Lingpao: After a sharp drop of 30% in listing, is "Redmi version of Xiaopeng" a chance or a scam?

After a period of sedimentation, except for Weixiaoli, the new energy vehicle IPO market has finally welcomed the fourth player- Lean In Auto.HK.

Unlike the overall excited market sentiment when Xiaopeng and IsIdeal were listed, Leaping Run seems relatively deserted: the subscription ratio of retail investors is only 0.16 times, and the final pricing is only set at the lower limit of the IPO range of 48-62 Hong Kong dollars, which is worth 54.8 billion Hong Kong dollars and barely 7 billion U.S. dollars in valuation. But even with such a discount listing, its stock price plummeted more than 30% on the first day of listing today, and fell to 4.5 billion U.S. dollars in one day.

Compared with the current Xiaopeng's 11 billion U.S. dollars, Ideal's 25 billion U.S. dollars, and Weilai's 27 billion U.S. dollars, plus the sales volume of the past two months has continuously surpassed the three first-tier new forces, Leaping Run seems to be miserable. So, where did its problem lie, is there any hope of breaking through, and how to view its investment value?

Dolphin Investment Research focuses on interpreting global core assets across markets for users, grasping the deep value of companies and investment opportunities. Interested users can add the WeChat account "dolphinR123" to join the Dolphin Investment Research community and discuss global asset investment views together!

The Dolphin Analyst will take a closer look:

1. Label One: "Self-Research and Self-Production", But the Contained Gold Content is a Bit Unreal

Different from Weilai's "high-end" electric vehicles, Xiaopeng's "smart" electric vehicles, and IsIdeal's "high-end extended-range" electric SUVs, the two labels of Leaping Run are probably "self-research and self-production" and "price butcher." Self-research and self-production are self-adhesive for the company, and the price butcher is the user's perception.

First, let's take a look at what the so-called self-research and self-production has really self-researched and self-produced. Is self-research and self-production a gimmick or really valuable?

1) Be prepared for production first

Although it is a second-tier new force, Leaping Run is not a second-tier in terms of establishment time. It was established at the end of 2015, which is about one year later than Weixiaoli.

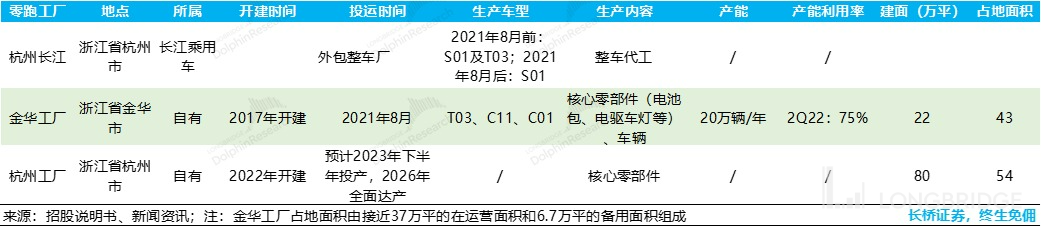

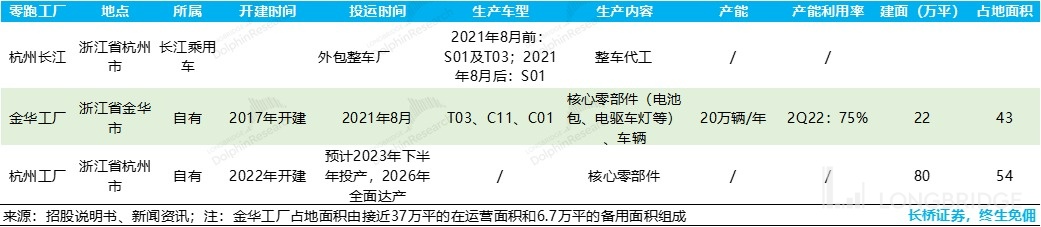

But what sets Leaping Run apart from Weixiaoli is that it attaches great importance to building its own factories, and the factory line is available even before the vehicles are produced. However, although the Jinhua factory was built, the company did not obtain the production qualification for automobiles, so the first car launched in January 2019, S01, after the core parts were produced by Jinhua factory, it was subcontracted to Hangzhou Changjiang Passenger Car Co., Ltd. (already bankrupt liquidation) for production. However, since 2021, the company has acquired production qualifications through a 400 million acquisition. After S01, all models are self-produced.

Currently, there is only the Jinhua factory for production, with a total vehicle production capacity of approximately 200,000 units. In addition to complete vehicles, it also produces core components such as battery packs and electric drives.

In 2022, the company also bought a 540,000-square-meter land in Qiantang, Hangzhou. The plan is to produce core components first and achieve comprehensive production in 2026.

The total construction area of the two places is 1 million square meters, covering an area of 970,000 square meters or 1,500 acres. The long-term capacity planning is basically equivalent to Weixiaoli; according to the company’s sales slogan- sales of 800,000 units by 2025, corresponding to the current 200,000 production capacity, occupying 220,000 building area. The reserve of 100 million square meters of factory construction area can basically match this long-term sales target, but whether the progress of capacity construction matches the sales target is another matter.

2)What has been independently developed?

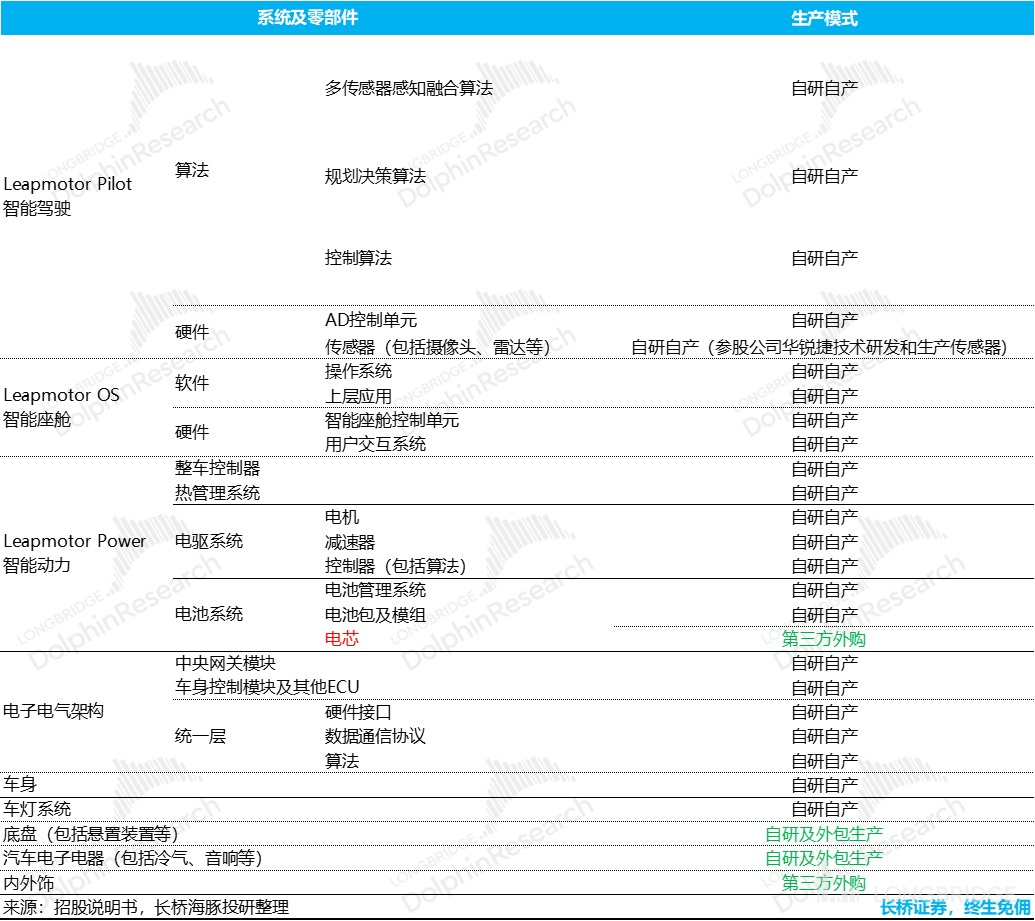

From the three electric systems, intelligent driving to the intelligent cockpit, the company wants to do full-stack independent research and development: for example, the automatic driving algorithm layer is handled by themselves, and hardware on the perception layer is researched and produced through cooperation with Dahua Holdings.

The operating system and vehicle applications on the intelligent cockpit are all self-developed. In terms of the key three electric systems, the motor and electronic control are self-developed and produced, and only the battery system purchases the battery cells, while the rest, from the module, battery pack to the battery management system are all self-developed and produced.

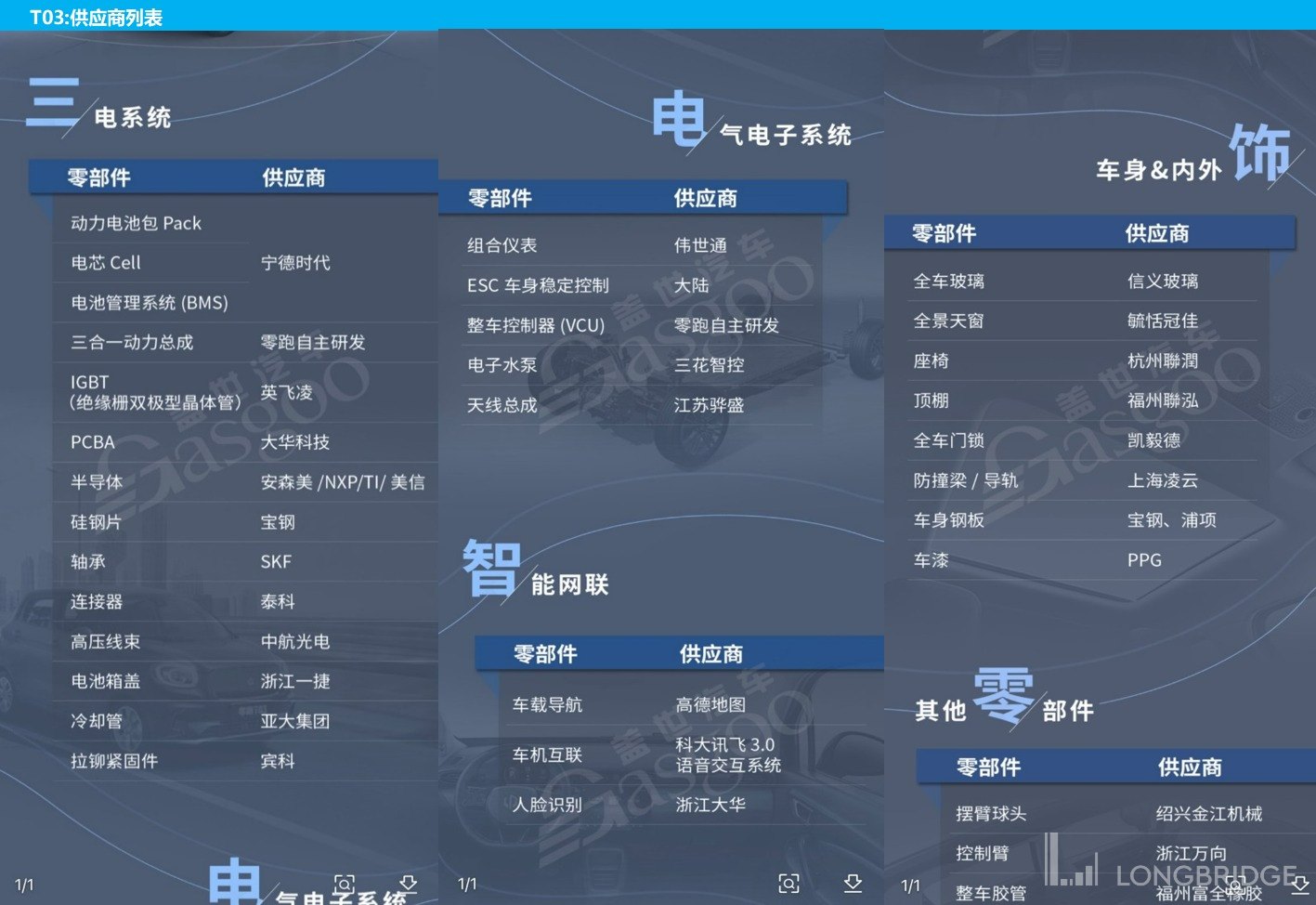

Dolphin Analyst did not find the supplier situation of C11/01, but from the analysis of Laotouleche's T03, apparently the motor and electronic control are self-developed and produced, and the self-development and production of battery modules and battery packs are possibly only found on C11 and C01.

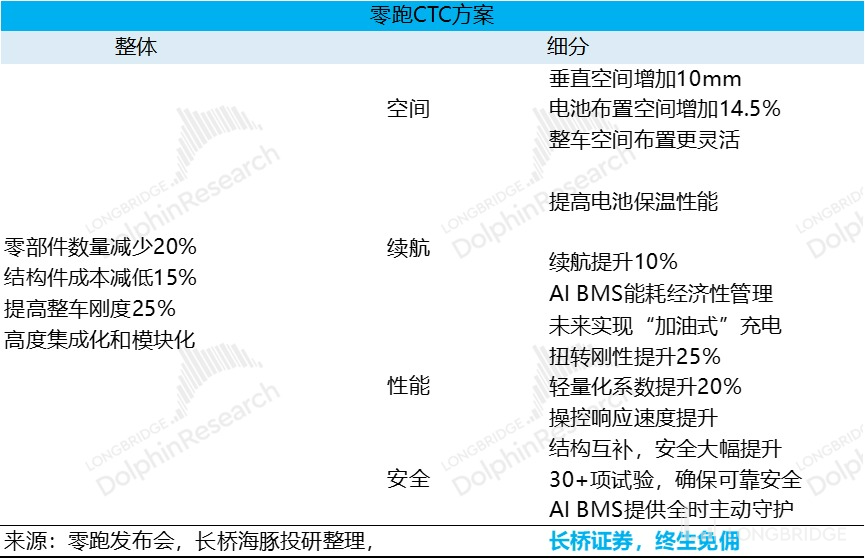

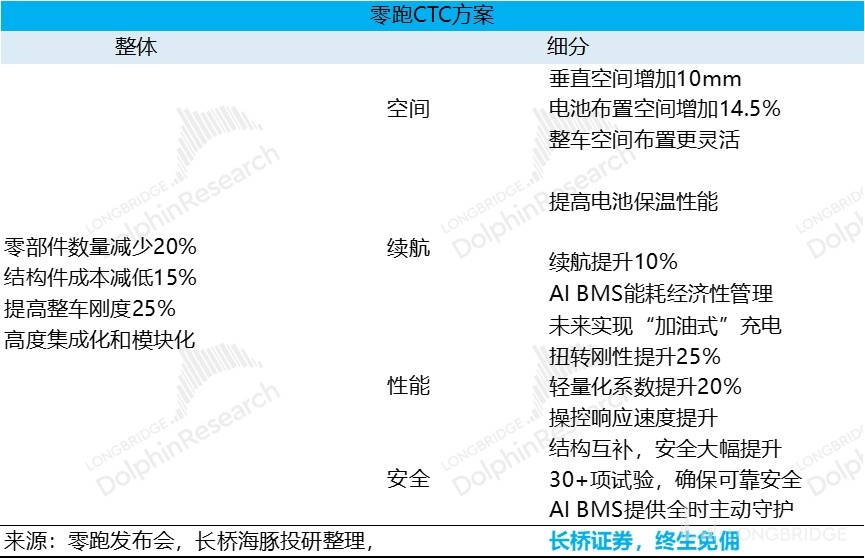

Currently, the most prominent highlight of independent research and development is that in the latest model C01, Leading Ideal still uses its latest CTC (Battery and Body Integrated Technology):

Currently, only Tesla and BYD have launched this technology, but there is a slight difference in the direction of Leading Ideal:

(1) CTC vs MTC? Tesla directly skipped the module link to integrate the battery cells into the battery pack. Leading Ideal did not skip the process of making battery modules from battery cells. It is more like MTC (M refers to the module, not the battery cell).

(2) The installation method is different: Tesla installs the battery pack as a whole onto a chassis that "hollows out" the car chassis to create a battery and body integration; Leading Ideal produces a battery pack without a cover using modules, and then seals the naked battery pack on the chassis of the car with the chassis serving as the battery cover.

Therefore, Leading Ideal still needs to produce modules as a whole, with no extreme efficiency in space release, integration, cost advantages, spare parts redundancy, etc. as found in Tesla.

!

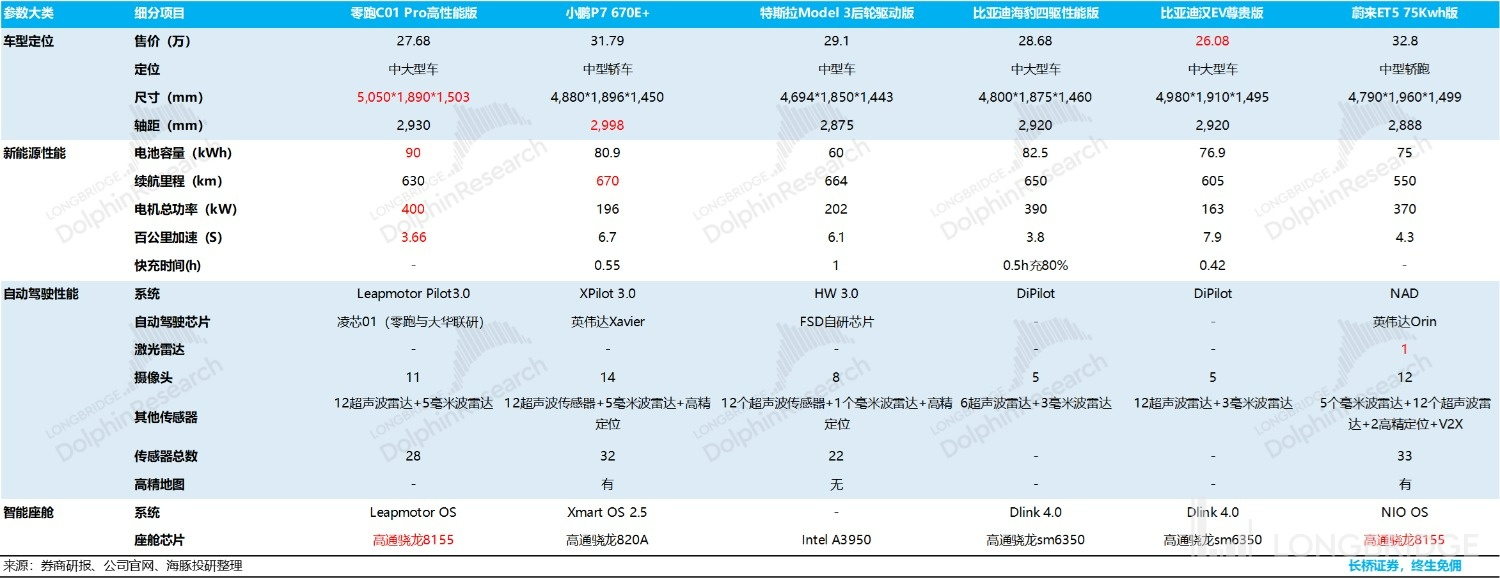

!When it comes to autonomous driving and intelligent cockpits, Dolphin Analyst has analyzed the latest R&D capabilities of Lixiang's new car C01 Performance Edition. The autonomous driving chip is co-developed with Dahua Technology, using the Lingxin 01 chip with only 4.2TOPS of computing power, which is visibly low and relatively common in terms of autonomous driving performance.

Compared with its peers, the intelligent cockpit does not appear to be in a disadvantaged position. It features self-developed LeapMotor OS, equipped with an Android virtual machine that supports Android apps. It also has a T-shaped three-screen display. The cockpit chip is no different from its peers and is mostly purchased from external sources.

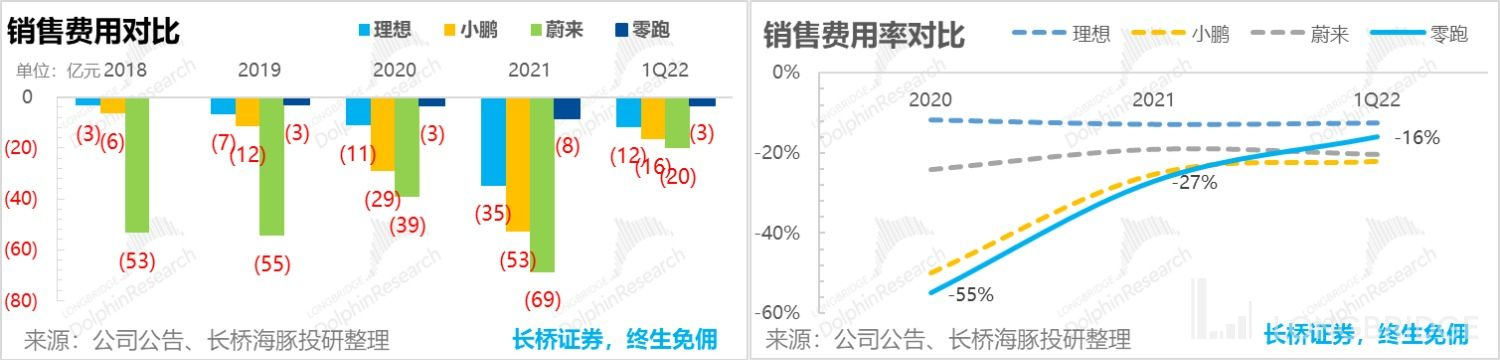

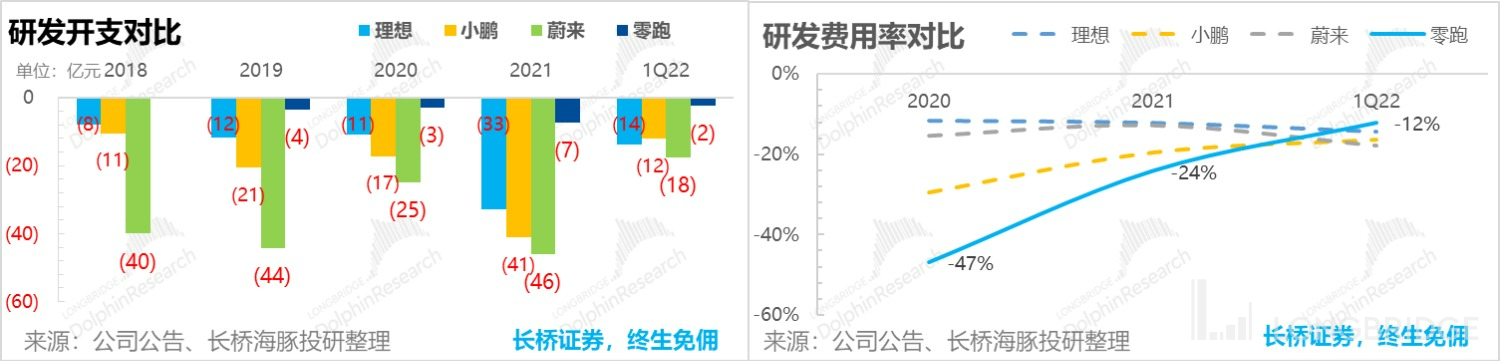

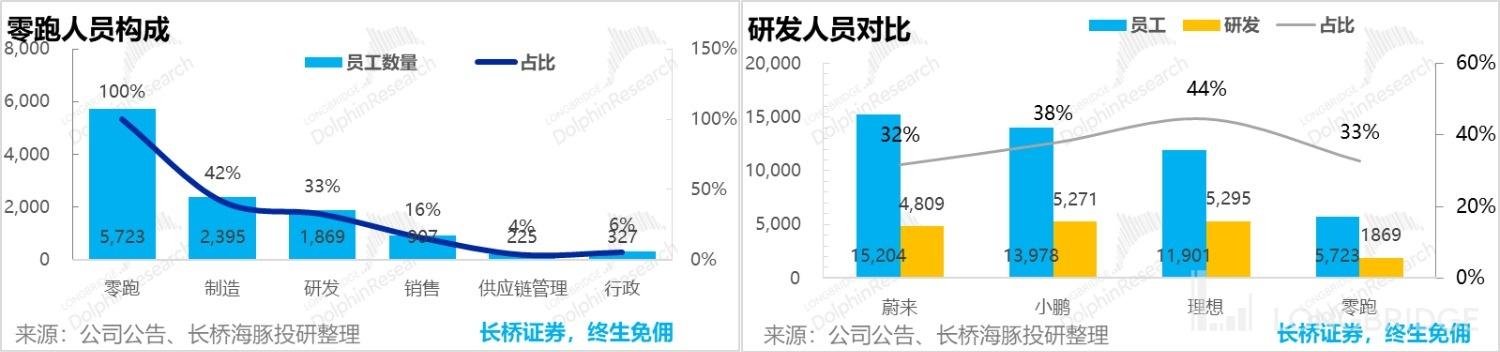

3) R&D investment is somewhat "second-rate"

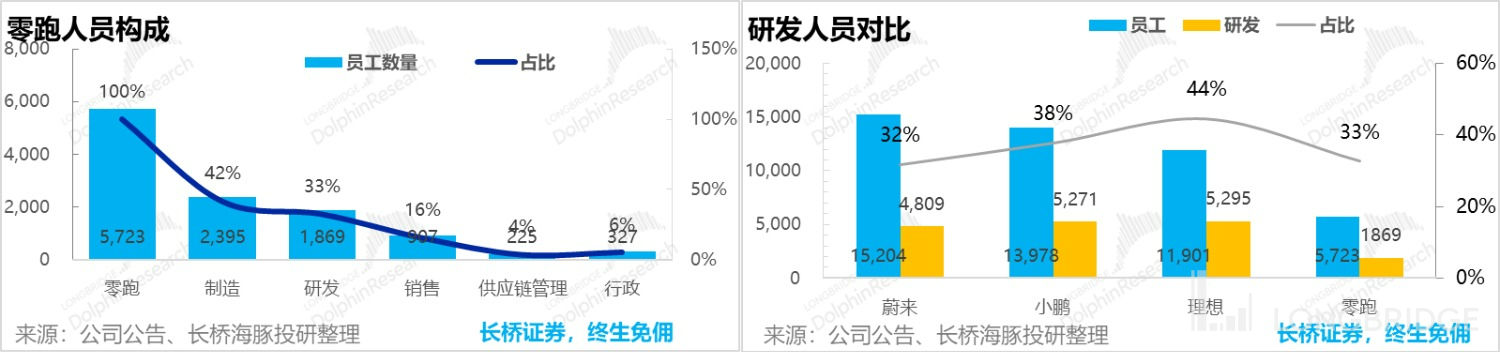

The investment in genuine self-development is related to the amount of R&D expenses and the number of R&D personnel. From this perspective, Lixiang's workforce is clearly that of a second-rate manufacturer, with roughly only half as many employees as Xpeng. This is largely due to the fact that NIO and Li Auto have their own stores, with sales staff accounting for 50% of the company's workforce. While XPeng uses dealerships, the proportion of sales staff is still relatively high.

In terms of product and R&D personnel, Lixiang had less than 2,000 people in the first quarter of this year, far lower than the product and R&D team size of around 5,000 employees at the three leading new forces by the end of 2021. This appearance of being second-rate is quite obvious. Moreover, in terms of personnel structure, Lixiang is more of a production and manufacturing company, with few sales staff but a large number of production personnel, accounting for nearly 50%. By contrast, 50% of Xpeng's personnel are sales staff.

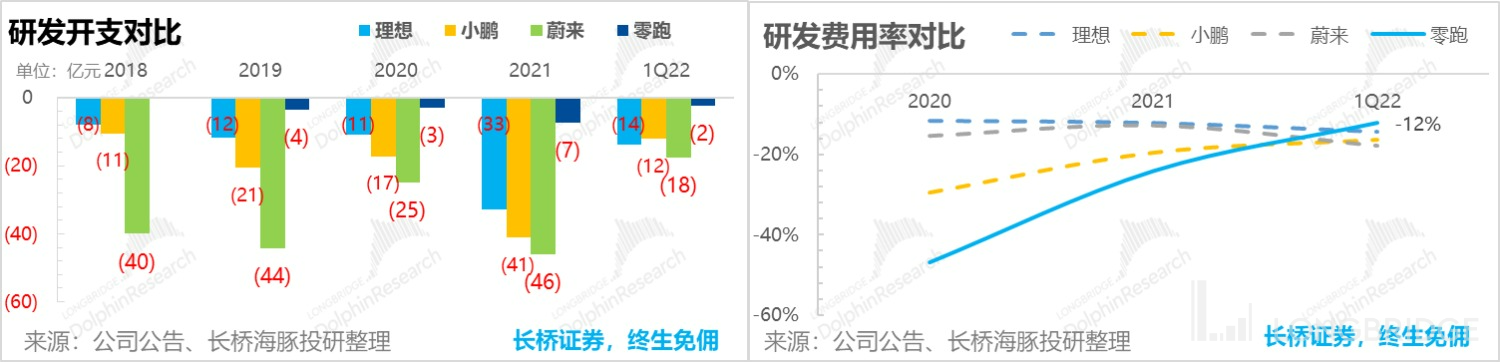

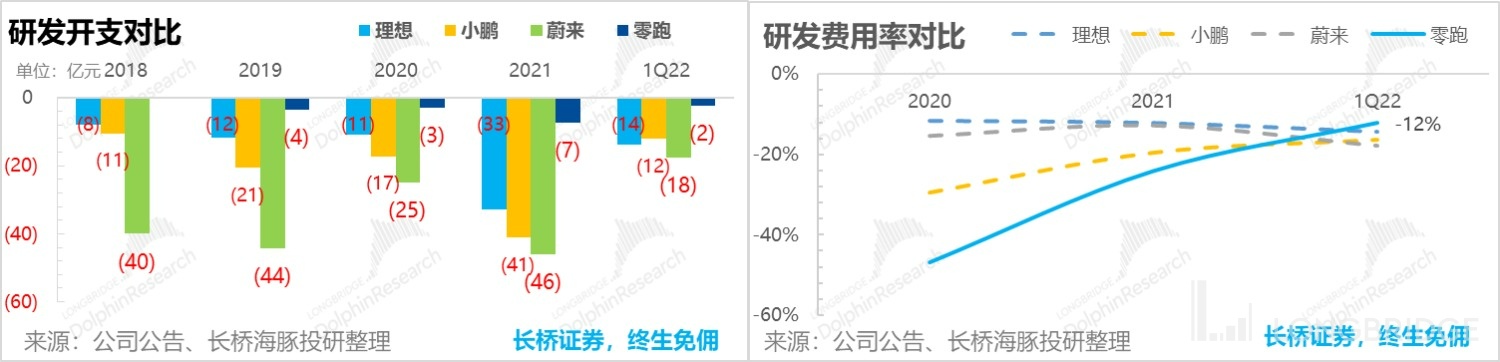

In terms of absolute R&D investment, Lixiang is clearly lagging behind. In the first quarter of 2022, Lixiang only had two billion yuan in R&D investment, while Li Auto, as the least invested among the other three companies, still had 14 billion yuan. Therefore, even though R&D costs are not high, compared to the relatively low income, Lixiang is still at a disadvantage.

Overall, Dolphin Analyst believes that Lixiang's most obvious characteristic compared to its self-development and production is the production capacity brought by its factories. Although the self-production content is still acceptable, self-development is more of a slogan than a reality in terms of both investment and effectiveness.

The three components of self-developed electric vehicles—three electric systems + intelligent cockpit + intelligent driving—are as follows: The motor and electronic control of Lixiang's three electric systems are not identifiable, and the battery mainly integrates the battery cells into the body of the car; autonomous driving is relatively weak, while the performance of the intelligent cockpit is relatively acceptable.1. Sea Dolphin's Analysis on Longbridge's R&D Investment and Staffing

From the perspective of personnel distribution and R&D investment, Sea Dolphin's analysis is confirmed. Longbridge leans toward production-oriented companies. If the company does not "share and divide" the self-developed technology with its shareholder Dahua Group, its investment in research and development is "stingy."

2. Tag Two: How Can Electric Car Companies with Low Prices Rebrand and Gain Traction?

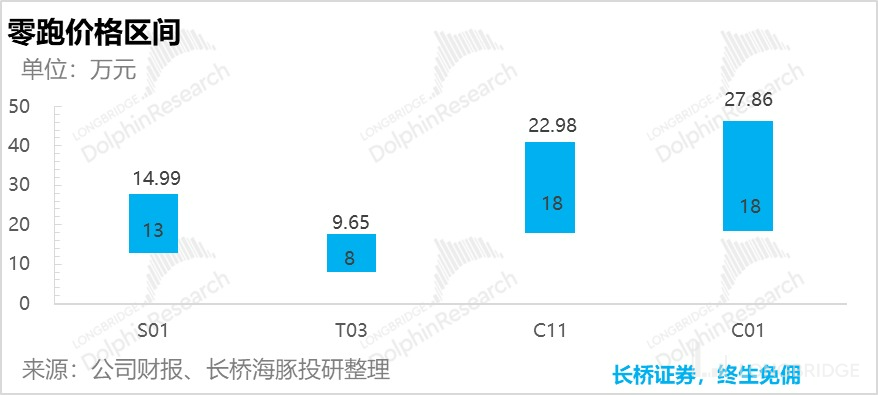

Although Zero Run (ZP) is considered a second-tier new power force, it's not necessarily newer than Weimar Xiaoli, having been established at the end of 2015 - only a year later than them. ZP aims to capture the mainstream car market at a price range of RMB 150,000 to RMB 300,000, which is lower than Weimar Xiaoli's price range.

Moreover, ZP's electric cars aim at "mass" prices, and it has a sales model similar to that of Xiaopeng, involving a combination of direct sales and franchises. Dealerships are major players, accounting for more than 90% of the entire business.

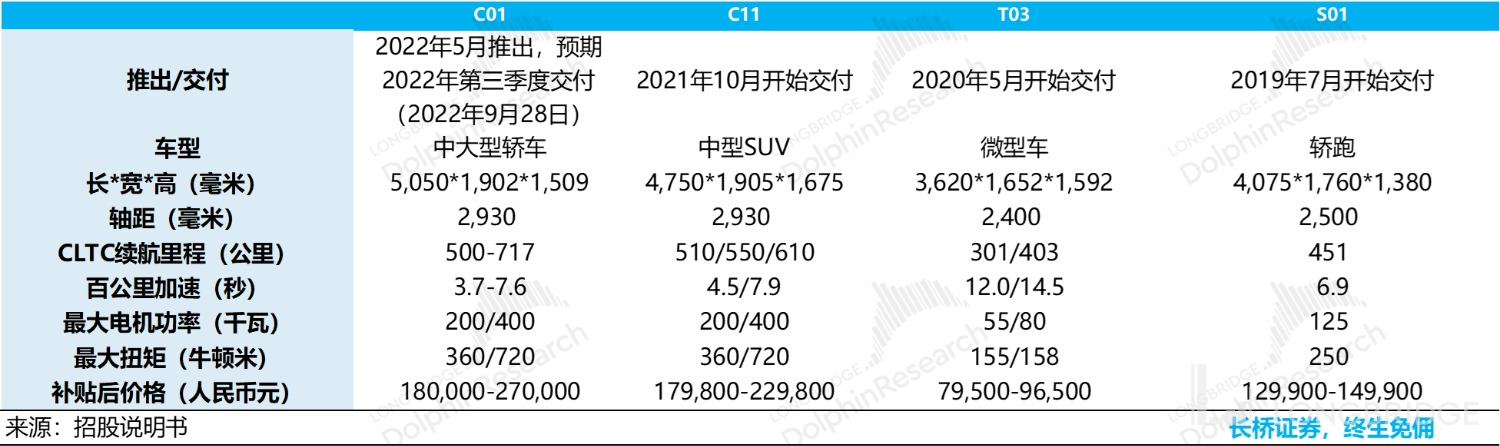

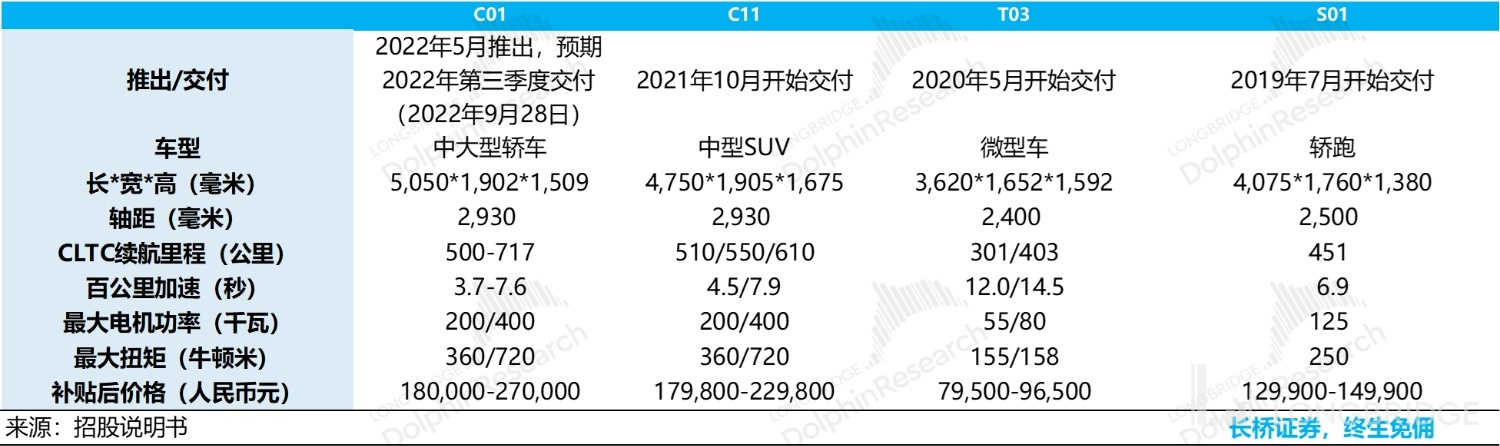

1) S01- A Trial Failure Toward Self-Reliance: The first vehicle, S01, was released in early 2019. ZP was established at the end of 2015 but took four years to release its first car. Due to the emphasis on self-reliance and self-production, and because the first vehicle served more as an experimental item for supply chain management, the S01 was a test item more than anything else.

Moreover, this car was not manufactured in-house; at that time, Zero Run did not have the qualifications to manufacture complete vehicles. It was instead manufactured by Hangzhou Changjiang Passenger Vehicle Co. Although it was not a successful model, it did not result in a complete failure.

Looking at the company's financial situation in 2019, it is evident that the launch of this car was somewhat hasty because the company was in dire straits, thanks to the unsuccessful sales of this vehicle. The company's financial statement illustrates that it was in a state of financial duress in 2019, with only RMB 400 million in cash and short-term investments, while it owed RMB 1.1 billion in long-term borrowings and RMB 200 million in short-term borrowings.

In the early stages, due to a lack of funds, the company's production of electric vehicles took too long. The core reason for the unsuccessful launch of the first vehicle was almost premature termination.

2) T03 - A Reluctant Expedient on the Road to Self-Reliance: Based on Sea Dolphin's observation, ZP's S01 failed, its balance sheet was almost empty by the end of 2019, zero equity financing was obtained in 2020, and only through borrowing could it maintain its cash flow. Furthermore, the company's newly planned seven cars were not slated to launch on the T-platform prior to 2025. Therefore, by selling the T03 vehicle in May 2020, the company's main goal was likely to extend its funding lifeline. Only by increasing sales figures could it continue to engage potential investors and secure funds in the primary market. Additionally, the T03 could help the company recover lost cash flows, which would otherwise be dwindling since the company has been sinking funds into its pursuit with no return.

Because its core goal is to boost sales figures, the T03 was the first micro-car in China to implement ADAS and AI voice assistants, among other smart features. It could also last longer on a single charge compared to its competitors like Hongguang Macro and Ora Black Cat.

However, despite its strong sales, the T03 did not cover the cost of raw materials required to produce it, and the company suffered a gross profit margin of -51%.

In 2021, the company underwent rapid financing after the strong sales of this car, raising over 10 billion RMB in four rounds of financing from the start to the end of the year.

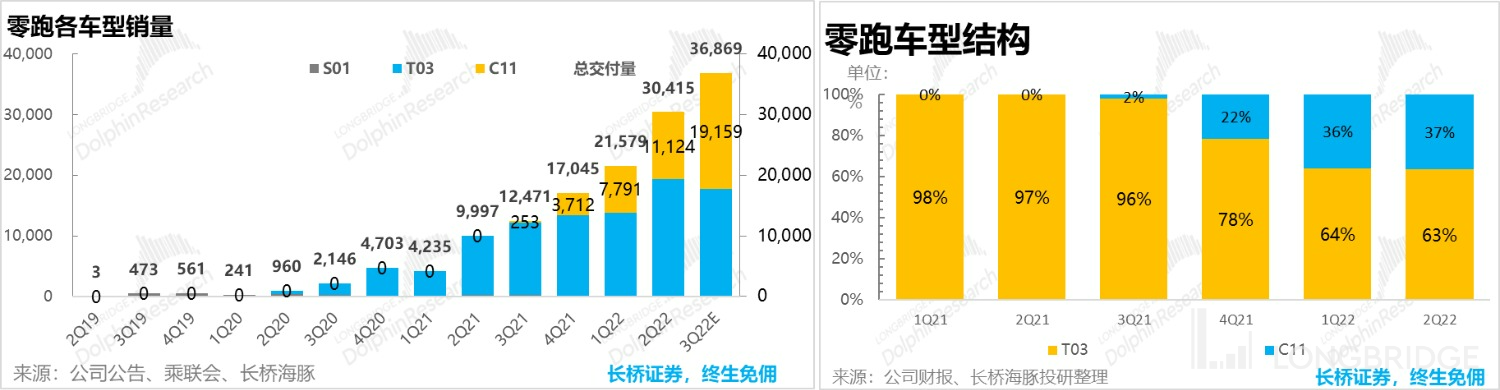

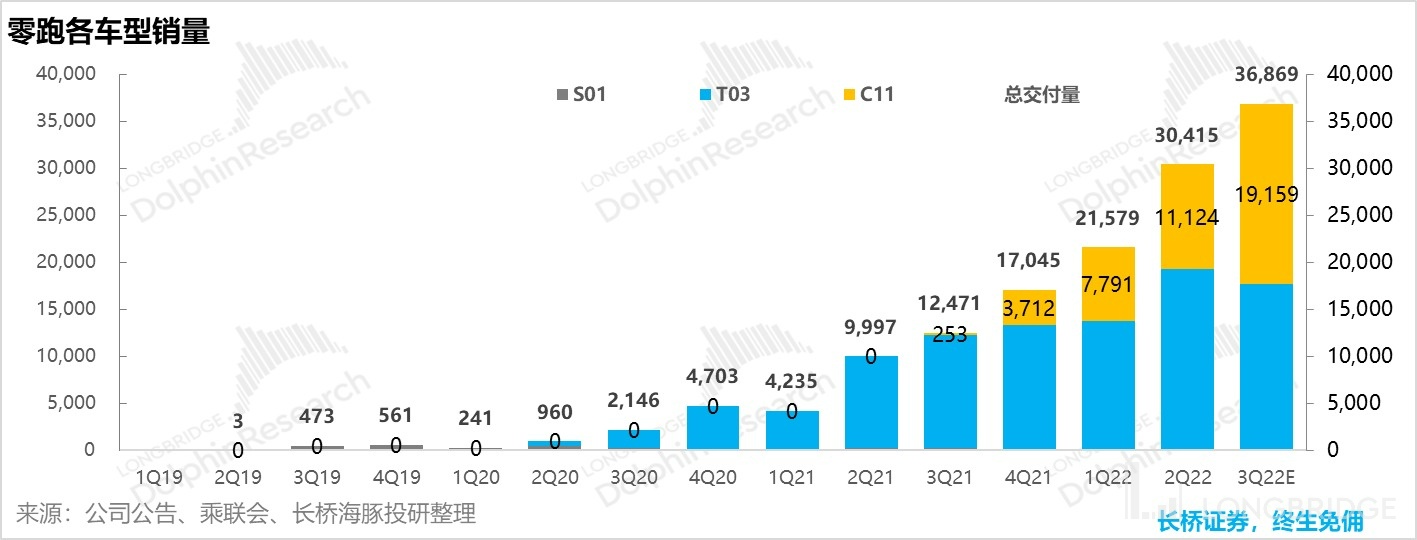

3) C11: The First True Car from Leapmotor

After the T03 sustained the company for a while, Leapmotor finally released their first vehicle within the defined target price range at the end of 2020, namely, the C11. It is a highly cost-effective pure electric SUV in Dolphin Analyst's opinion.

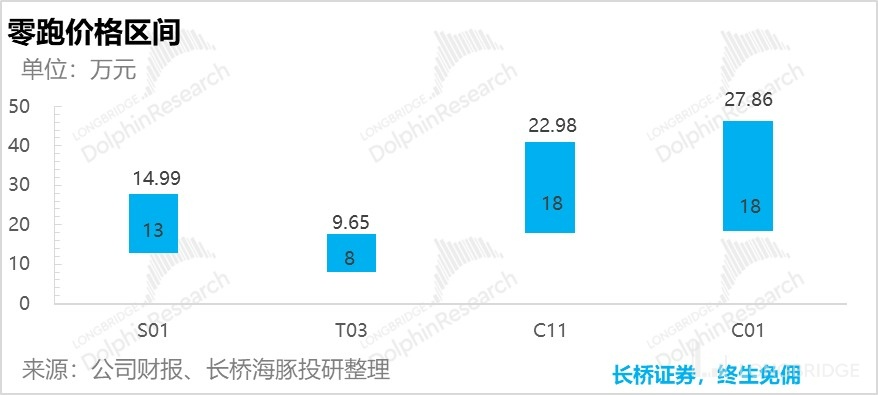

The configurations for this car range from basic to top-of-the-line, with the only difference between them being the number of engines and batteries. In terms of features, intelligent cabins and automatic driving are standard, and it is priced between 180,000 and 230,000 RMB, making it significantly cheaper than the minimum pricing of its competitor, Xpeng's P5.

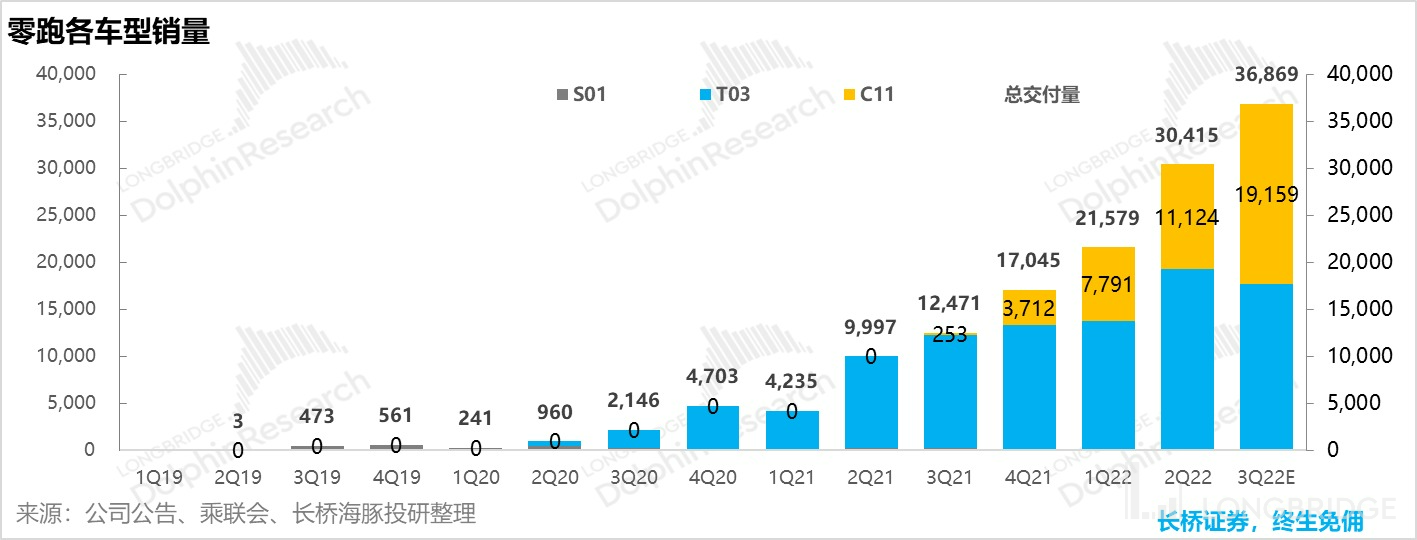

It took a long time to fulfill the orders of this vehicle since pre-sales began in late 2020, and only began delivery in October 2021. Combined with the customer prepayments surging from 40 million RMB to 500 million RMB by the end of 2021, it appears that the supply chain management is having difficulties, with production capacity being underutilized due to a parts shortage.

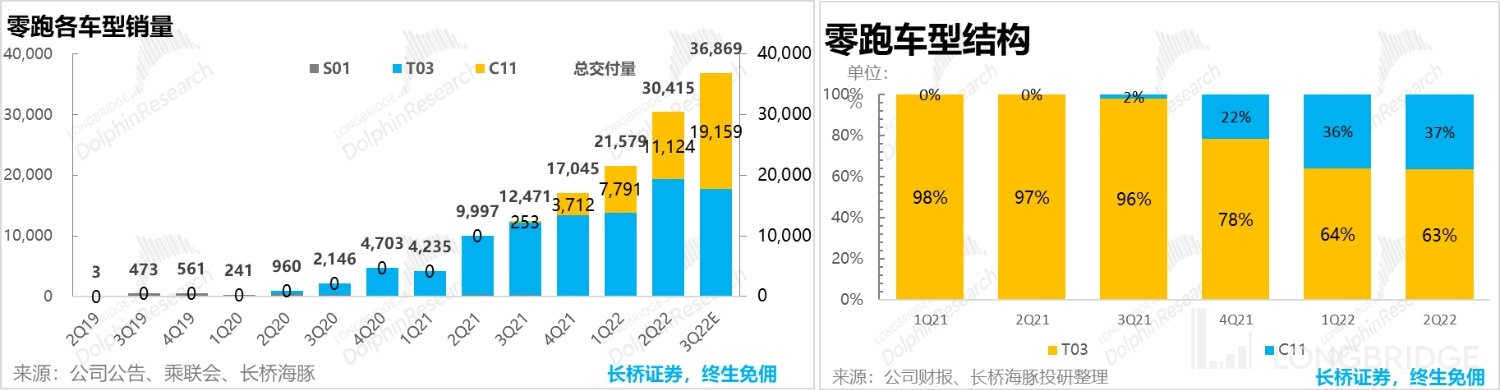

However, it appears that C11 is quickly catching up with the demand, with delivery numbers exceeding 6,000 units per month in July and August 2022.

Regarding the company's latest deliveries in August, the S01 has already been discontinued, and the new C01 has yet to be delivered. As of August, the company has only delivered two models, the T03 and C11.

The sales volume of the company has exceeded 12,000 units per month, with the C11 being the only model that is truly valuable in terms of valuation, with sales exceeding 6,000 units per month.

From a review of the company's car models, it can be seen that after the T03 saved the company from collapse, it received additional financing. However, compared to other new major companies that burn cash in the initial phase to establish brand awareness and then gradually reduce prices to focus on the price range of their products, Leapmotor took the opposite approach by using an ultra-low-priced vehicle to save itself. As a result, even with the higher price points and better features in later models, the prices still remain under high pressure, impacting profit margins.And the company's overall brand presence is clearly insufficient.

- Can low-end cars start the game and break the brand stalemate?

Although T03, as the first car, allowed the company to obtain financing, it also constrained the company's brand positioning, making it difficult to raise prices even with configuration improvements on subsequent cars.

Although the pricing of C11 has clearly increased to 180,000-230,000 RMB, it is still a low-profit car model based on its configuration. To avoid the status of a large proportion of negative profit margins, the sales price of cars must be able to cover the procurement cost. This is obviously impossible with T03 and can only be achieved by relying on C11, C01, and releasing 7 car models on platforms A, C, and D before 2025.

Considering the current Li Auto brand weakness and inadequate marketing budget (advertising and promotional expenses were only 260 million RMB last year, and only more than 80 million RMB was invested in the first quarter of this year), Dolphin Analyst believes that the path of upward pricing may likely require the accumulation of word-of-mouth through product strength, and it may also depend on slightly lowering the procurement prices after backend production increases, thus increasing profit margin space.

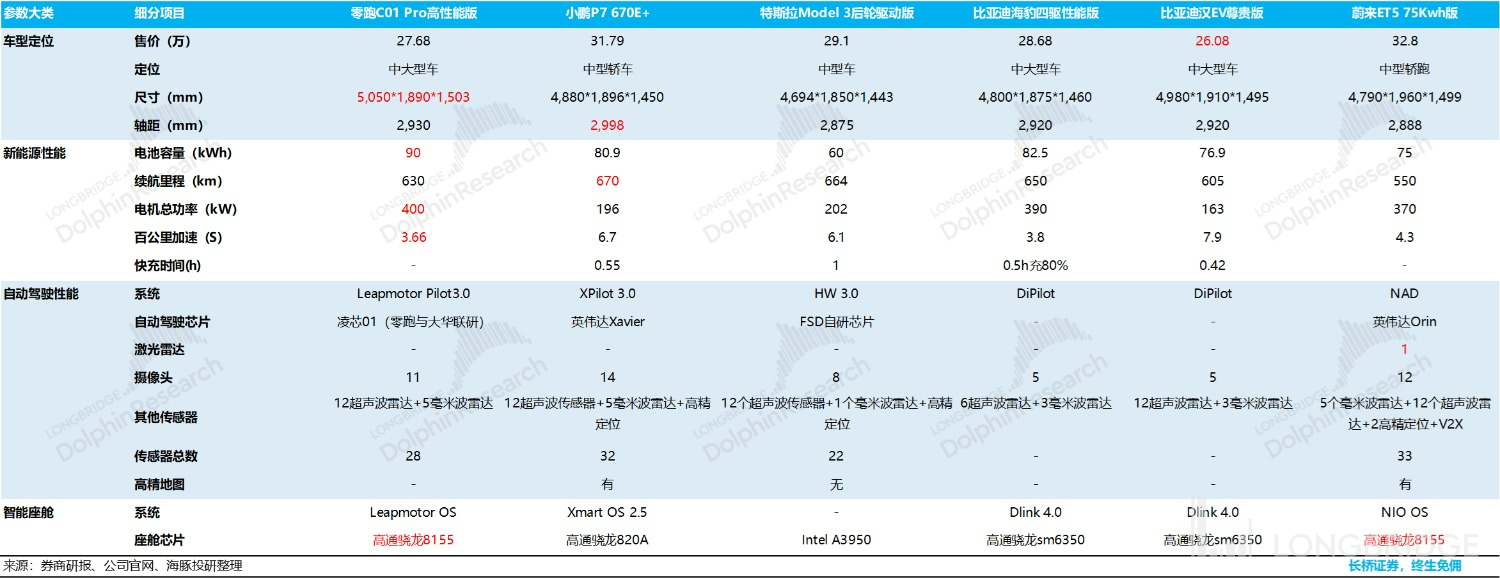

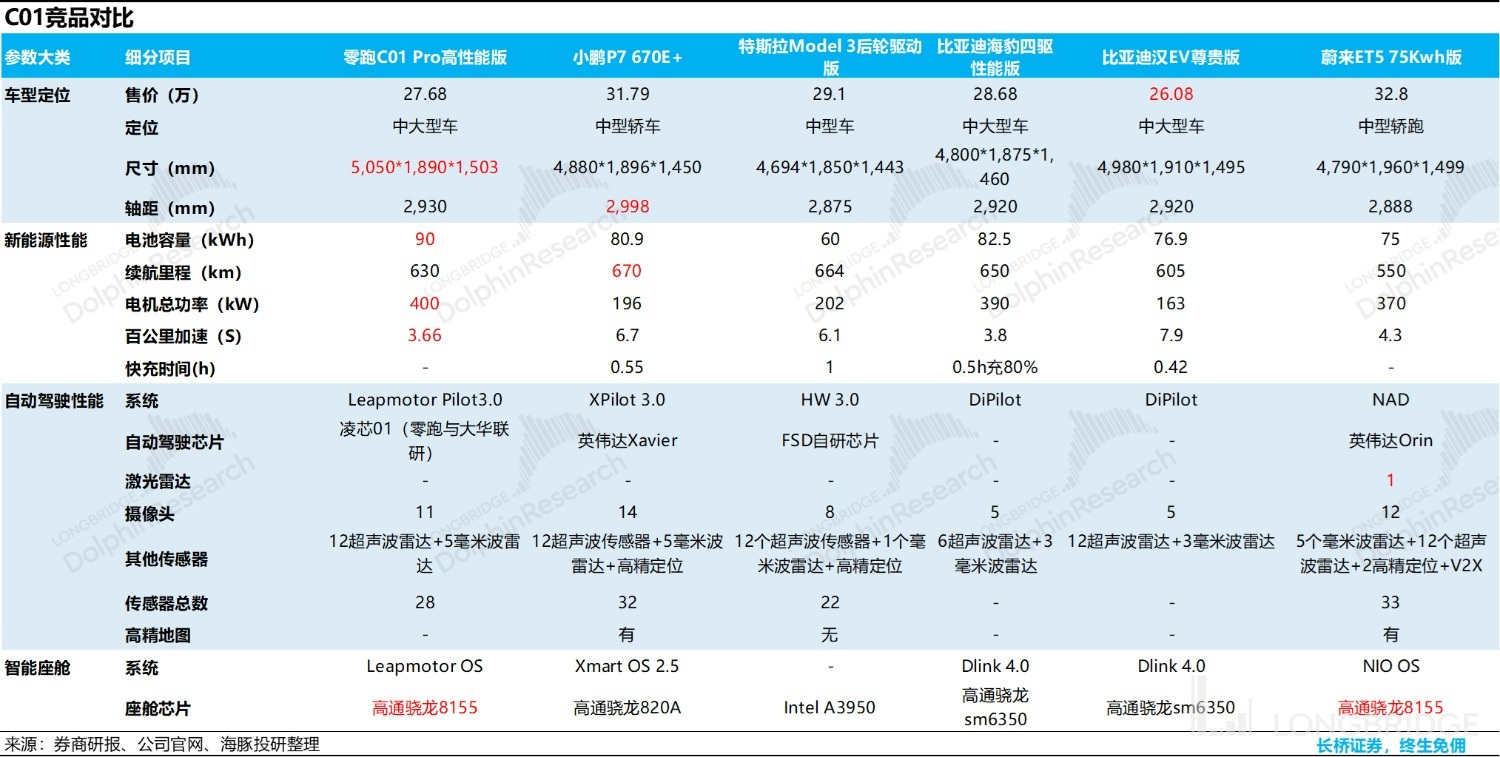

In terms of product strength, the latest model on the C platform, the first sedan C01, was officially launched yesterday and delivered together with the IPO debut today. Dolphin Analyst compared it with other mainstream competitive models in this price range.

From the perspective of product strength, C01 chooses a very practical path in terms of four dimensions: car size, power, intelligent driving, and smart cockpit. As advanced automatic driving configurations are currently ineffective in road traffic, it is relatively weaker in automatic driving. However, its intelligent cockpit and power system are relatively robust, and if combined with its relatively affordable pricing, it has good attraction from a product perspective.

But overall, relying on product strength to gradually increase premium space through word-of-mouth and using the self-produced method to reduce costs through increased backend production capacity in a low-end brand setting with weak impact is even more challenging than NIO and Li Auto, who set their brand positioning with high-priced cars and then gradually reduce prices. Even if the final path becomes feasible, it will take more time.

- "Blood-boosting" Li Auto

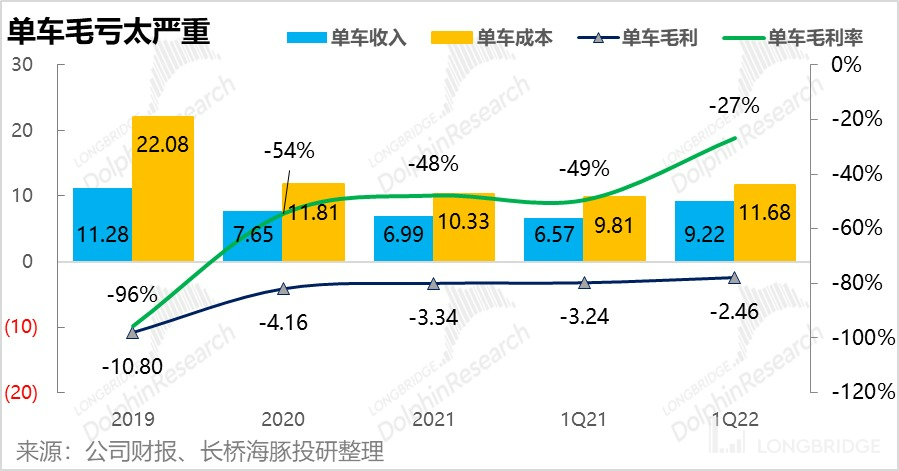

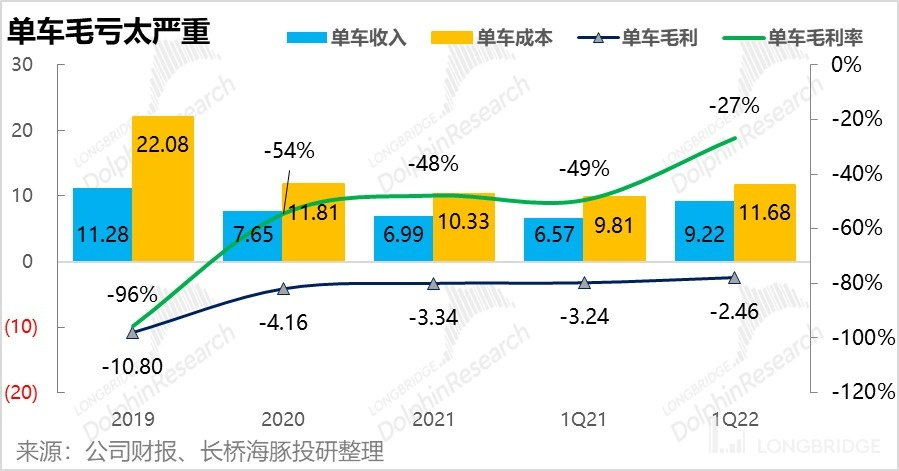

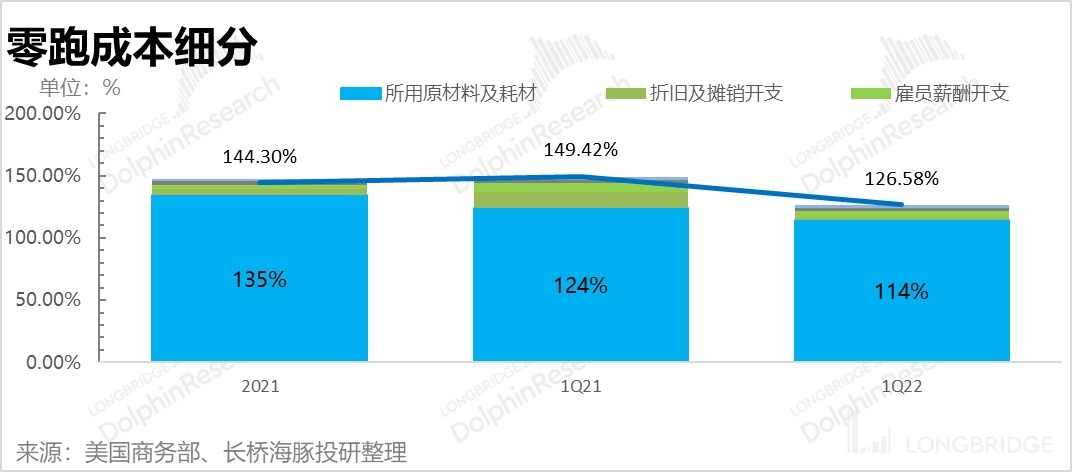

As the "Redmi" of new energy vehicles, its biggest problem is the flawed structure of its car models and the "unbearable" financial performance under this structure.Even in the first quarter of this year, when things had already significantly improved, the average price of a car was just over 90,000 RMB, with a single unit cost approaching 120,000 RMB. With each car already suffering a gross loss of 25,000 RMB.

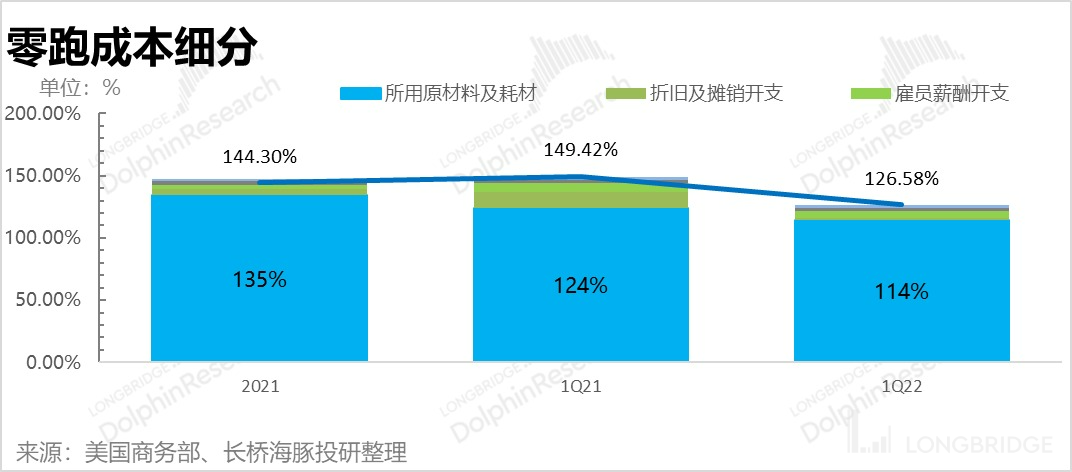

In terms of detailed cost breakdown, the core problem behind the low gross profit margin is that the cost of raw materials and consumables is too high. To put it bluntly, the price is too low while the materials used are too excessive – the factory price alone can't even cover the cost of materials, let alone subsequent expenses such as equipment depreciation, labor, sales, and logistics.

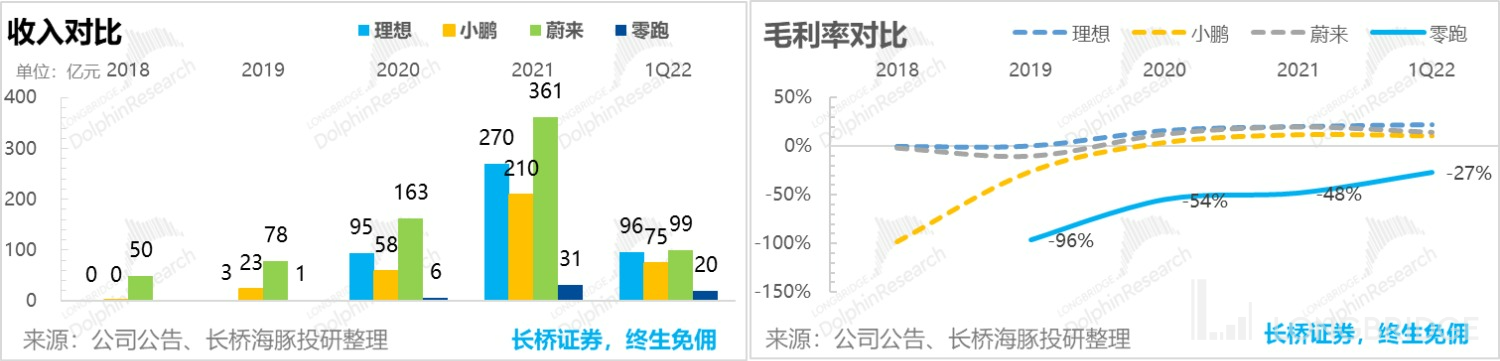

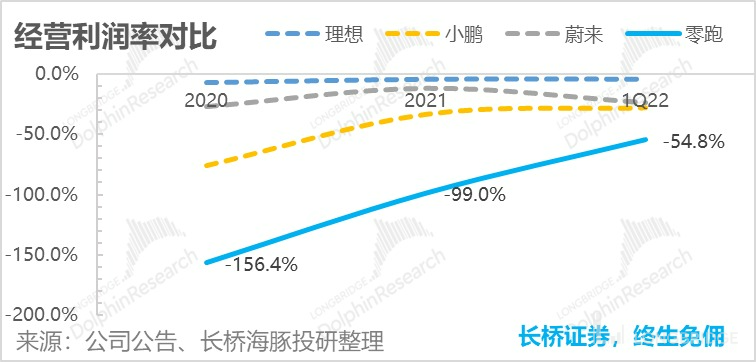

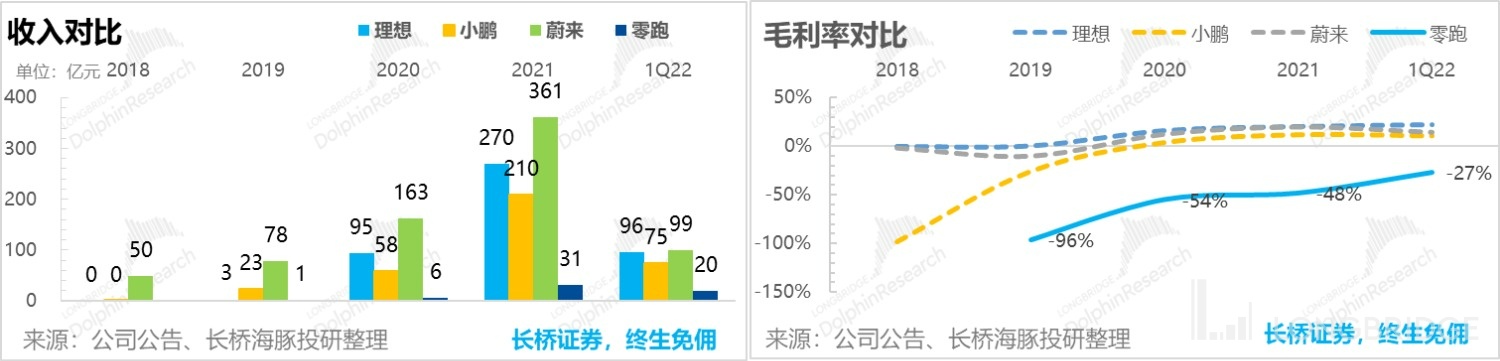

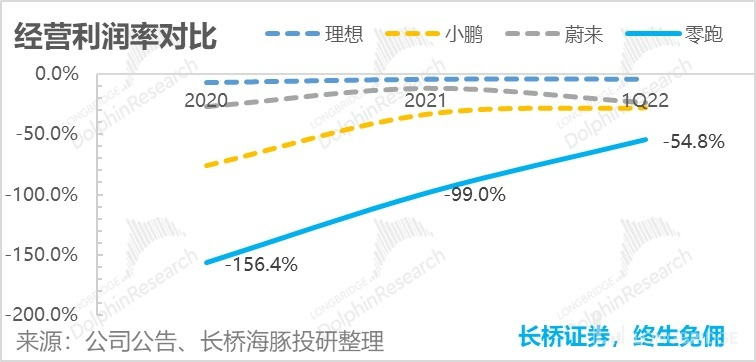

If we compare this with Li Auto's data, even the worst-performing Li Xiang had achieved an annual sales revenue of 2.3 billion RMB, with a gross profit margin of -26%. By comparison, as of this quarter, Leapmotor has only managed to sell about 2 billion RMB worth of cars while suffering a high loss of 27%. Judging by Leapmotor’s product structure, the main culprit for such a significant loss must be the Laotoule T03 model.

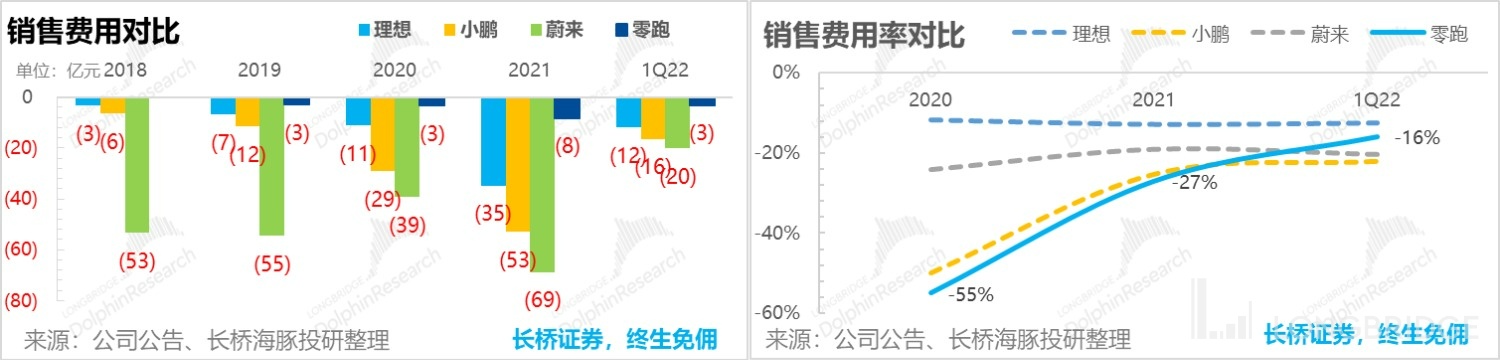

When it comes to research and development expenses and sales management, Leapmotor is extremely penny-pinching compared to its peers:

In terms of sales expenses, due to reliance on net sales to achieve volume, the absolute value of sales expenses can basically be ignored, and sales expense ratio has been kept as low as 16% even with quarterly revenues of only 2 billion RMB, making it the lowest among the three companies.

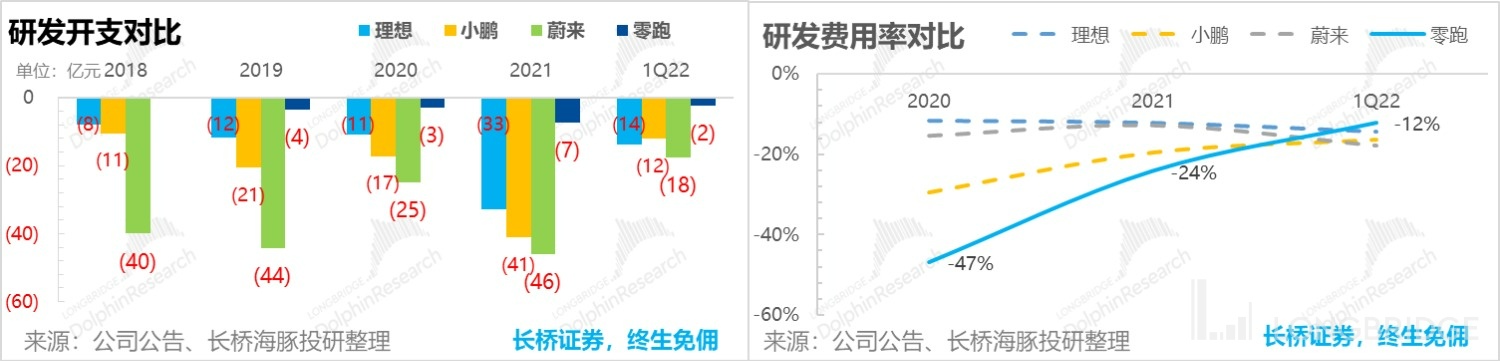

As for R&D expenses, the company has been extremely tight-fisted, with R&D expenses diluted to a mere 12% of the 2 billion RMB revenue scale, the lowest among the four companies.

Ultimately the huge difference in the net operating loss rate (with a net loss of over 50% of the vehicle price per unit) can be attributed back to the fact that the cars are underpriced yet also use materials that are too expensive, leading to severe losses.

Overall, from a financial perspective, Leapmotor is nearly a new energy company that has already sunk to a "shocking" and despairing level of loss. In the current market environment, where risk is widely abhorred, if it does not adapt and reach a valuation with sufficient safety margin, it “virtually” has no hope of getting by on T03’s “inflated” sales data alone.IV. Is there still any investment value for companies that lose so much?

It's jaw-dropping how much these companies are losing. Does this market still have any investment value? In the opinion of Dolphin Analyst, it's still necessary to take a look at the specific valuation.

1) After surviving the edge of bankruptcy, the next key turning point: it seems easy to reverse gross loss

If we compare its gross profit margin with its bicycle economy and vehicle structure in more detail: when the sales ratio of the highly-priced C11 reached 36% in the first quarter of this year, the overall average unit price of the company was 92,200 yuan, which was 26,600 yuan higher than the same period last year when only T03 was on sale. The cost of a single vehicle rose by 18,700 yuan to 116,800 yuan. In this pricing process, the asymmetric increase in vehicle revenue and cost actually improved the overall gross loss rate slightly.

And note the sales volume during the same period. In the first quarter of last year, there was only T03, with T03 accounting for 64% and C11 accounting for 36% in the first quarter of this year. However, starting from July and August this year, C11 began to increase rapidly, from a monthly sales of 5,000 in May and June to over 6,000, and now its sales have caught up with the T03.

Moreover, C11's rapid increase in sales occurred when C01, which already had a clear reservation expectation, was launched. That is to say, although C11 and C01 were built on the same platform and had similar dimensions, one was an SUV and the other was a sedan, and they did not show any obvious erosion of each other.

Currently, Jinhua company can produce up to 200,000 vehicles, and considering the current production and sales level of T03 at 5,000-6,000 vehicles, if the supply chain problems can be solved and there are enough orders, its current production capacity can meet the demand for C11 and C01, which is about 10,000-12,000 vehicles.

Based on the low intention deposit (450 million yuan) for C11 in the first quarter, the number of orders should be guaranteed. As for C01, the company previously announced that it had reserved more than 100,000 units, but Dolphin Analyst estimated that this number should have a relatively large fluctuation since before the official launch yesterday, this vehicle was sold with zero down payment and no reservation, but the intention of 100,000 units shows that users are still quite interested.

If the sales contribution ratio of C01 and C11 with higher prices continues to increase, then it is hopeful that Zeropark will soon see a turning point where the gross profit margin becomes positive.

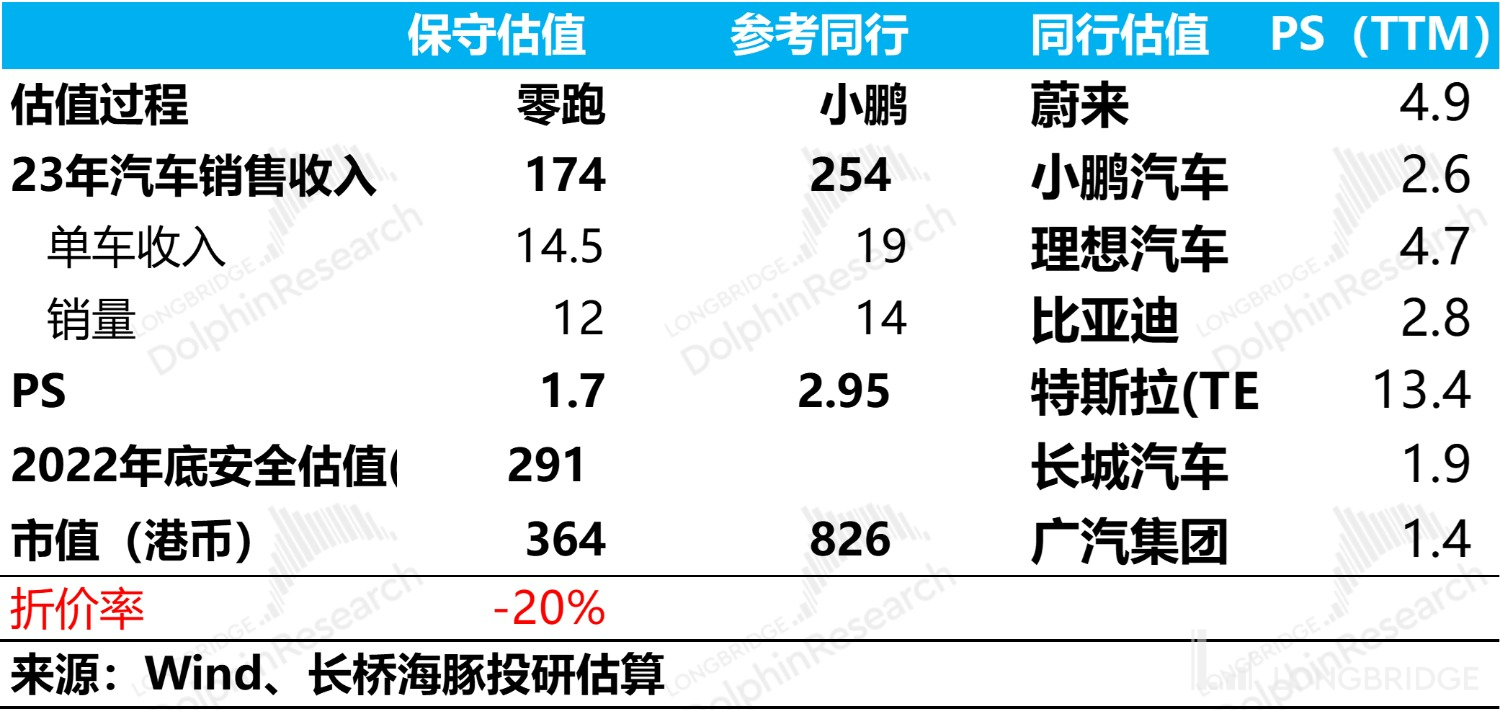

And the core point here is: For Zeropark, its investment opportunities should be found in the price plunge to a low enough point to look for investment opportunities with a turning point of gross profit margin becoming positive in 2023. After all, Weimotors has already passed the point of gross profit margin becoming positive, but Zeropark still has a chance to invest in gross profit margin becoming positive.It was difficult for Dolphin to value ZERØRUNE, a company that has always been in existence using Dolphin Analyst's usual DCF. However, with the judgment of the valuation, which is based on the expected sales of the valued vehicle models C11 and C01, it has become relatively easier: Make an extremely conservative valuation, pass the critical point of turning from gross loss to gross profit to survive, and then look at its long-term value.

2) Valuation logic:

The short-term investment opportunity for ZERØRUNE lies in the turn of the gross profit. However, since the problem of gross loss can be solved by controlling costs, to some extent, the problem of the critical point of turning from survival to death can be addressed. After that, the question becomes more long-term, such as the problem of long-term sales and upgrading.

Therefore, Dolphin’s valuation judgment for it is based entirely on the sales outlook within one year. The sales within one year are based on its capacity and output structure arrangement.

Assuming that among the annual output of 200,000 units, T03 maintains a sales volume of 5,000 units for one year, and C11 and C01 have a monthly sales volume of 10,000 units (this number should be relatively easy to achieve, C11 is currently selling over 6,000 units, and C01 should sell 4,000 units per month under the circumstances of 100,000 interesting orders).

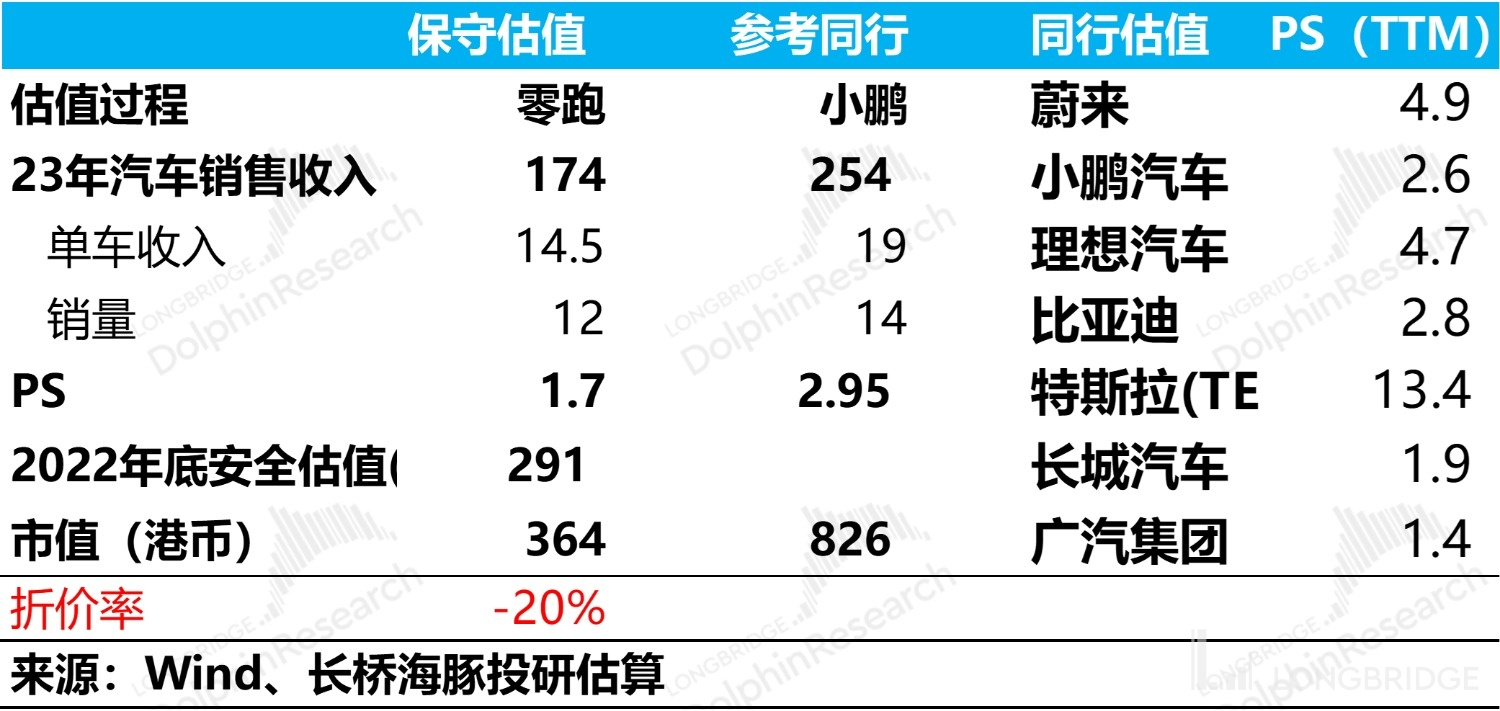

The sales of the contribution valuation models C11 and C01 are 120,000 units last year. The company can achieve full production status in 2023. Dolphin Analyst believes that T03 does not contribute to the valuation from the perspective of secondary market investment value.

Based on Dolphin Analyst’s previous dismantling of single-bike income and cost analysis, he estimates that the price of C11 is 144,000 yuan (considering actual factory price after some user discounts and dealer deductions).

For the valuation reference, Dolphin Analyst mainly refers to Xiaopeng Motors, because from the perspective of sales channel strategy and pricing strategy, it is basically similar to Xiaopeng Motors, with a positioning of 150,000 to 300,000 yuan, which is colliding with fuel vehicles. Also, it is because on this positioning channel, besides direct sales, more are sales through dealers, but ZERØRUNE is the "red rice version" of Xiaopeng below.

The valuation mainly uses short-term PS as the valuation reference and Xiaopeng Motors as the core reference point. Considering the additional investment risk brought by its lack of cash and the difficulty of brand value enhancement, it is compared downward with traditional cars, and the PS is comprehensively set at a slightly lower position of 1.8 times. Corresponding to the conservative sales and valuation expectations of 2022, it corresponds to around HKD 30 billion.

The corresponding core judgment is:

Dolphin Analyst recognizes that ZERØRUNE is a company that is serious and down-to-earth in making cars. In the beginning, it was slow to take action due to its insistence on production. As a result, the hasty promotion of cars was not successful, and it was facing the crisis of breaking the capital chain. Therefore, to avoid death before success, it reluctantly made a popular loss-making car that was not in its target positioning to raise funds.

This shortcut has enabled it to survive, but it is also limited by the price-performance ratio and low brand value. In addition, it is not good at internet marketing, and the budget is insufficient, which leads to insufficient brand sense. Therefore, using the release of product power and production scale efficiency to achieve the upward pricing and gross loss turning positive is the next life-and-death test that ZERØRUNE must pass after going public. From an investment perspective, risks and opportunities originate from this.After the IPO discounted listing and the subsequent plunge in stock price, Dolphin is now looking for investment opportunities at a reasonable price. Zero Run falls around 20% again today, which is equivalent to being cut in half from the IPO price. Dolphin sees this as a very safe investment opportunity and closely tracks its order progress and delivery volume to play a high certainty gross margin turning point investment opportunity. Once the gross margin has turned positive, the zero run stock price will have higher elasticity to go up.

Dolphin's historical articles reference:

Risk Disclosure and Statement of this article: Dolphin Research Disclaimer and General Disclosure