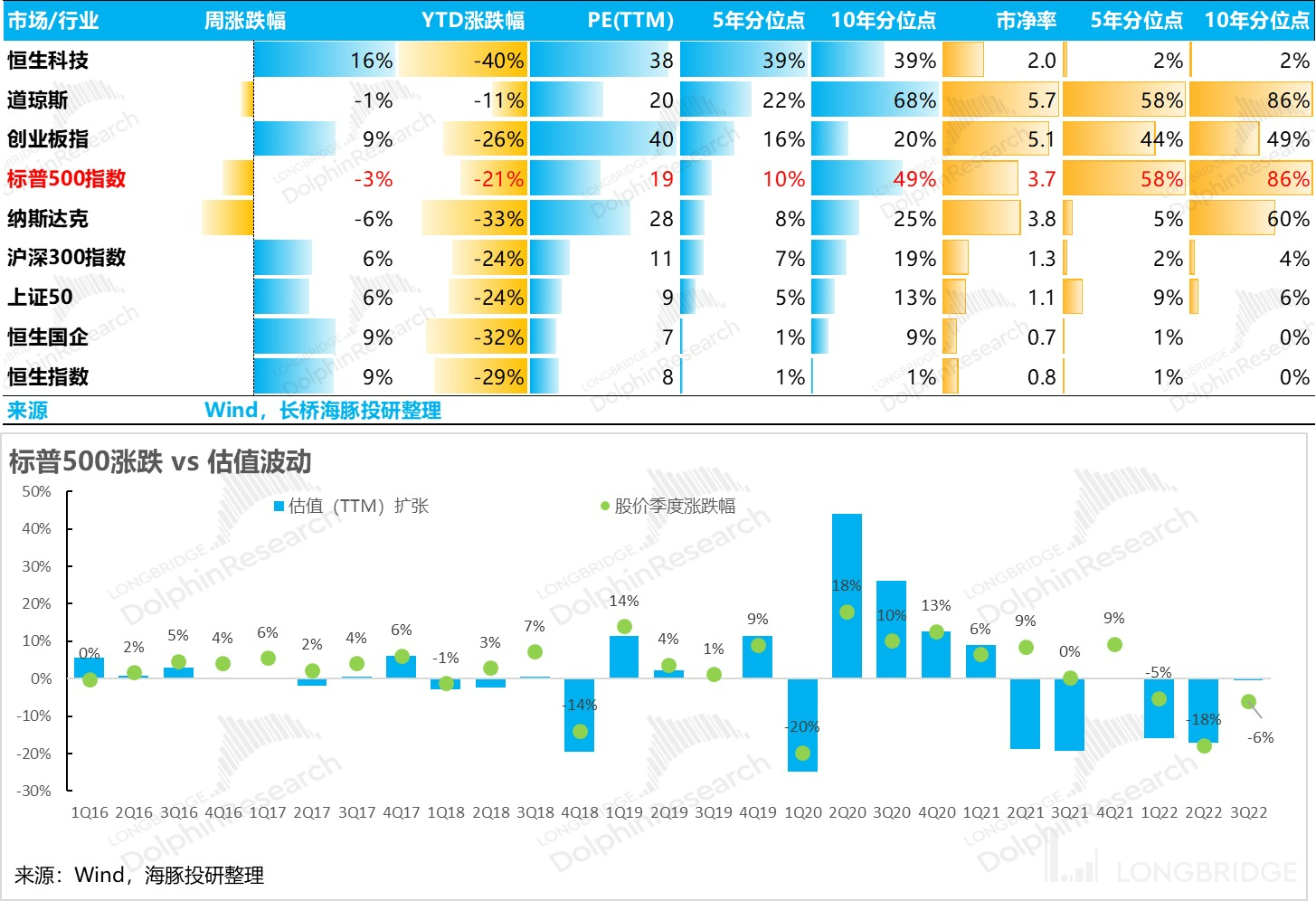

Accompanied by the fall of the giants in the third quarter, the global stock indices have generally fallen between 20-30% this year. From a valuation perspective, the PE valuation of the S&P 500 index is only about 8% of the valuation history of the past five years. It seems cheap enough.

So, where is the rate hike now? Is the valuation done killing? After the valuation is killed, will there be performance killing? How tragic will the performance killing be?

These two issues are almost the two big mountains that Dolphin Analyst sees in most companies. Therefore, before delving into the analysis of individual stocks, Dolphin Analyst attempts to explore these two major issues from the perspective of individual stocks and macro levels.

First, valuation killing: will interest rate hikes continue?

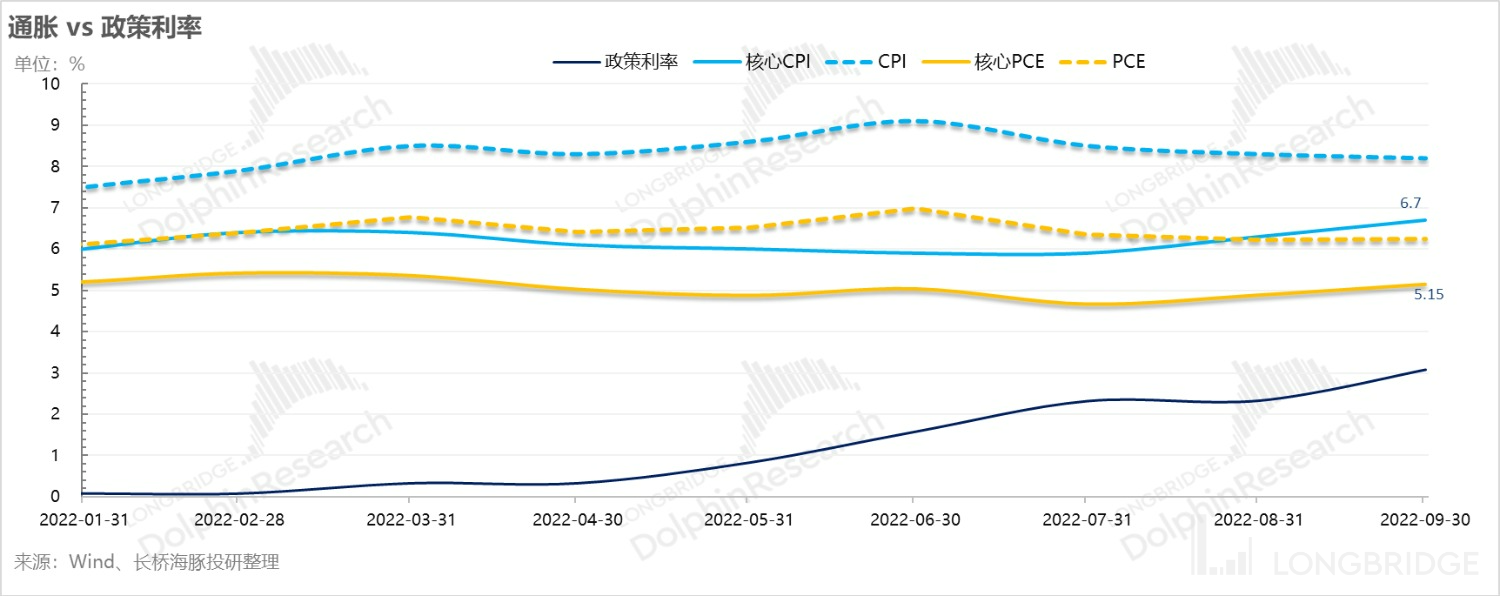

Since the beginning of this year, after six interest rate hikes by the Federal Reserve (the first two were 25, 50+ and the recent four were each 75 basis points), the Fed's policy interest rate has accelerated from zero interest rates (0-25 basis points) to 3.75%. -4%.

When observing several core indicators: (1) core CPI in September was 6.7%, and the fluctuation in the nine months since the start of the interest rate hike was between 6% and 6.7%; (2) core PCE in September was 5.15%, and the fluctuation in nine months was 4.7-5.4%. Especially in September, in the process of the interest rate hike quickly chasing inflation, the inflation on a month-on-month and year-on-year basis seems to be widening.

Since the last global inflation wave happened too long ago, and from a long-term and limited historical information, in each round of the previous inflation cycle, the peak of the Fed's policy interest rate after interest rate hikes clearly exceeded the peak of the core PCE inflation rate in that round.

Then there is a high probability that when the market seems to expect interest rates of around 5.0-5.5%, the real interest rate of the market (relative to demand-driven inflation) gradually turns positive, and the possibility of interest rate hikes gradually reaching the peak is expected.

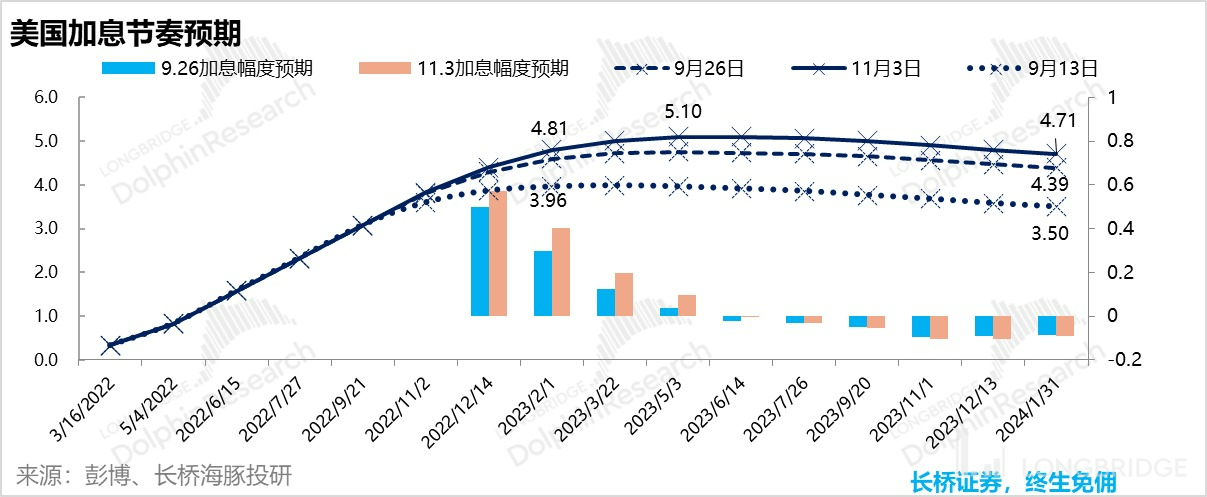

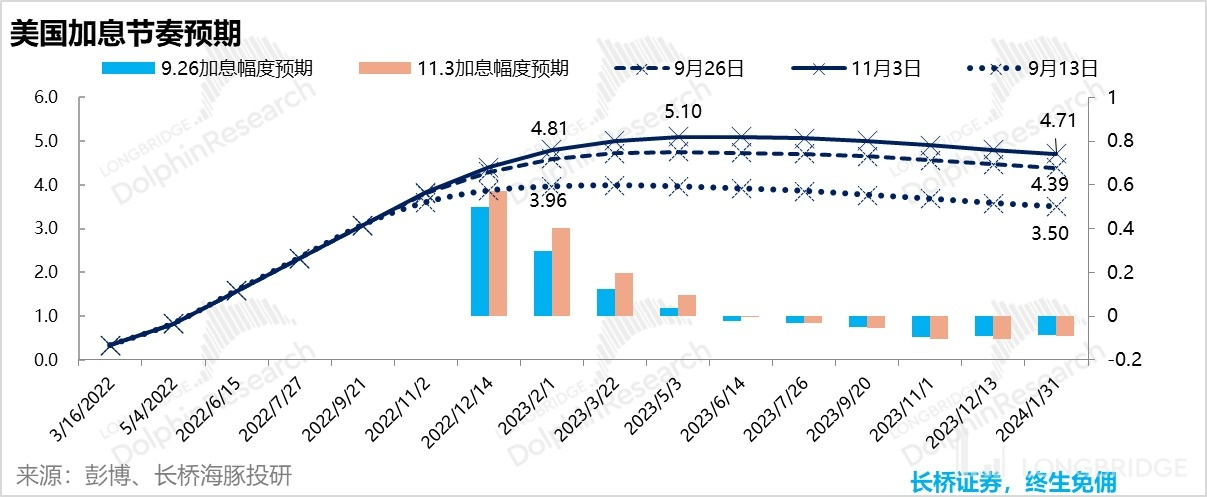

Taking the core PCE of 5.15% in September as a reference, the current policy interest rate is 4%, and it can be achieved with just two 50 basis points hikes and one 25 basis points hike. After the announcement of the November rate hike meeting by the Fed, the market is filling this expectation:

The market's expectation of interest rate hikes corresponds to adding 50 basis points each in December and January, keeping up with the inflation level, and then entering a slow rate hike or high-level stagnation, and some people expect a rate cut in the second half of 2023.

The three stages of this round of Fed rate hikes are "stepping on the accelerator, high interest rates, and a high-interest rate tug-of-war." In these three stages, if the next two rate hikes are a combination of 75+50, the interest rate will quickly exceed the current core PCE range. Therefore, the Fed's acceleration of rate hikes is basically coming to an end. This is also the core message conveyed by the Fed in the latest rate hike meeting. After slowing down the pace of rate hikes, the most important remaining question is where the endpoint should be and how long we should stay there.

In the previous rate hike cycle, if each rate hike exceeded the core PCE range, the expected endpoint for rate hikes is around 5.25-5.5%, and the current expectation of the endpoint is 5-5.25%, which is approaching this critical point. Especially as we gradually approach the endpoint, the faster the rate hike is, the more likely the market will think that we are approaching the endpoint.

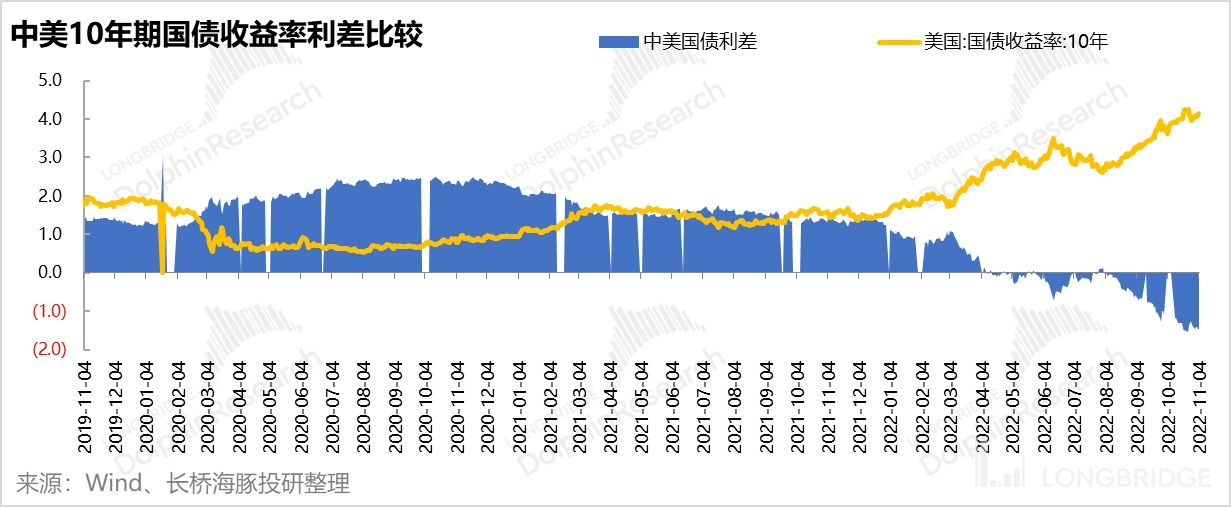

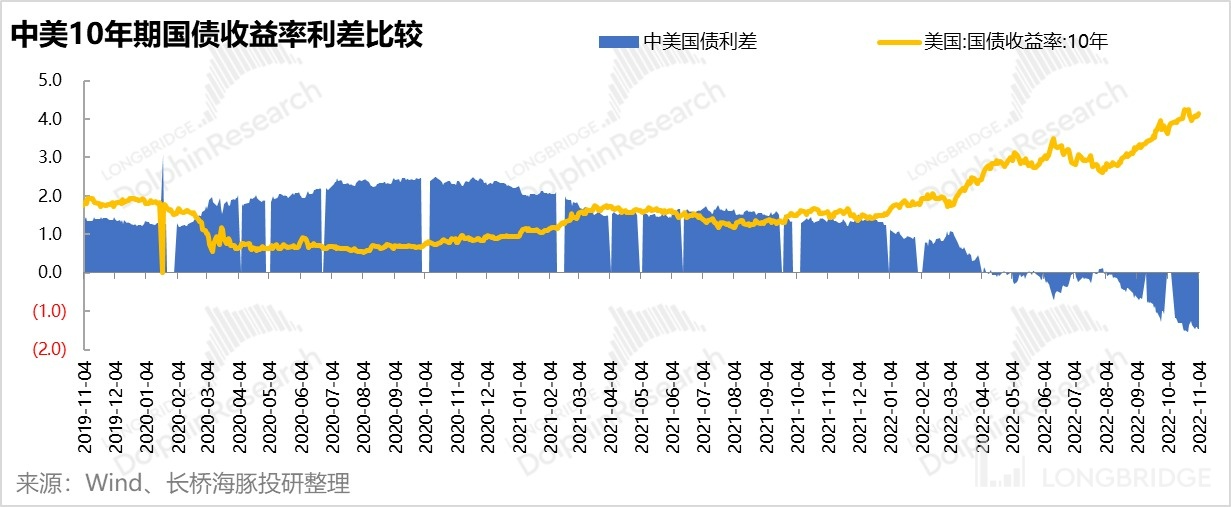

As the rate hike speed and endpoint continue to rise, the yield of risk-free assets US Treasuries continues to climb, causing global equity markets to generally experience a valuation slump. The duration of the high-interest-rate tightening phase is of completely different significance for Dolphin Analyst in the Hong Kong and US markets:

- Hong Kong stocks, as the peripheral market for the US dollar and the main carrier of mainland assets, have bottomed out in terms of valuation in various markets due to the continuous outflow of the US dollar during the strong dollar cycle. However, reaching the peak of rate hikes and stabilizing liquidity is like unshackling Hong Kong stocks from a big burden. As Hong Kong stocks follow mainland policies in terms of performance fundamentals, companies in Hong Kong, mainly those in the real estate and technology sectors, have already experienced their worst moments. In the future, there will be expectations for recovery. Based on their super-low valuations as a safety margin, Hong Kong stocks may be approaching their opportunities, and the real macro risk is mainly the issue of delisting.

- As for US stock assets, the most intense phase of rate hikes has passed. However, keeping high-interest rates for a long time is more about allowing the economy to fully experience the "chill" of high-interest rates and transmitting high borrowing costs to every industry operating in the domestic currency. In other words, the duration of the high-interest rates will impact whether the performance fundamentals of US stock companies will deteriorate.

From the perspective of controlling inflation, in a situation where the employment rate remains high, it is necessary to raise the unemployment rate, driving the economy into a slight recession state, in order to break the cycle of labor shortage, rising wages, and rising prices. This intention can also be seen from the Fed's economic forecast data in September.

Therefore, for US stocks in the next phase after overcoming the pressure of systematic valuation slumping, greater attention will be paid to the performance fundamentals of the companies themselves. Next, Dolphin Analyst will look at where the US economy has gone from a fundamental perspective. Macro perspective from individual stock leaders: "The fall of giants" and the B-C polarization behind the meteor shower

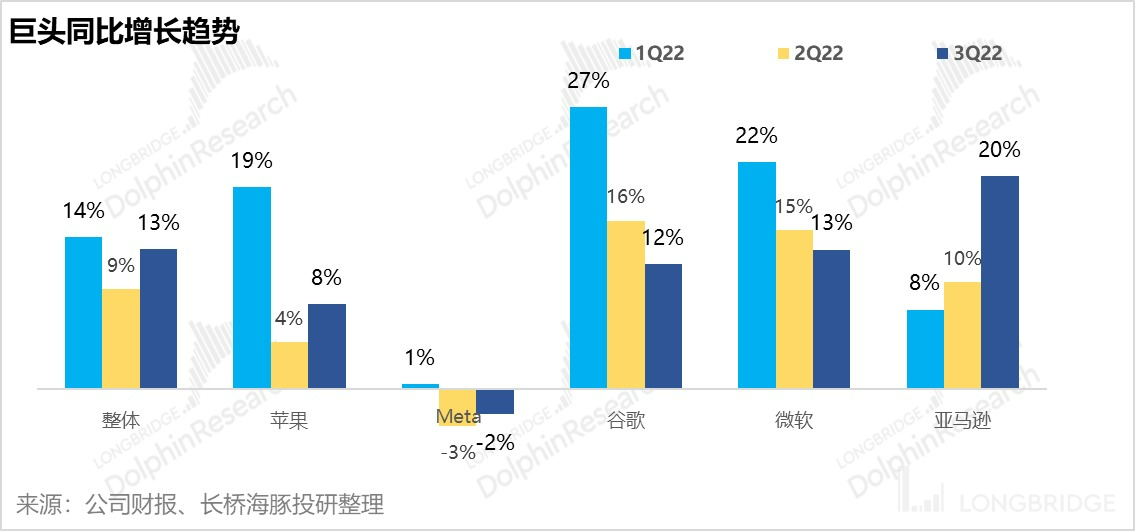

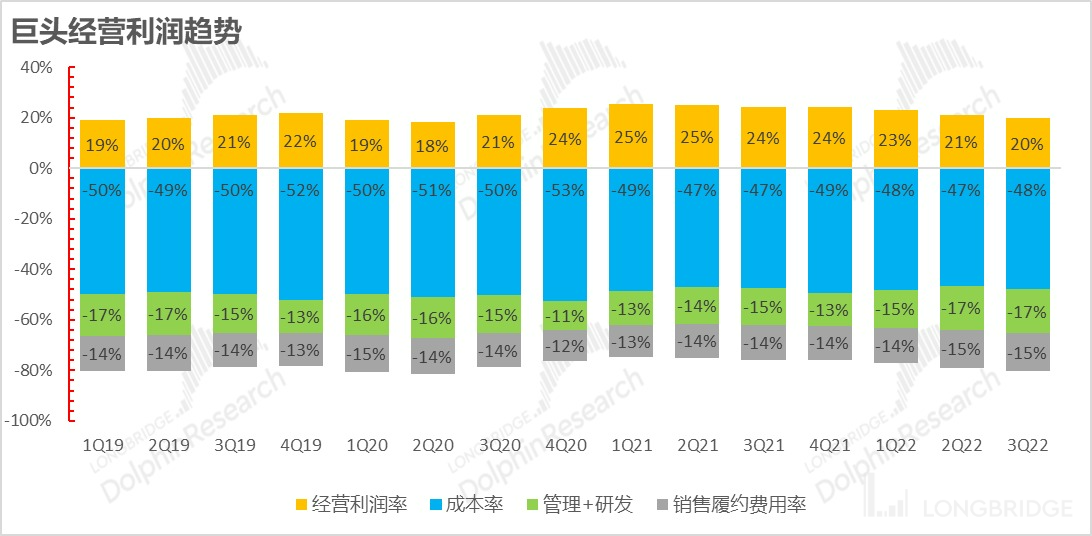

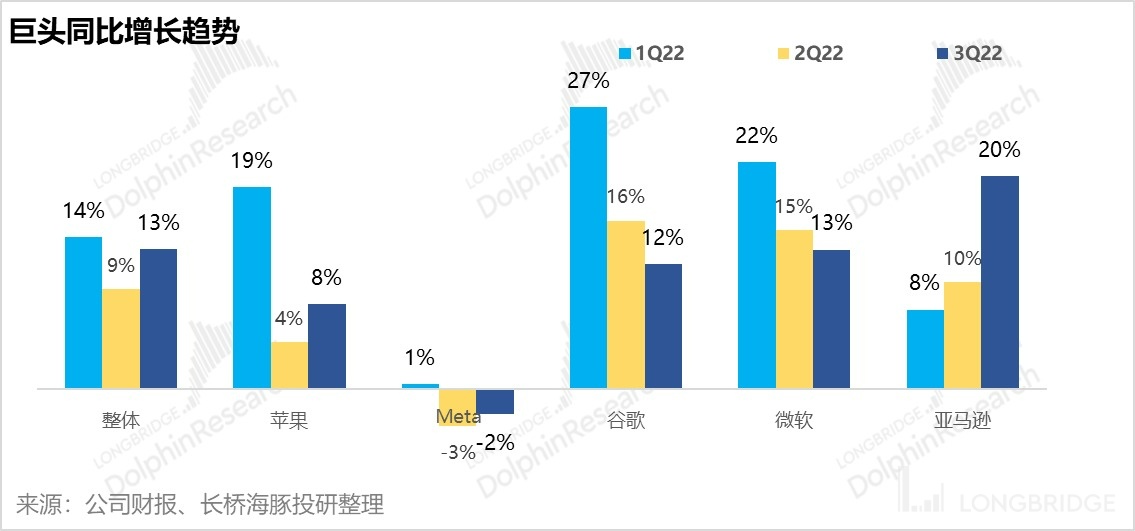

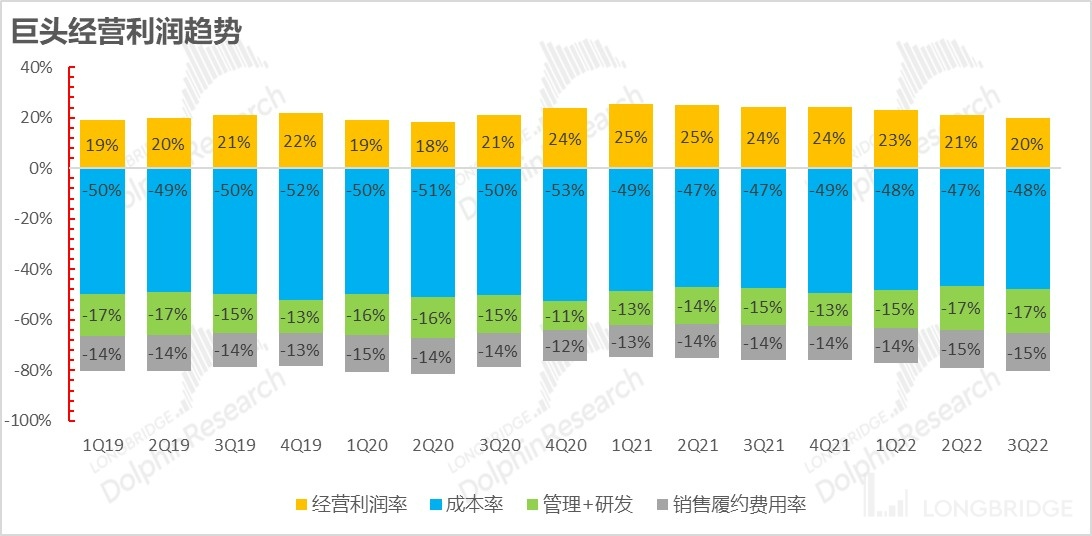

If there is one phrase that can summarize the just-ended Q3 earnings season for US stocks, "the fall of giants" is probably the most straightforward. Among the giants covered by Dolphin Analyst, Apple remains the only backbone that still seems relatively firm, while Microsoft, Google, Amazon, and Meta have all fallen.

However, a closer look at these falls reveals that they were more of an expected decline than a real one, as the fourth-quarter guidance was uniformly pessimistic. Considering the subjectivity factors of market value management and expectation guidance in the guidance itself, Dolphin Analyst focuses on the core information hidden in the actual Q3 performance itself:

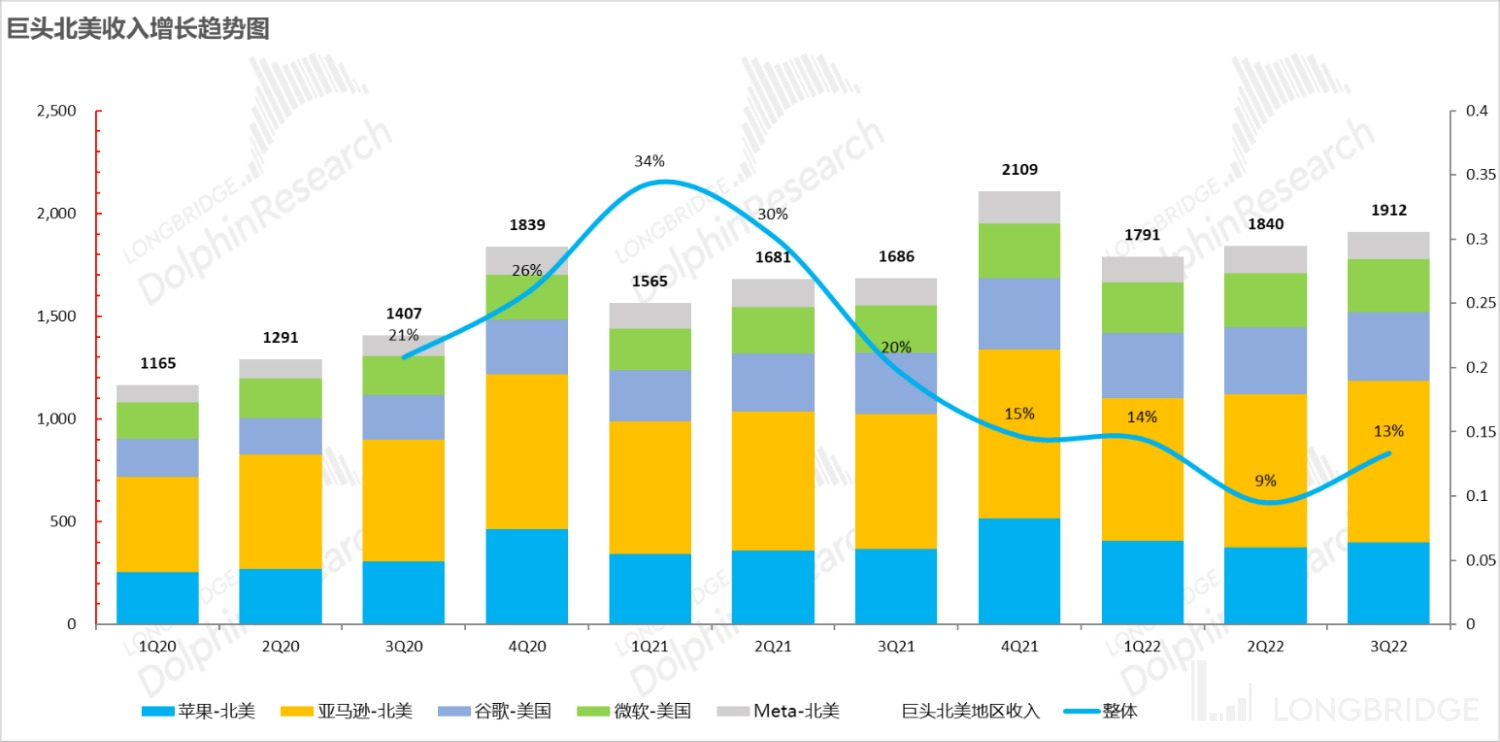

1) Local business growth is not inferior

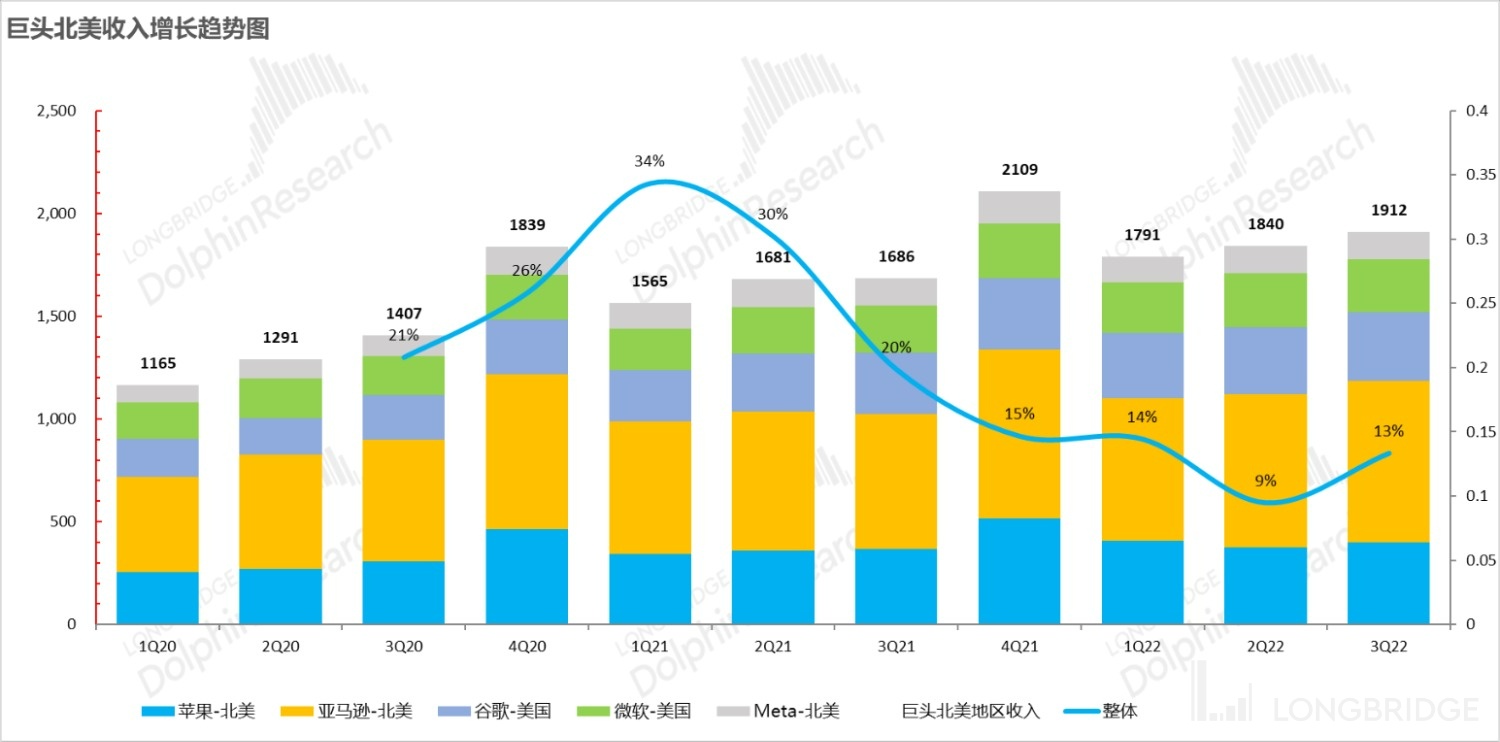

From the perspective of the overall revenue growth of the top five Internet tech giants, their North American business revenue (using the most accurate meaning of US region revenue, and using approximate regions if the US is not applicable) not only did not decrease in Q3, but also accelerated its growth, which is not as pessimistic as what the giants had guided.

2) To-C business is stronger than To-B business

A detailed breakdown shows that the marginal changes in this wave are more obvious in the To-B business' creative ability decline speed compared to the To-C business:

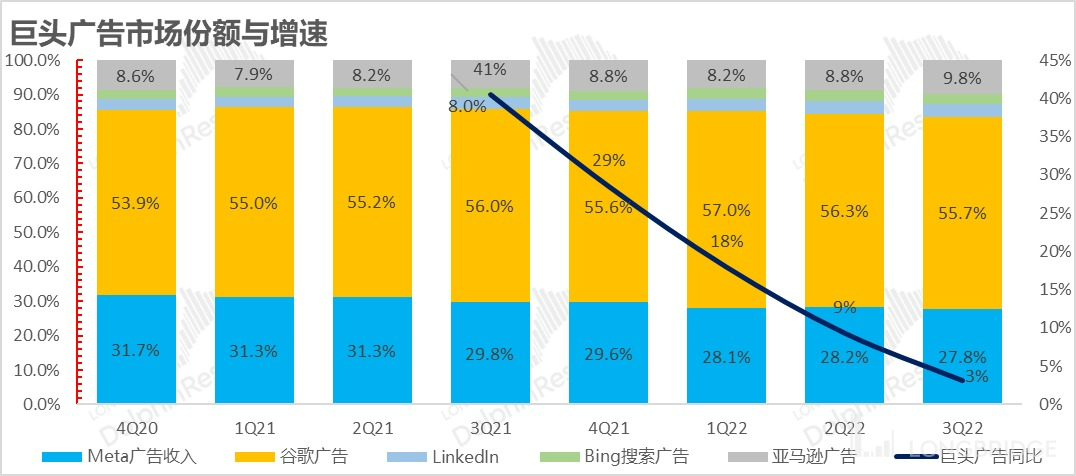

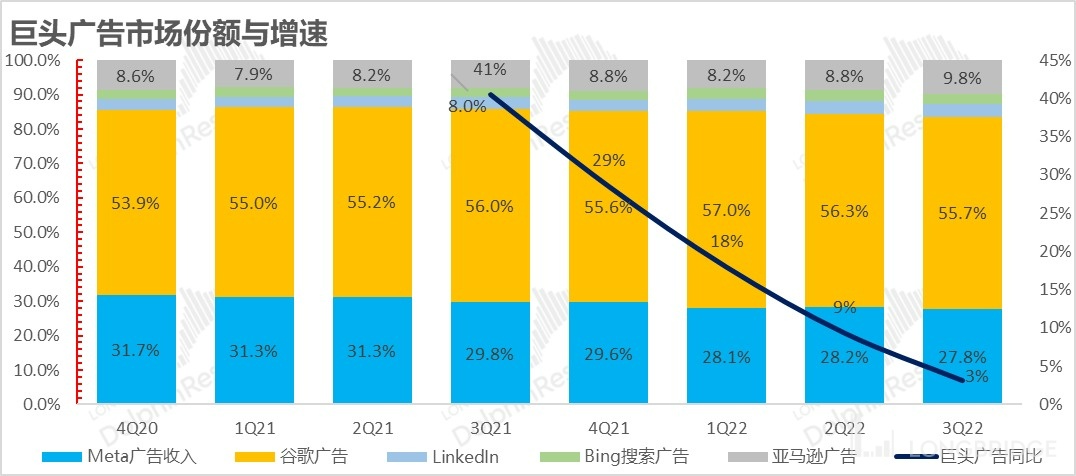

a). Advertising in To-B business: Advertising platforms generally earn revenue from advertisers' advertising budgets, and the slope of revenue growth slowdown is very steep. Combining Dolphin Analyst's summary of the advertising sector in the previous article "Cold air spreads the relay race, Google and Meta have no reprieve", advertisers' pessimism about the business prospects should be a major factor.

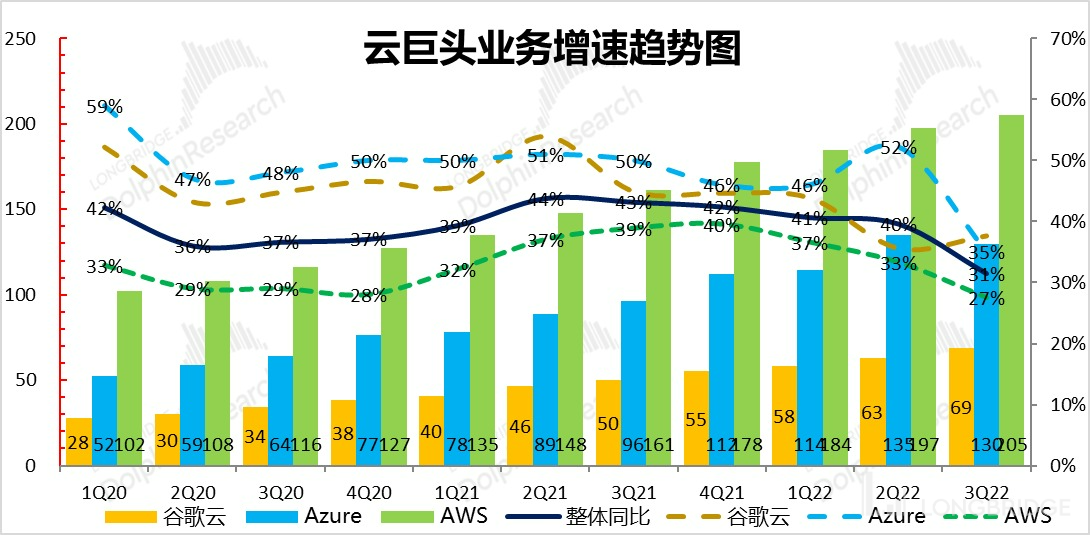

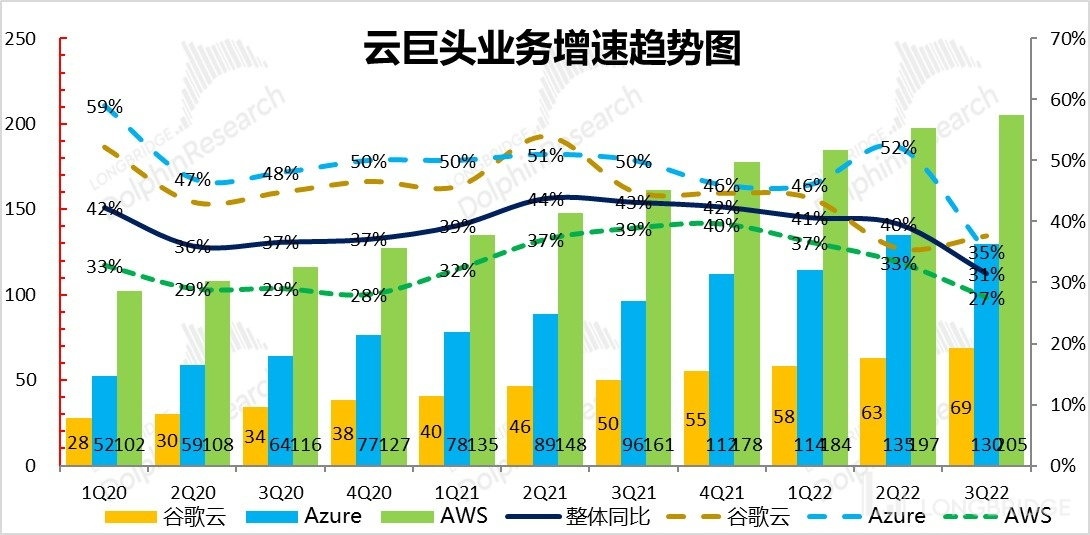

b.) Public cloud in To-B business: Cloud business corresponds to the budget of enterprise owners for IT expenditures. It can be seen that except for Google, whose base is relatively low, the revenue growth of the three major public cloud giants has slowed down significantly across the board, with its growth rate dropping from 40% in Q3 to 31% rapidly.

c.) The To-C business is more resilient: Compared to the underperformance of the overall To-B business, selling physical goods in the To-B business seems to be doing better, of course, Apple and Amazon had special factors this quarter—Apple's new product launch conference was held a week in advance and Amazon's Prime Day was moved to the Q3 this year, which brought about an increase of several percentage points from the previous quarter.

d) Why did the business of B go through a crisis, while that of C remained relatively stable?

In addition, Dolphin Analyst noticed that this finding echoed the private investment shrinkage and the relatively strong consumer spending in the US macro data GDP. And why? Dolphin Analyst tried to identify the reason by examining the profitability of the giants:

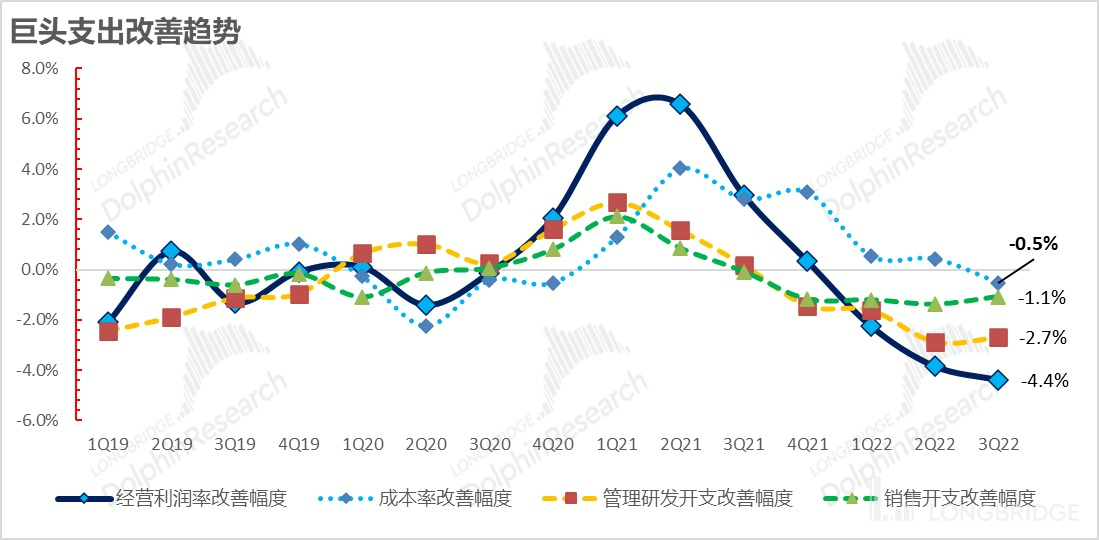

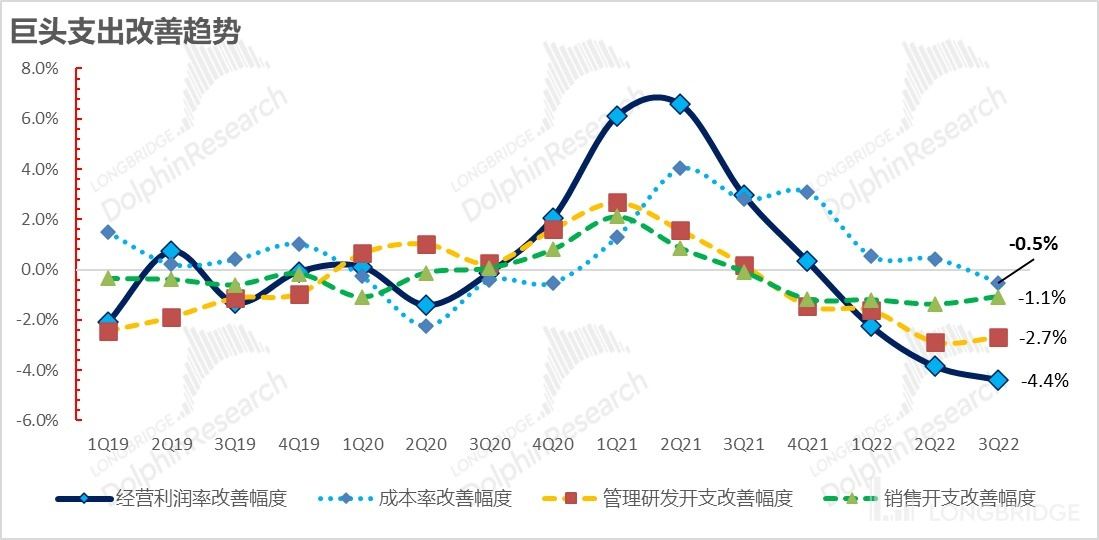

From the overall operating profit of the five giants, the profitability of the giants all declined coincidentally, even as their overall revenue remained relatively stable. The reasons for this can be generalized as:

(1) Appreciation of the US Dollar impairs gross profit margin: According to Microsoft's guidance, the appreciation of the US dollar not only suppressed the company's revenue growth, but also suppressed its gross profit and profit performance.

(2) Pressure of resource costs: In the composition of the investment elements of cloud business, besides server equipment, the largest variable cost, apart from labor, is electricity expenses. Amazon mentioned the pressure of electricity expenses on the gross profit margin of cloud business.

(3) Pressure of labor costs: In this cycle, the most rigid cost item is the research and development input cost that centers on labor input.

(4) Worsening Competitive Environment: The core reason for the decline of the gross profit margin of Google and Meta is the same as that of Tencent's advertising business in China. New industry players entering the market and the video traffic becoming shorter have led to weak video monetization capabilities. However, the cost of bandwidth is relatively high, which leads to a structural decline in gross profit margins.

It can be seen that apart from the advertising industry, the biggest marginal change in the expenditure of giants in the third quarter is the further decline of profitability due to the deterioration of cost rates: previously, with their monopoly position, the giants maintained their cost scale effect capacity despite the deterioration of the three expense rates. However, in the third quarter, the appreciation of the US dollar and the rise in resource costs began to have a significant negative impact.

Only Apple and Amazon's North American retail business, among those who do business with C, have relatively stable profitability.

With a combination of a) to d), we can roughly infer the following complete picture:

In this confrontation between the enterprise and employees, due to the labor shortage, the bargaining power of the enterprise has declined relatively. Apart from enduring the rise in energy prices, the enterprise also faces the pressure of labor costs. In addition, successful giants who do business overseas also face the pressure of the appreciation of the US Dollar. From the perspective of employees, what they mainly endure is the upward pressure of commodity prices, which is at least two layers less than the pressure on enterprises. And after the significant decline in corporate profitability, expenditure reduction was initiated. Advertising and public cloud expenditures (where advertising is an expense and public cloud is a capitalized investment, corresponding to the private investment contraction in GDP) are both external expenditures with variable elasticity, and the platform economies of the Internet advertising and public cloud service platforms examined by Dolphin Analyst have felt the pressure of rising enterprise costs first.

III. How much longer can American residents "hold up" their spending?

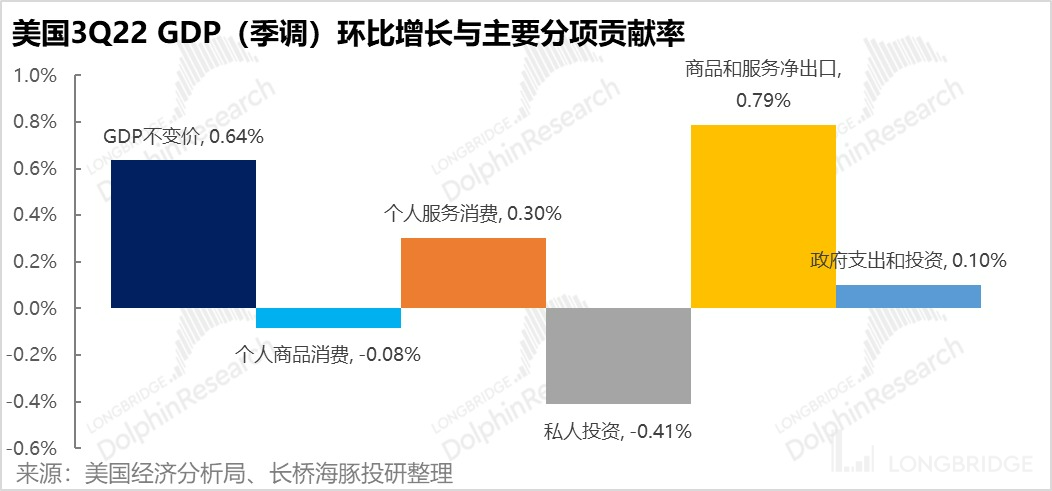

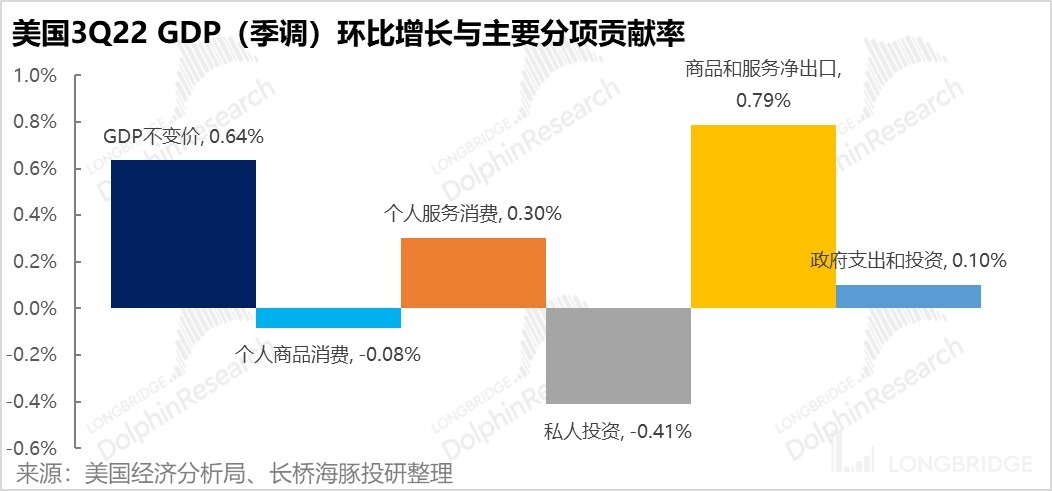

At this point, it is clear that, among the core pillars of economic growth, namely, resident consumption, corporate investment, government investment/consumption, and net exports, without considering external demand and countercyclical government investment/consumption behavior, true endogenous natural growth is mainly left with resident consumption. Next, let's take a look at how much momentum remains for resident consumption.

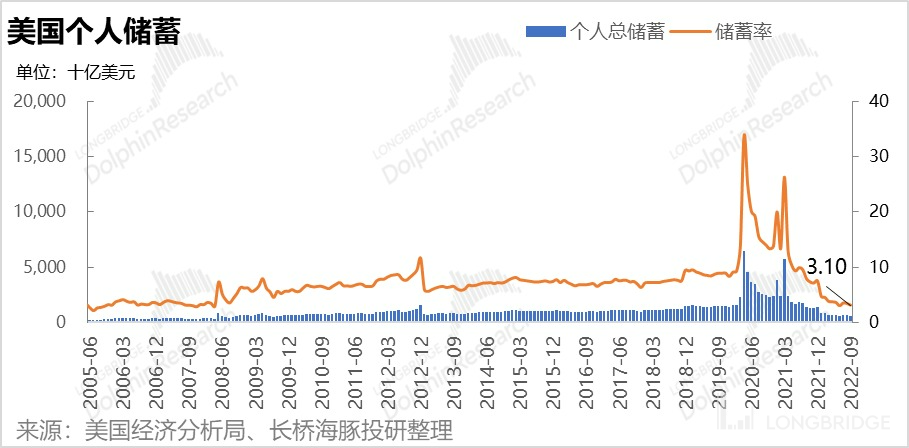

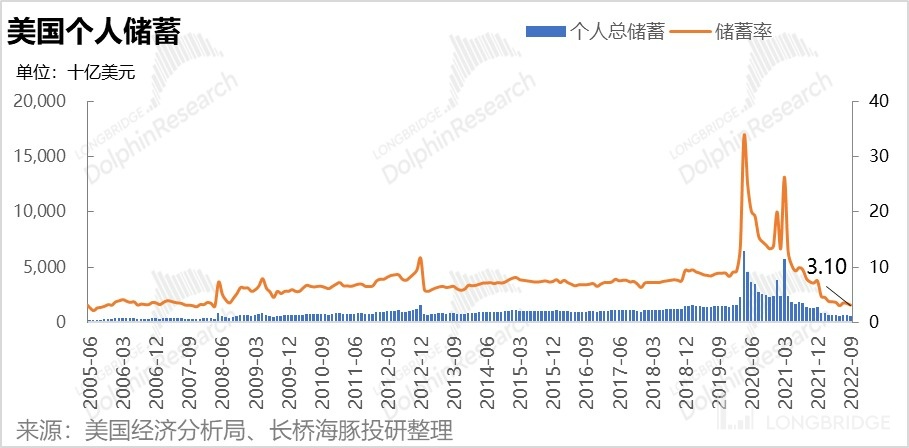

1) "Emptying" pandemic savings

As of September, it can be seen that American residents have basically emptied their excess savings from the pandemic, and the savings rate (savings/disposable income) has fallen to pre-2007 levels.

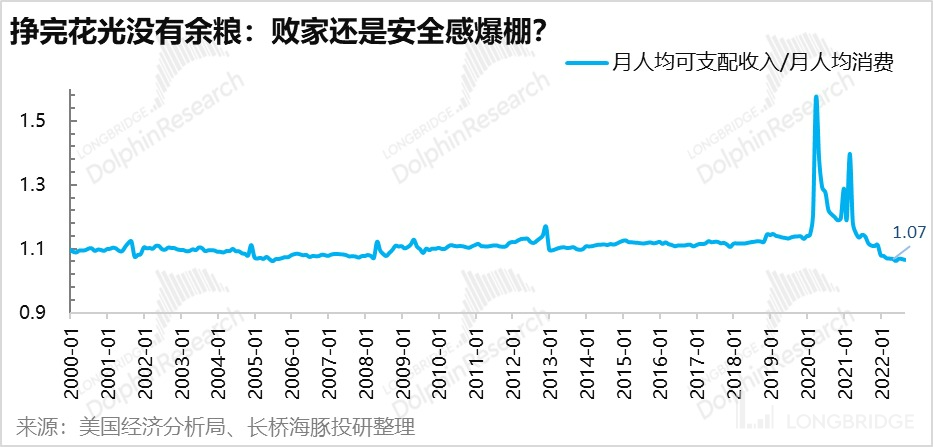

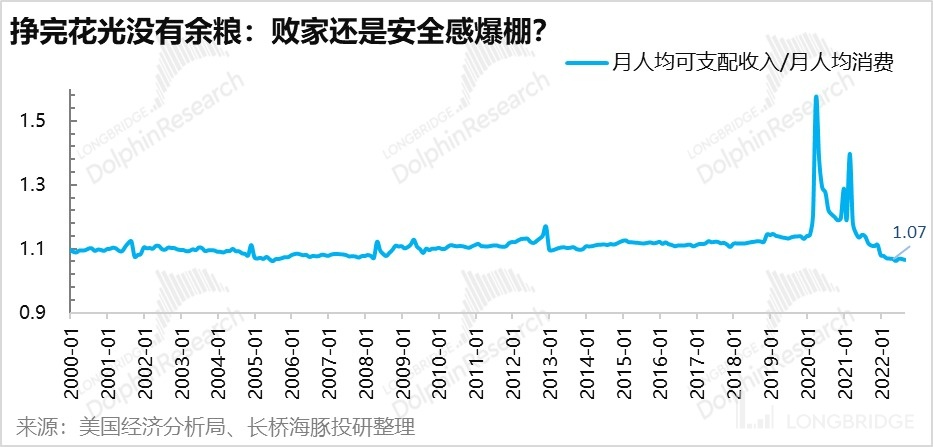

2) Earning all and spending all, with no spare change

From the perspective of per capita disposable income and monthly per capita consumption, the average monthly income that Americans can dispose of (including social security contributions) is less than $4,700, while they have to spend more than $4,400, leaving themselves very little spare money. Similar proportions between income and spending - both so low - were last seen in around 2007.

3) Spending tomorrow's money? With no spare change and rising costs, how long can they hold on?

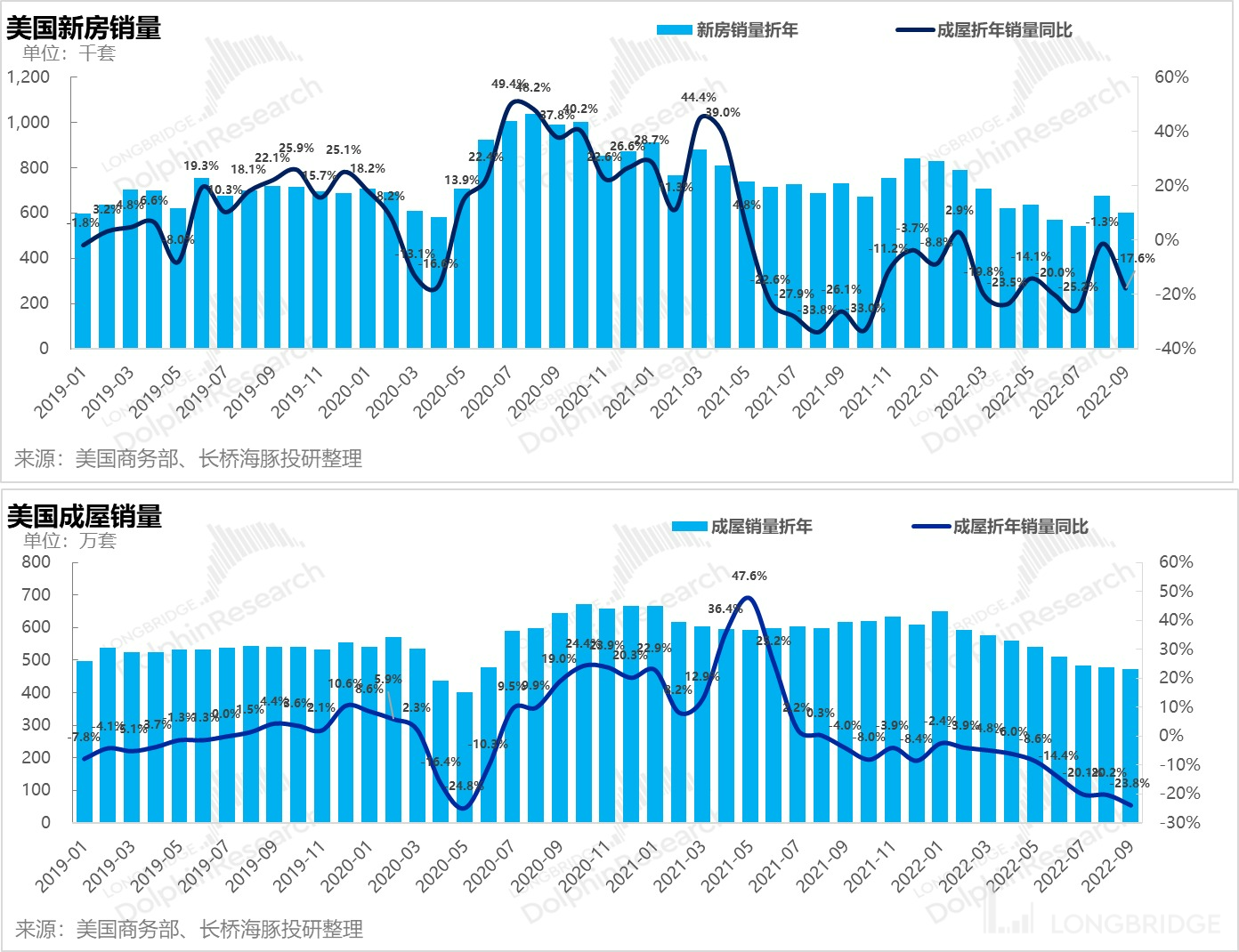

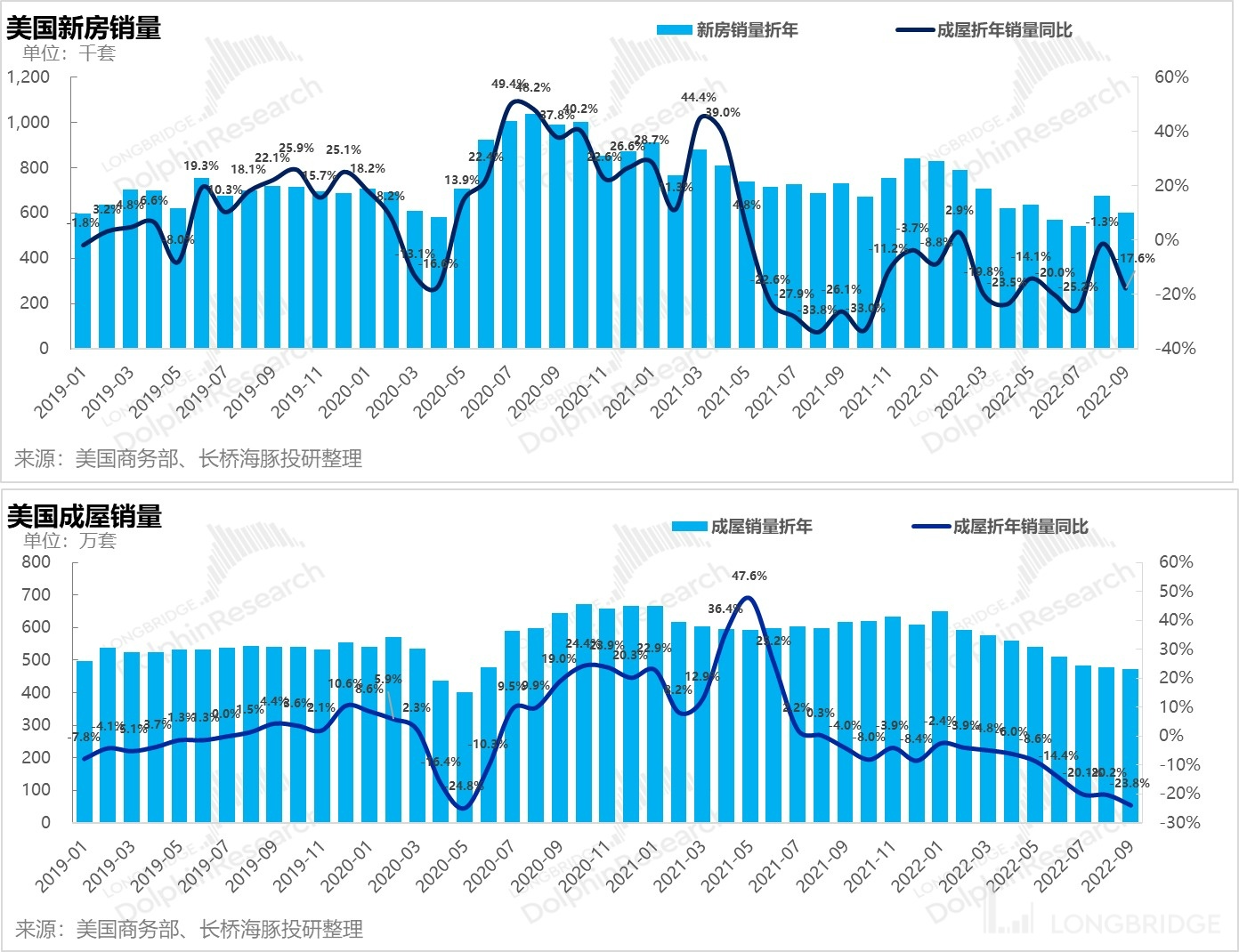

In terms of overdrawing future consumption, let's look at the two main items: home mortgages and consumer loans. The housing sales market seems to be cooling down soon, but consumer loans are still strong. Let's take a look at house prices first:

a) Housing prices are holding up: As of September, new housing prices in the United States are relatively stable compared to the same period last year, while sales prices for second-hand homes have shown a downward trend on a month-on-month basis.

b) Housing sales volume is declining: Both existing homes and new homes have seen a significant decline since September, with year-on-year declines of between 15% and 25%.

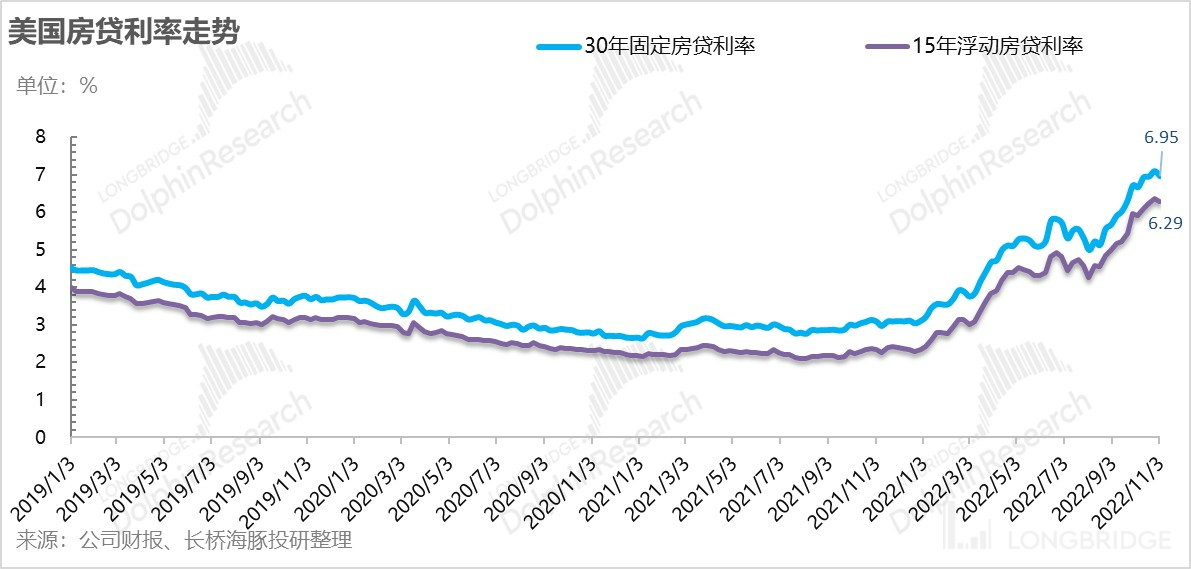

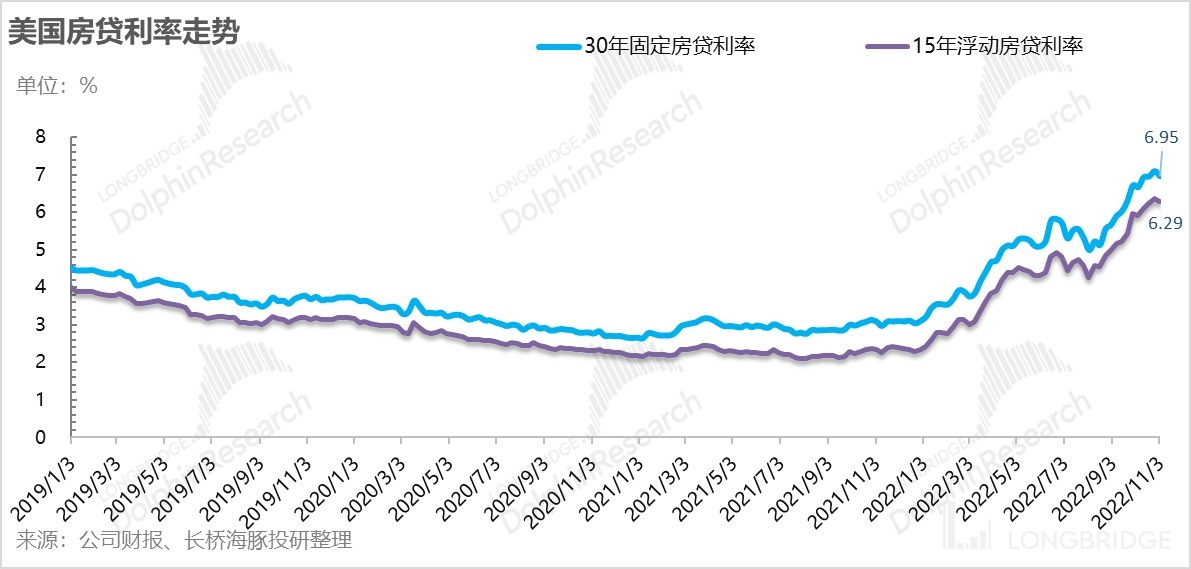

If we look ahead, the current US mortgage interest rate has already surged to 7%, and with further rate hikes, the mortgage interest rate is highly likely to reach over 8%, which will directly cause home buyers to back off, and the real estate market is likely to cool down.

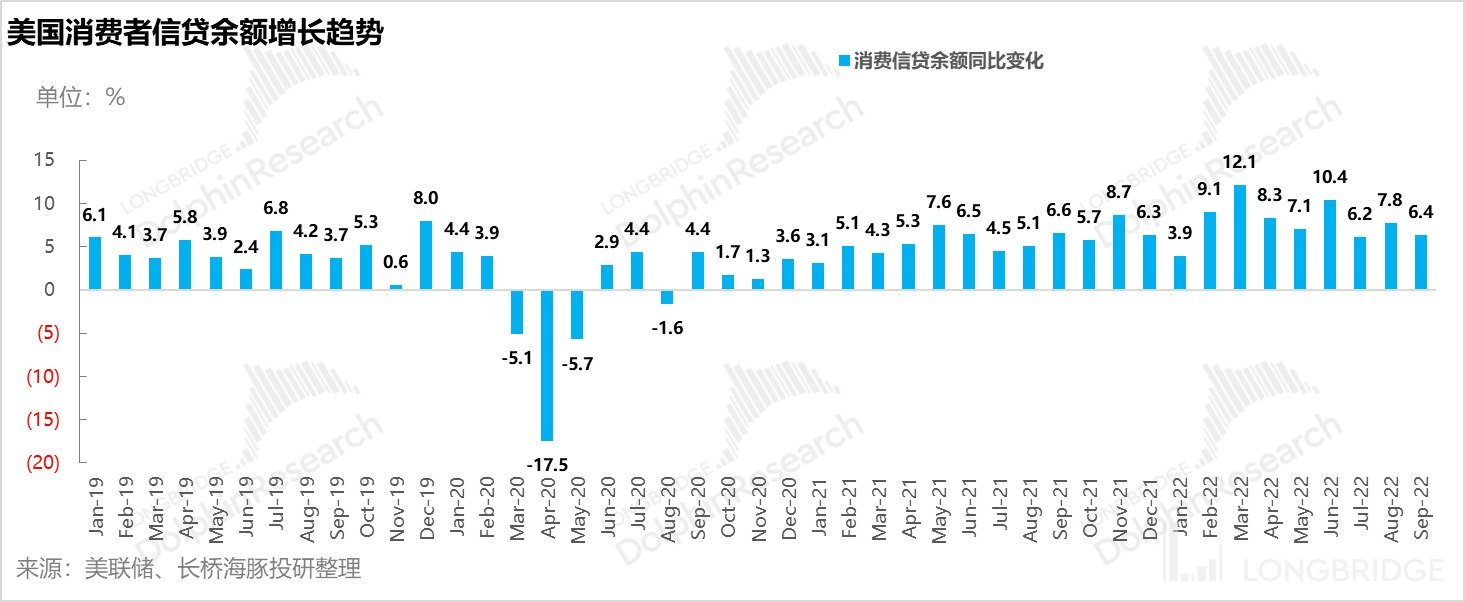

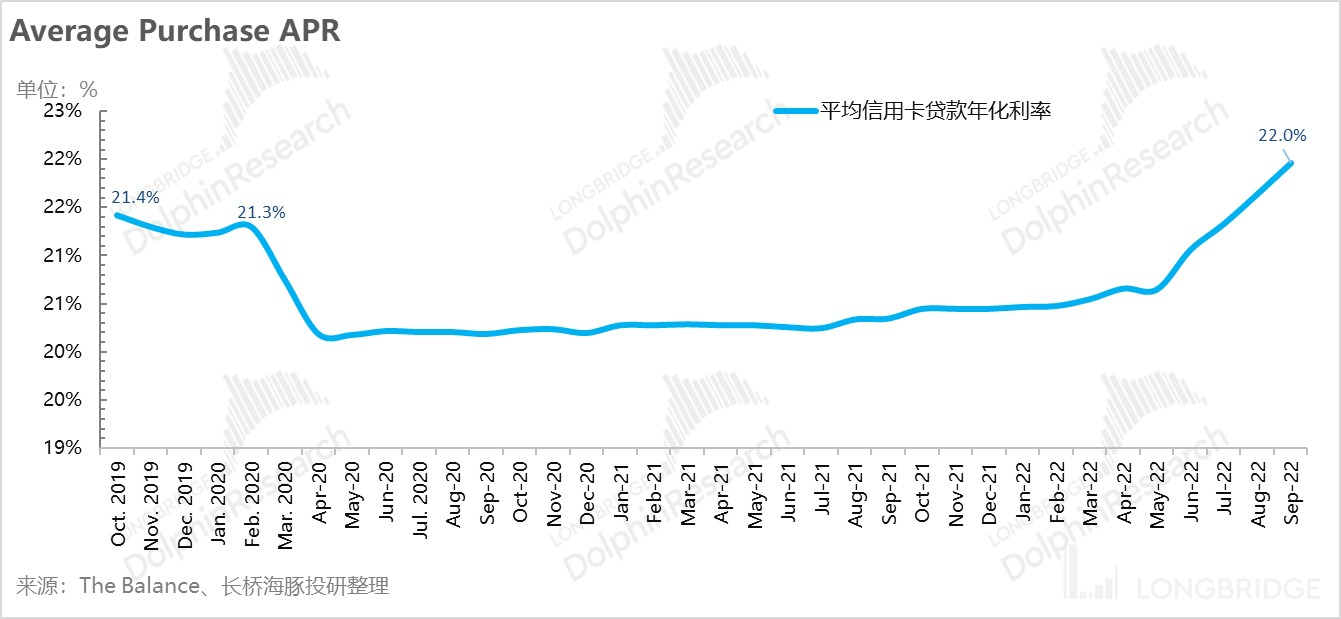

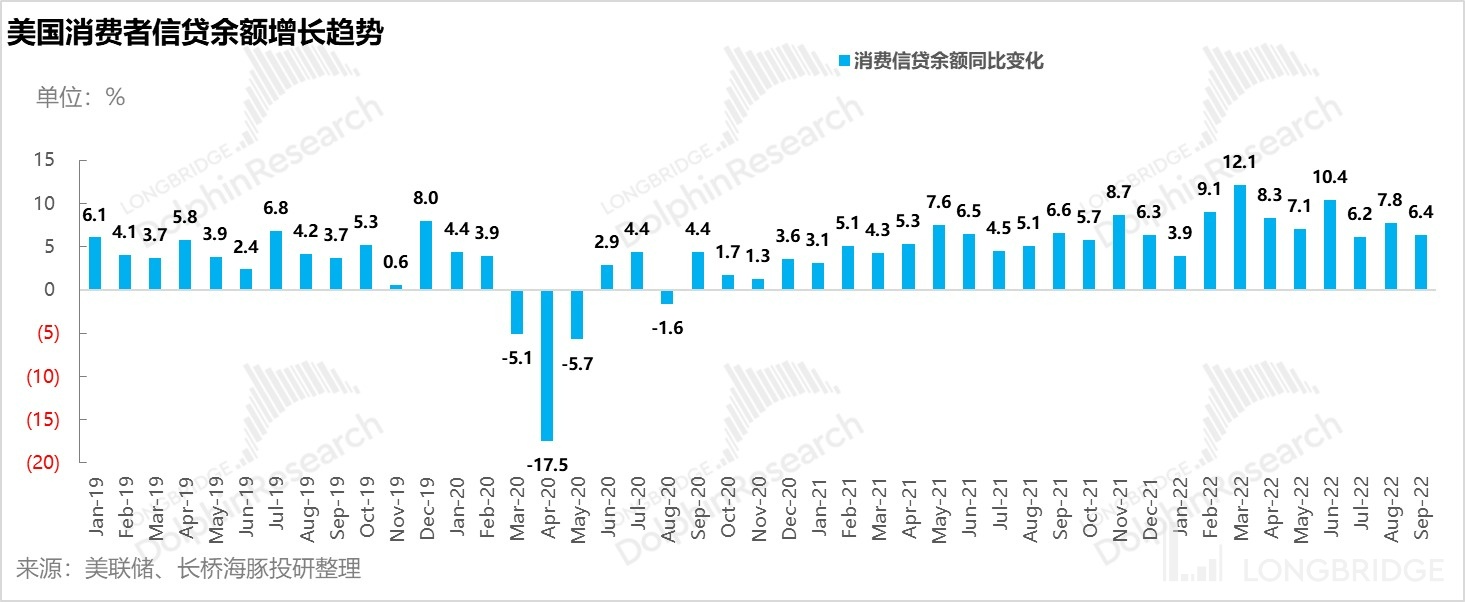

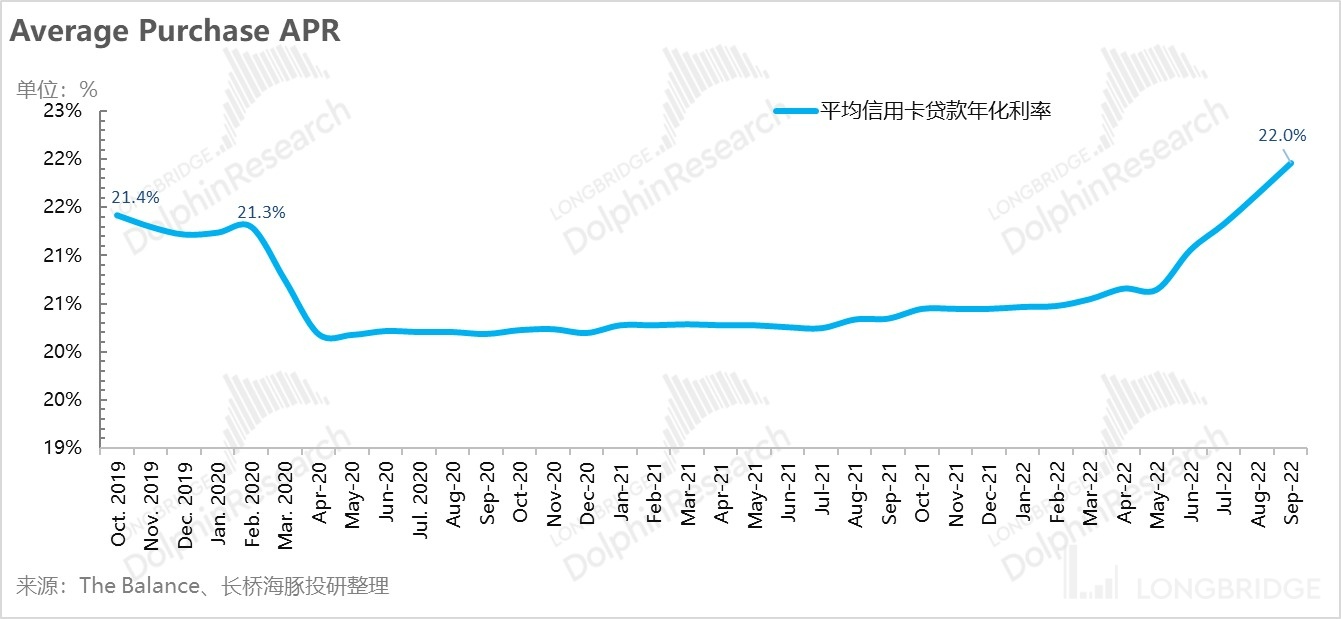

Looking at consumer loans, it seems that the balance of consumer loans in the United States has not been affected as of the end of September, and is still steadily increasing. Although the rate of increase in consumer loan rates is not as high as that of housing loans, the comprehensive annualized interest rate of consumer loans in September has approached 22%, exceeding the pre-epidemic level. In the case of exhaustion of surplus food, how much leverage can residents still consume is a question that needs to be answered.

4) The only source of confidence-never worried about job hunting, what if we meet the archenemy—Federal Reserve?

If we say that the only thing that currently supports residents to continue to move forward is the job market, in the data seen by Dolphin Analyst, it seems that most of the security comes from the booming employment market. For the latest employment data analysis, please refer to "Chinese assets are booming, why are China and the United States in two different worlds".

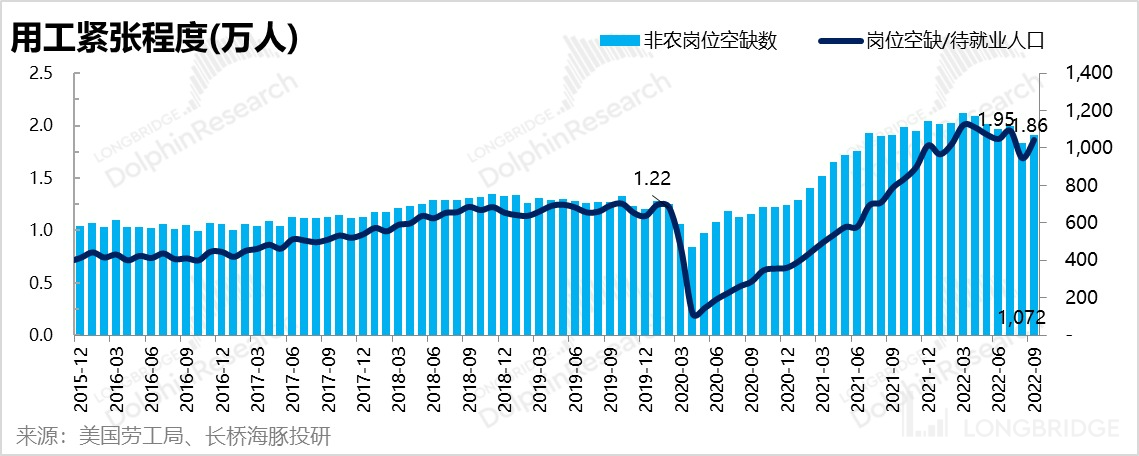

It can be seen from the data in October that the only contradiction that can be felt in the employment market is the rise in net unemployed people (high entry and high exit) under high employment mobility. The unemployment rate has risen slightly from the historical low point to 3.7%, which is far from the expected unemployment rate of about 4.4% by the Federal Reserve.

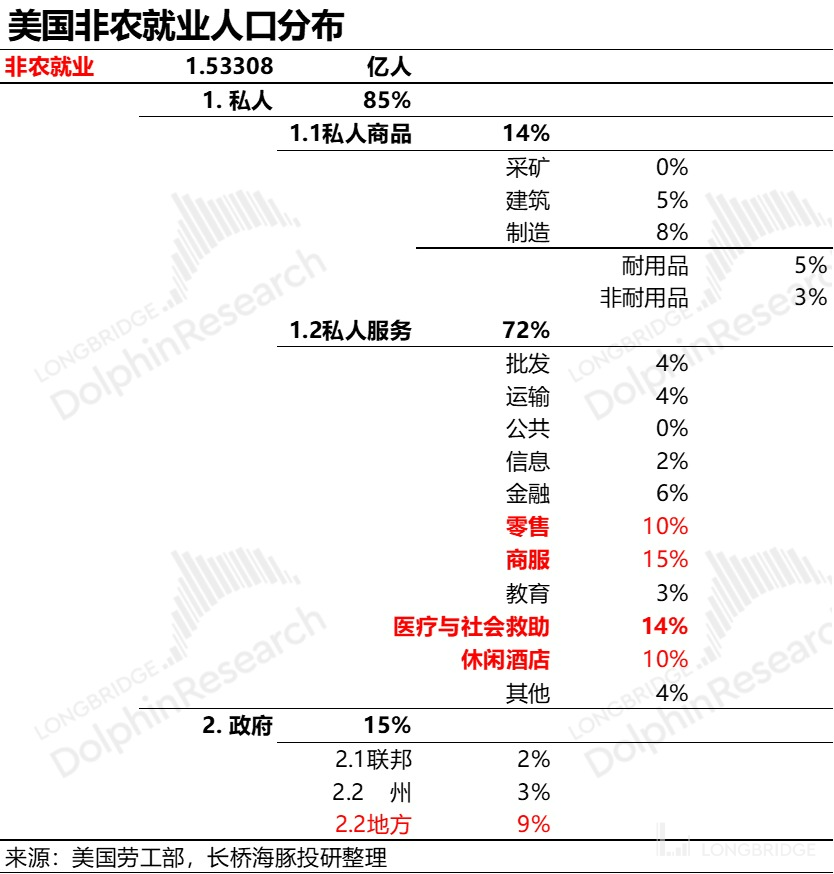

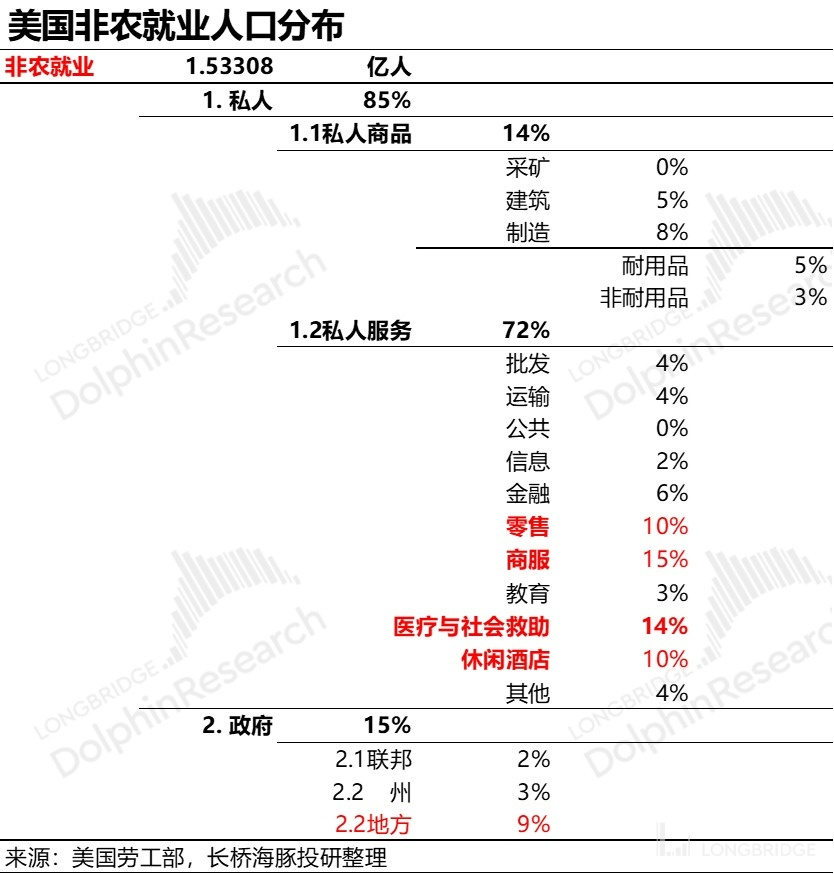

If we delve into the supply and demand contradictions in the American labor market, taking October as an example, let's first look at the industry distribution of non-agricultural employment in the United States. From the perspective of private and government departments, it is clear that the proportion of private sector employment is still about 85%. Private sector is divided into private commodities and private services. Private services account for a large proportion. Among private services, the four major industries with concentrated employment are retail, professional and business services (such as real estate brokerage services, accounting and auditing, IT outsourcing, etc.), medical and social assistance, and leisure and hotels.

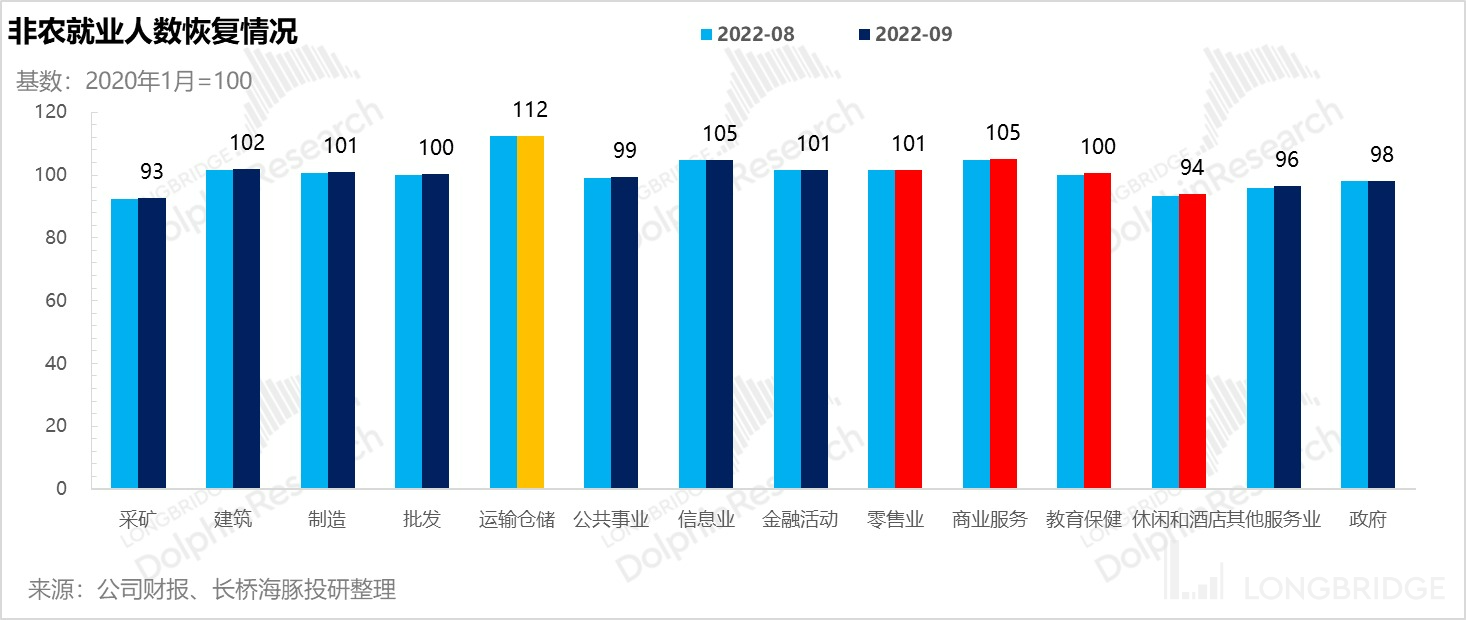

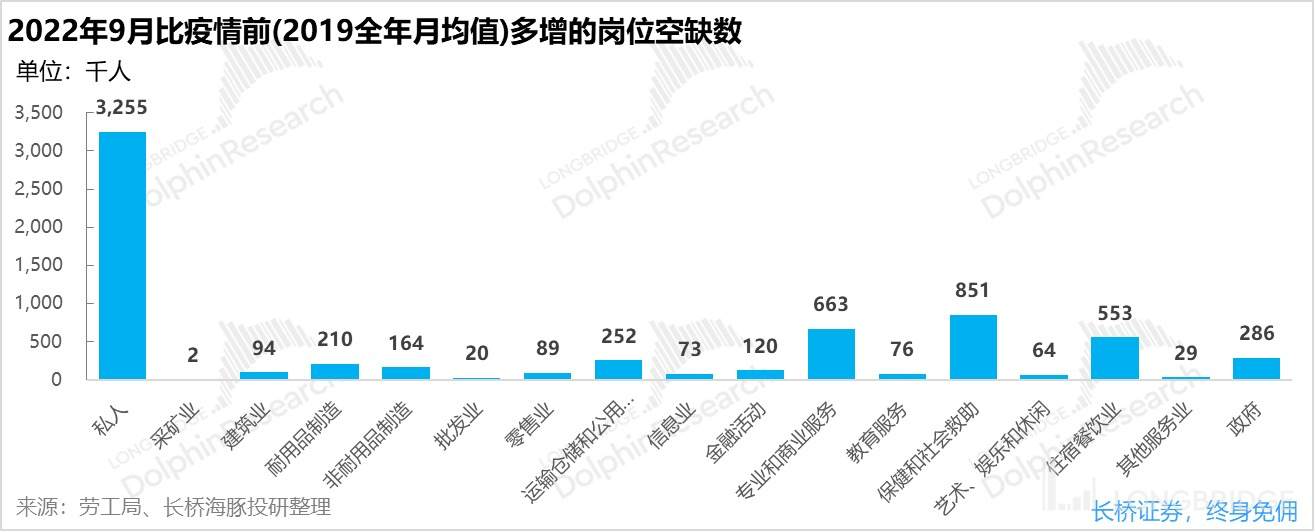

Judging from the degree of recovery of the number of employees in these industries compared with before the epidemic, except for the transportation and storage employment, the number of employees in the other three labor-intensive service industries are far beyond the epidemic level (based on January 2020). Among the four major labor-intensive service industries mentioned by Dolphin Analyst, only the leisure and hotel industry has not returned to pre-epidemic levels. Combining the vacant positions that still need to be filled in these industries, we can see that the core of new demand mainly comes from healthcare/social assistance, professional and business services. Accommodation and catering services are more to make up for the employment population lost during the epidemic. The former two account for 50% of the private sector's new demand after the epidemic.

The significant increase in the number of jobs in healthcare and social assistance is obviously affected by the "aftershocks" of the epidemic. It seems that after the epidemic, people have a higher demand for labor-intensive industries such as medical services and social assistance.

According to Dolphin Analyst's estimate, if the proportion of job vacancies to unemployed persons is adjusted back to the tight balance state before the epidemic (about 1.2), the current number of job vacancies needs to fall from more than 10 million to more than 7 million net, which requires a net decrease of more than 3 million jobs. This decrease corresponds exactly to the three million-plus job demand created after the epidemic.

From the distribution of new job demand, if other industries have a certain amount of "monetary loosening" brought about by inflated demand, to some extent, the demand can be suppressed by raising interest rates, but it seems that healthcare has a heavier essential nature and is not so easy to be suppressed. In other words, the labor supply in the United States is scarce due to both inflated demand and structural changes in demand after the epidemic.

As for the solution to the employment contradiction, hoping to increase the US labor participation rate is basically a slim hope. Although the United States has suspended epidemic subsidies, the labor participation rate has remained basically unchanged since the beginning of this year, and it is still lower than the level before the epidemic. The recovery of the labor force to the level before the epidemic mainly relied on the increase in the total population, and the US population has increased by approximately 2 million people compared to before the epidemic.

Therefore, without significantly opening up immigration or supplementing the supply of US labor, and considering that the labor supply before the epidemic was already in a tight balance state, the current employment contradiction caused by this demand + structural friction can only be solved by other industries significantly cutting jobs to subsidize the additional new demand of healthcare, professional, and business services. Only in this way can the unemployment rate be reduced to about 4.4%, which is the Federal Reserve's expectation for 2017.

The significance of the Federal Reserve's interest rate policy is precisely aimed at this: when companies have already felt the economic chill, by raising borrowing costs, they can transfer the chill to residents, reduce the leverage expansion speed of the resident sector, and put interest-sensitive industries, such as the real estate industry, under the "freeze" state through interest rate hikes. By disintegrating the employment demand of these industries, it can alleviate the employment contradiction of healthcare and other industries in a curved manner. And combined with the real estate sales situation shared by Dolphin Analyst, the real estate industry should have felt the chill first. Under the current situation where the mortgage interest rate has soared to 7% and is further moving towards 8-9%, it is meaningless for residents to buy houses with leverage in the current residential area. After the real estate market cools down, the largest proportion of CPI and the main item driving the current CPI surge-residential prices-downward is only a matter of time.

Overall, if we put the aforementioned 1) -4) together, we can see such a picture:

a). From the perspective of residents' consumption, such as "surplus grain" (excess savings), consumption potential of immediate income (disposable income has reached its maximum in terms of consumption expenditure, and further increasing spending may require borrowing for consumption) and rising costs of borrowing for consumption, there are obvious flaws in further driving economic growth through residents' consumption.

b). Currently, the only insurance item for residents' consumption-"no worries about finding a job". After the benchmark interest rate rises to 4-5%, the employment demand pressure of interest rate-sensitive industries will increase significantly, which will alleviate employment contradictions to a certain extent. However, under structural employment friction, the situation of high employment and high unemployment in the US employment market may need to persist for a long time:

As Dolphin Analyst said, if there is a need to reduce net employment demand by 3 million, even if it is necessary to reduce 500,000 people per month, it will take six months; if it is 300,000 people per month, it will take 10 months. However, since 2010, the US employment market has never experienced a continuous decline of 300,000 people per month for half a year. This level of layoffs may require a crisis that matches it to be solved.

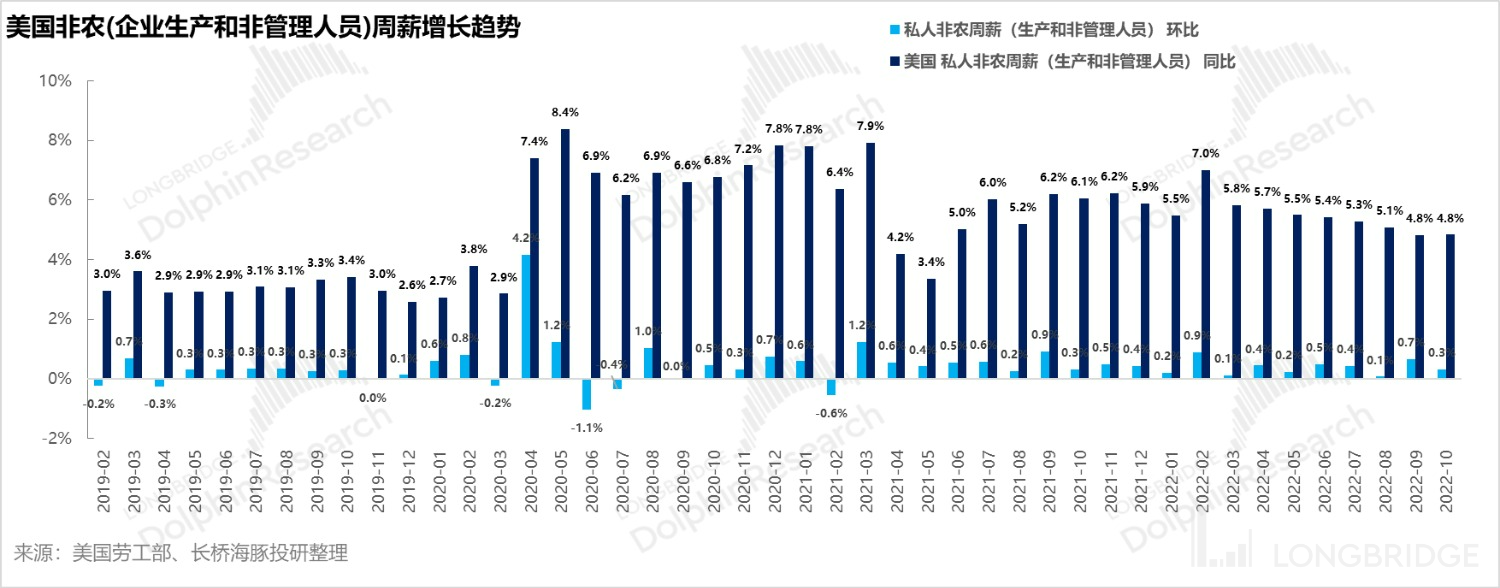

If this contradiction is not solved, in the composition of price elements, labor costs (which have been growing positively on a month-on-month basis and currently have a year-on-year growth rate of about 5%, which is basically consistent with core PCE) will probably continue to rise at a growth rate of more than 2.5%, and it will be very difficult for CPI to be pulled back to the neutral level of 2%.

During this process of labor supply and demand rebalancing (it will take at least six months according to employment contradiction data), it may be difficult for labor salaries to go down, leading to a need to maintain interest rates at high levels for a long time.

Dolphin Analyst noticed that some people in the market expect the benchmark interest rate to loosen in the second half of next year. If the final labor balance starts in half a year, Dolphin Analyst tends to be optimistic about market expectations. After the interest rate rises to the top, the stagnation may still be maintained for a period of time.

At the same time, the core of this employment balance is actually the industry transition of the employed population under the premise of the constant labor pool: after the personnel in the real estate service industry are transferred, coupled with the release of residents' consumption potential, the next marginal deterioration may be in the optional service consumption industry, such as going out for catering, accommodation, optional commercial services, etc. Dolphin Analyst pays attention to the Internet industry. Airbnb and Uber Eats may both have certain risks. IV. Conclusion:

a.) On the issue of interest rate hikes affecting valuations: The three factors affecting interest rate hikes (How Fast, How High, How Long) have already been taken care of. For the degree of height, Dolphin Analyst tends to believe that the market has already priced it in to some extent, and for how long the high rates will last, Dolphin Analyst thinks the market is optimistic.

b.) On the impact of a high interest rate tug-of-war on the market: Unlike the global market in which valuations are being killed as the endpoint for interest rates continues to be raised, the duration of high interest rates mainly affects the expectation of an economic downturn inside the US, which corresponds to the degree of deterioration of individual stock performance in the US. Therefore, after the stage of shrinking liquidity to kill valuations, Dolphin Analyst's focus on the Hong Kong stock market can finally see a big obstacle being removed, with opportunities for the Hong Kong stock market approaching, and there is hope to see a restoration of valuations.

c.) On the extent of the US economic downturn: Dolphin Analyst tends to believe that after high interest rates, under the structural unemployment friction of the US economy, stagnation may continue for a period of time. During this period, the potential for further consumer spending to be released will gradually diminish as optional service consumption choices, represented by Airbnb, Uber, and other industries, face a decline in consumption and deterioration of their fundamental performance. This situation will gradually spread from "to B" business enterprises to "to C" business enterprises, and even to labor-intensive service-oriented enterprises. A situation where income and costs are mismatched (income deteriorates first, and labor costs remain high, followed by layoffs) may occur.

For US stocks that are already configured in Dolphin Analyst's portfolio, Dolphin Analyst will adjust valuations based on fundamentals and expected conditions, optimizing the portfolio. Stay tuned for updates.

Reference to historical articles:

Overview of US Stocks

May 30, 2022. "Can an US economic recession defeat the inflation tiger?"

May 9, 2022. "With enemies on all sides, can US stocks withstand the light version of an oil crisis?"

February 14, 2022. "US stock market carnival is over, too many people swimming naked"

December 3, 2021. "Who will be acquired, and are Google, Meta, and Netflix still in the game?" 3Q22 Industry Review:

On November 3, 2022, the third quarter of US stocks network advertising "Cold air relay race, Google, Meta no amnesty"

Risk Disclosure and Statement of this Article: Dolphin Disclaimer and General Disclosure