Google soaring? Learning from Meta, striving to be the best

On the morning of April 26th, Beijing time, $Alphabet.US's parent company Alphabet released the financial report for the first quarter of 2024. The significant post-market surge has indicated that the market is very satisfied with the performance of this financial report, summarized in four key words - $70 billion buyback, first dividend, better-than-expected performance, and layoffs for efficiency improvement, reminiscent of Meta in the previous quarter.

Key Points of the Financial Report:

1. Bringing out the Same Gift Package: Seeing the stock price soar after Meta introduced buybacks and dividends last quarter, Google has also brought out the same gift package, adding a $70 billion buyback and issuing its first dividend ($0.2 per share). Although the dividend is more symbolic, at least the company has taken the first step.

2. Revenue Expectations Adjusted: The revenue side in the first quarter has swept away the gloom of the previous quarter and returned to the stable state of exceeding expectations. Dolphin believes that besides optimizing its own technology (AI empowerment), the market's conservative expectations have also contributed to the expectation gap. Looking into details:

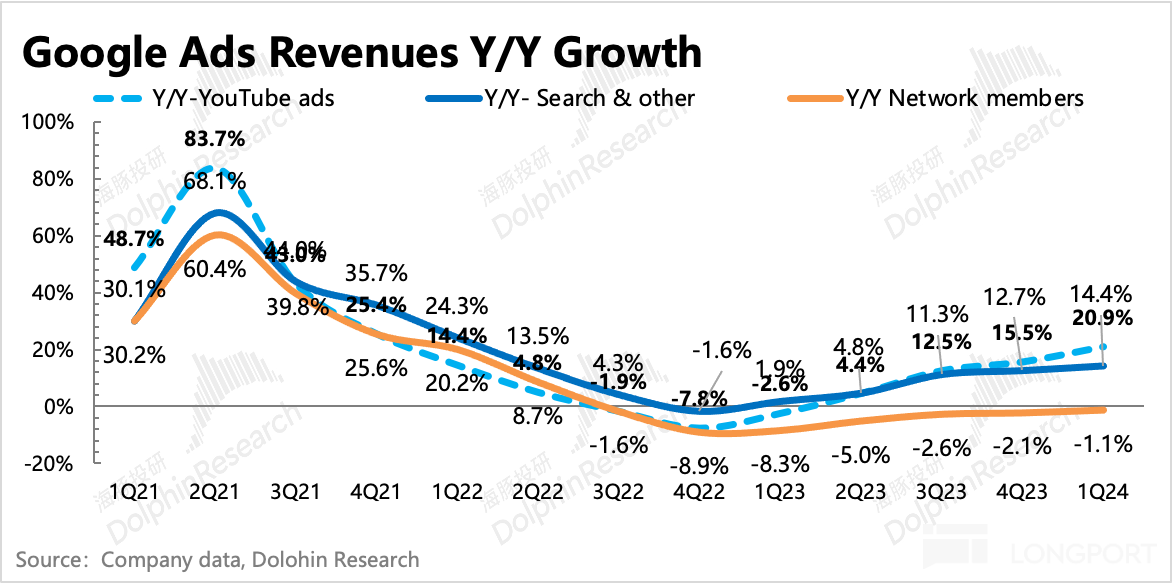

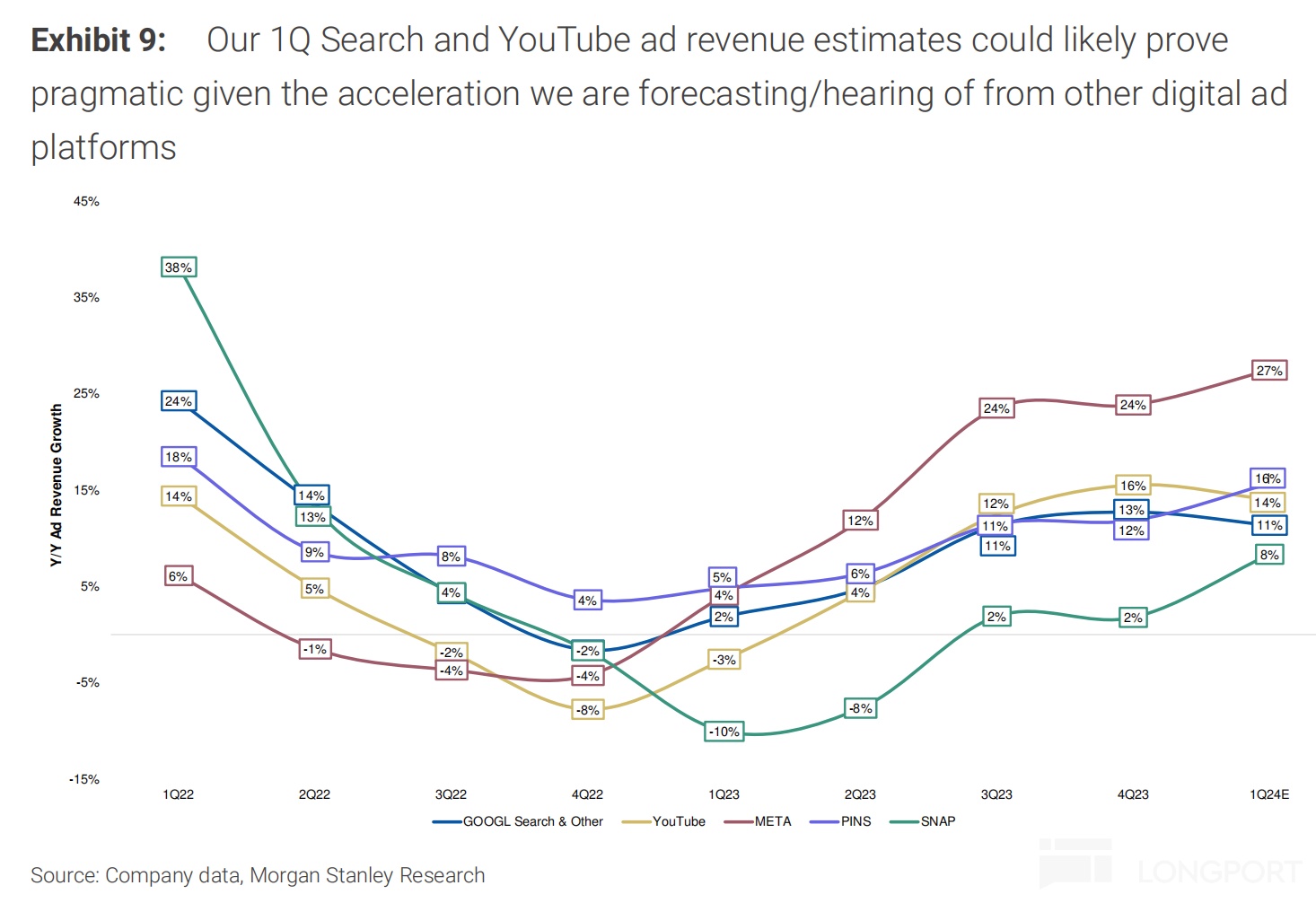

(1) YouTube: With the highest growth rate due to a low base, but in terms of month-on-month improvement, it also has the largest improvement, with a 20% year-on-year growth rate, exceeding the market's expectation of 15%.

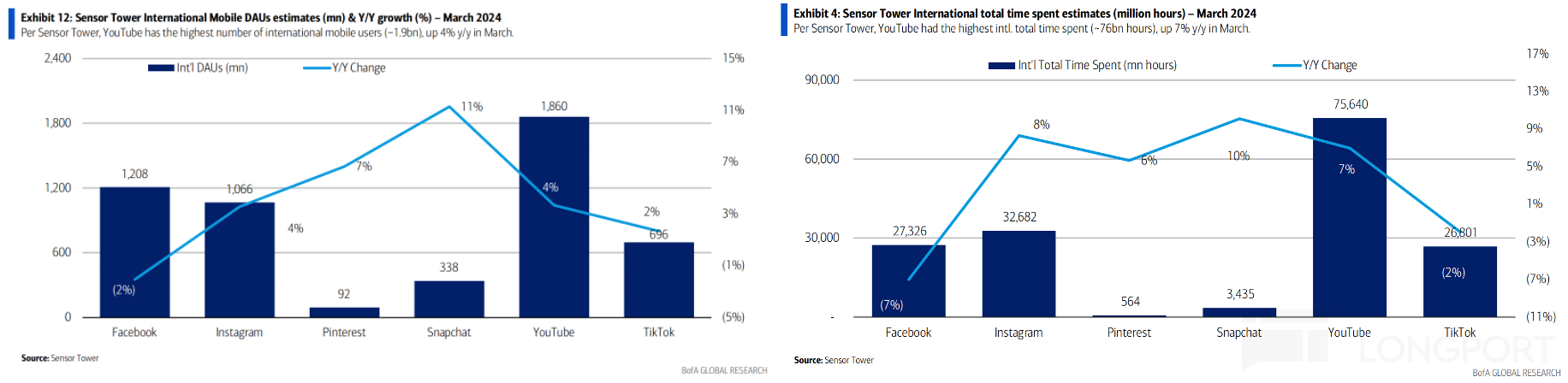

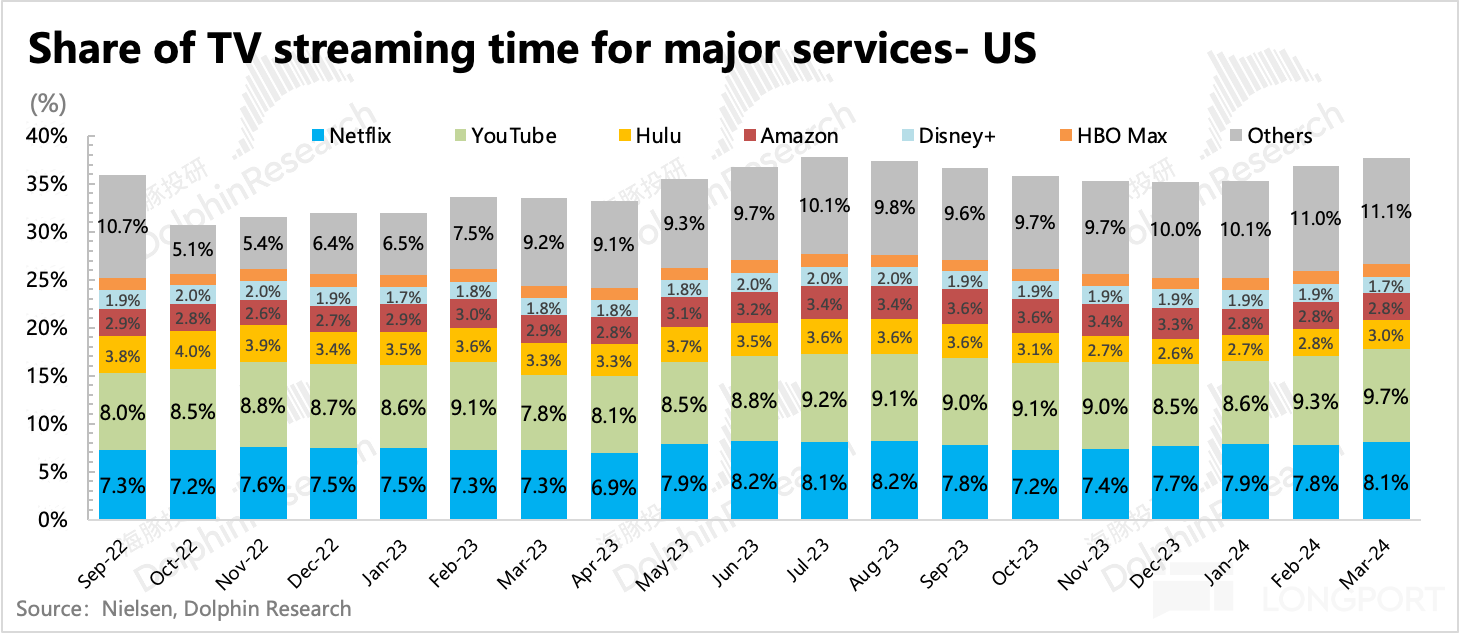

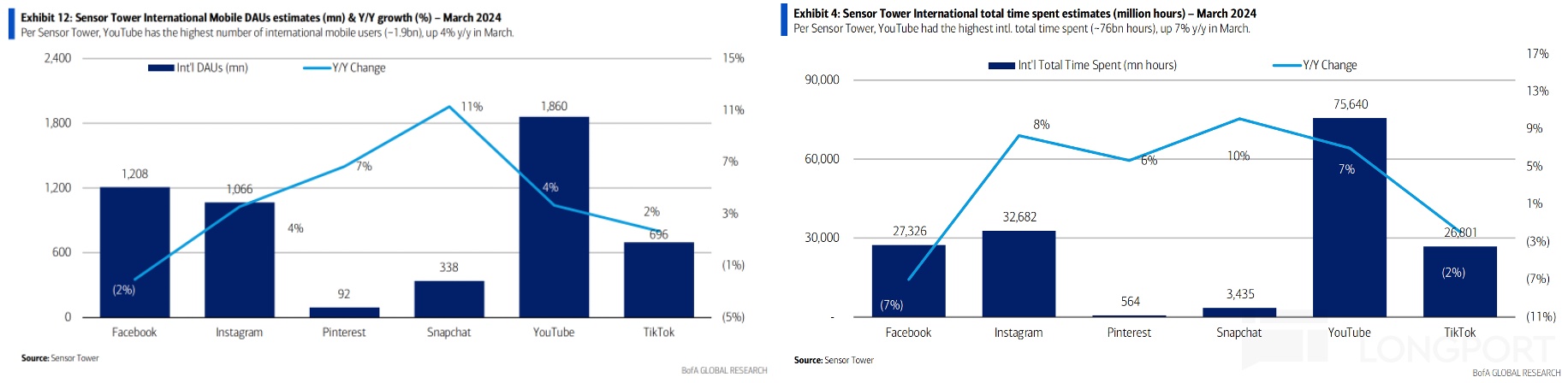

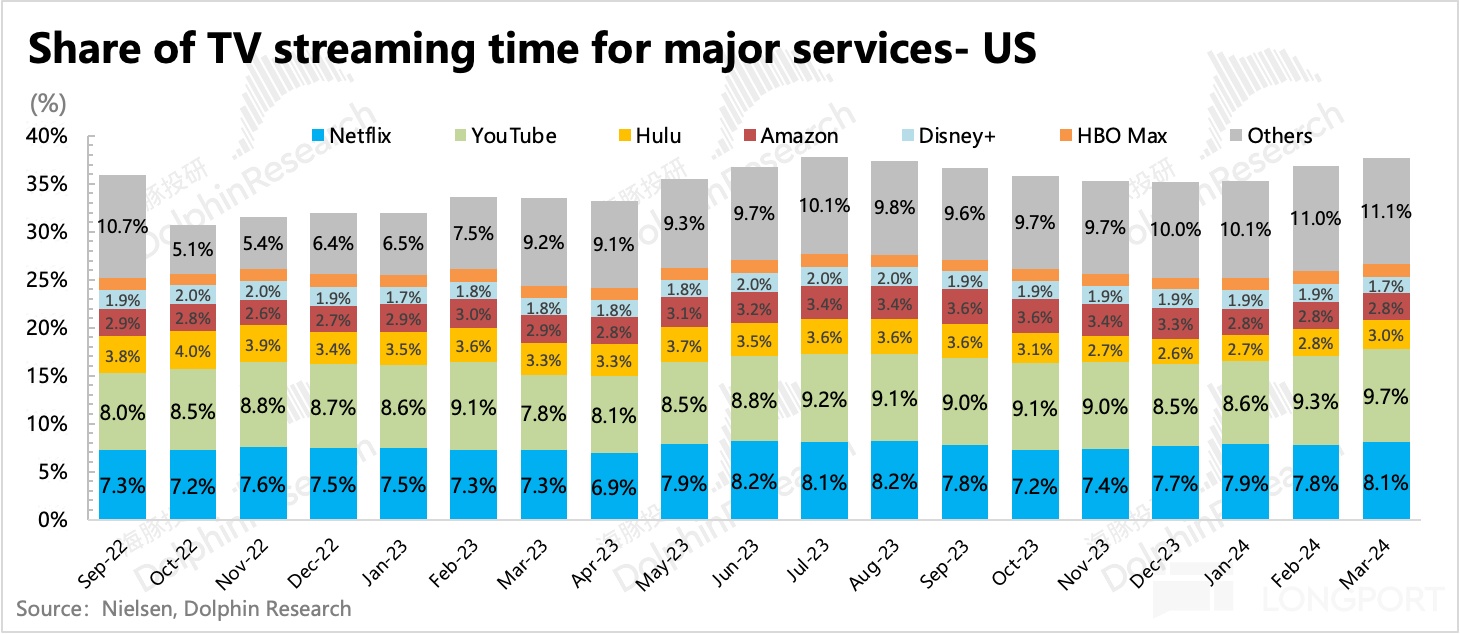

In fact, third-party data shows that YouTube's user data has performed well recently. For example, according to Nielsen, YouTube's share of streaming TV time in the United States increased by 2 percentage points year-on-year in March, possibly due to the relatively lack of content from peers in film and television. At the same time, according to Sensor Tower, the user growth of YouTube's App in the United States region in the first quarter is more stable than its peers. Although some institutions have raised their revenue expectations for YouTube in the past month, the actual performance is still better.

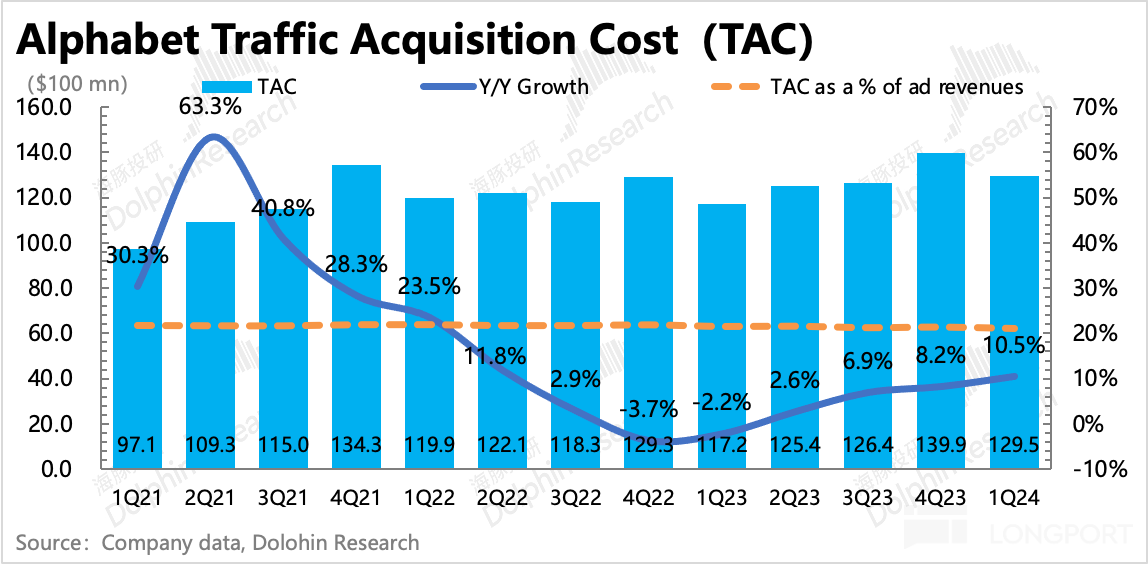

(2) Search: This is the main area where market expectations are relatively conservative. Search advertising in the first quarter grew by 14% year-on-year, while the market expected only 11-12%, possibly still concerned about the erosion from new AI entries.

Dolphin believes that in the long run, this issue may ultimately be unavoidable. However, in the short term, Google still has defensive power (leading AI technology globally), and the migration of advertising budgets also has a process, requiring a balance between user scenarios, user stickiness, and advertising conversion effects.

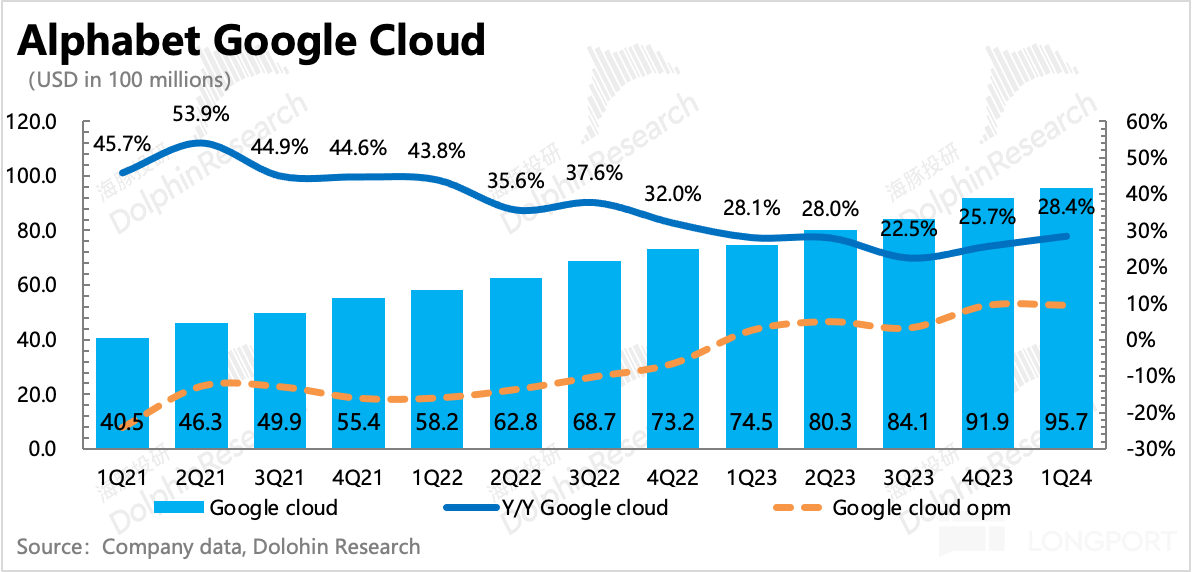

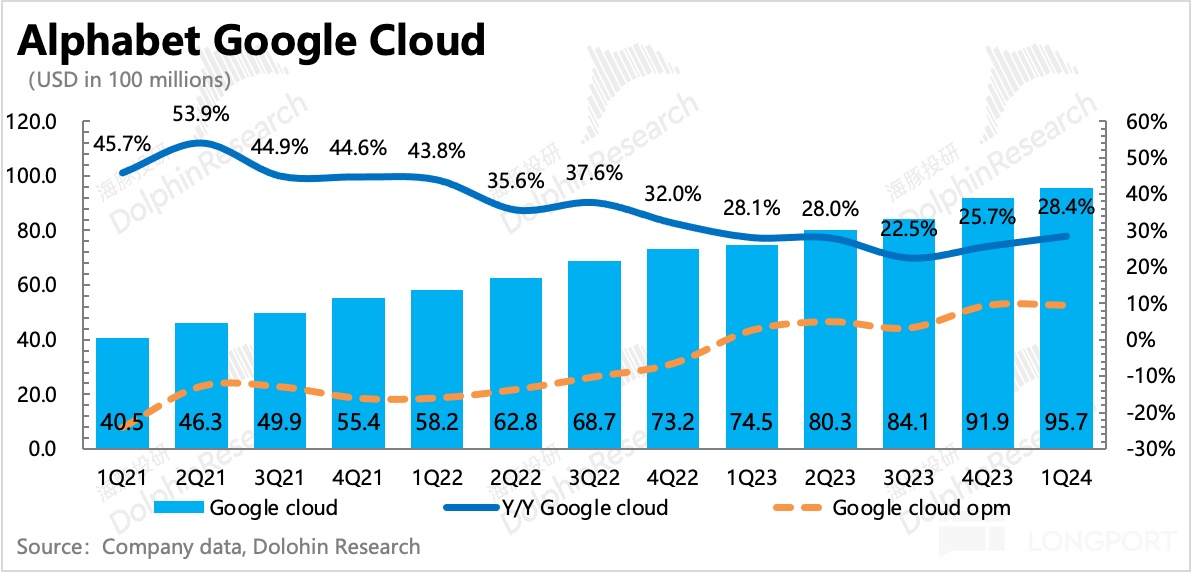

Currently, AI question-and-answer platforms led by GPT are mostly used in office and learning scenarios (GPT traffic will quickly decline during holidays), and the commercialization space for advertising is temporarily limited. However, due to the rapid development of this round of AI industry transformation, it is still necessary to closely monitor marginal changes.(3)Cloud: It is truly benefiting from AI, with a quarter-on-quarter growth rate of 28% accelerating. Although there are some base effects, cloud services do not show obvious seasonality, with consistent customer demand (high renewal rates under no major changes), coupled with some recent introductions by the management at the Next conference in early April, Dolphin believes that there should be a significant AI bonus for the accelerated growth in Q1.

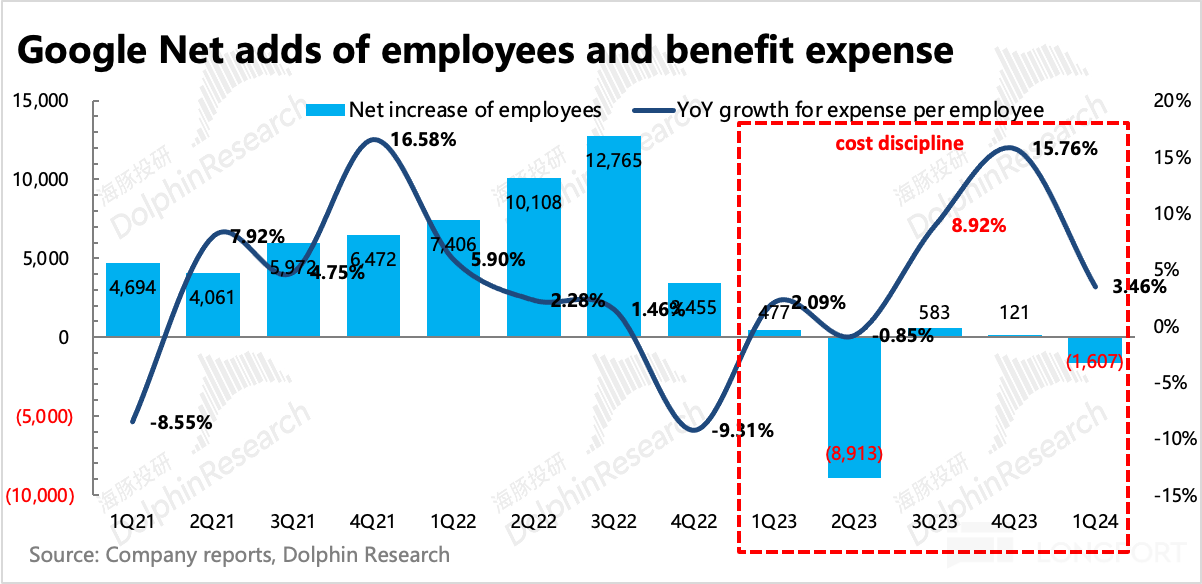

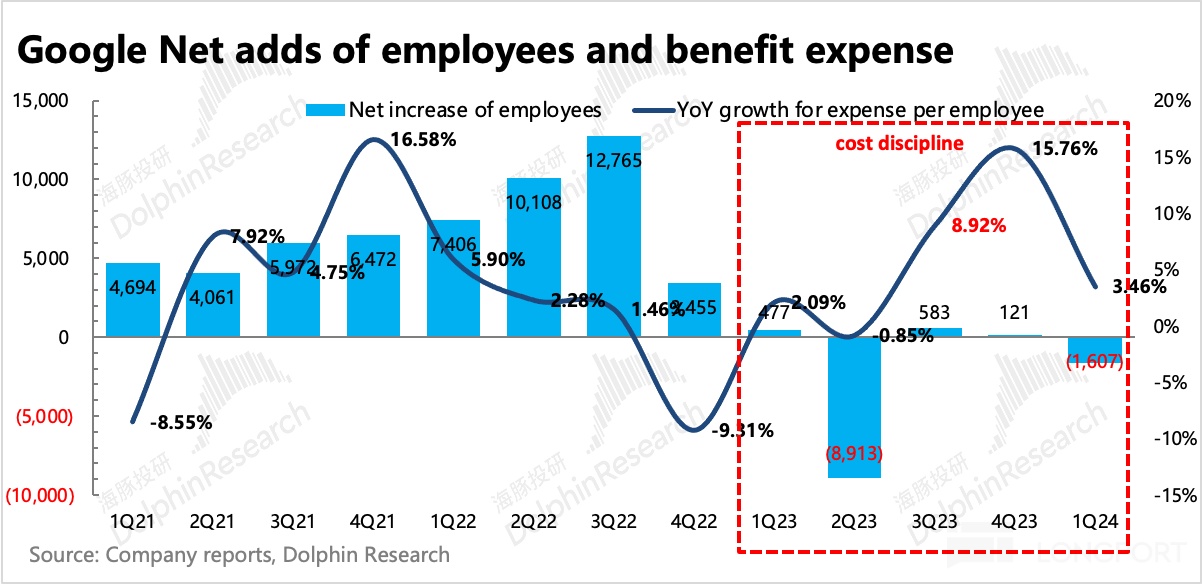

3. Efficiency improvement cycle is not complete yet: Unlike Meta, which has already gone through the benefits of layoffs, Google started its layoffs later, paused last quarter and then progressed in Q1, so there is still a pull on profit margins from layoffs. As of the end of March, the company reduced its employees by 1,600 compared to the end of last year, a decrease of nearly 10,000 year-on-year.

In addition, it may be related to AI improving ad conversion rates, as well as internal operational efficiency improvements. For the Services business mainly focused on advertising, the OPM of the segment is close to 40%, and excluding severance costs, the profit margin is hitting new highs.

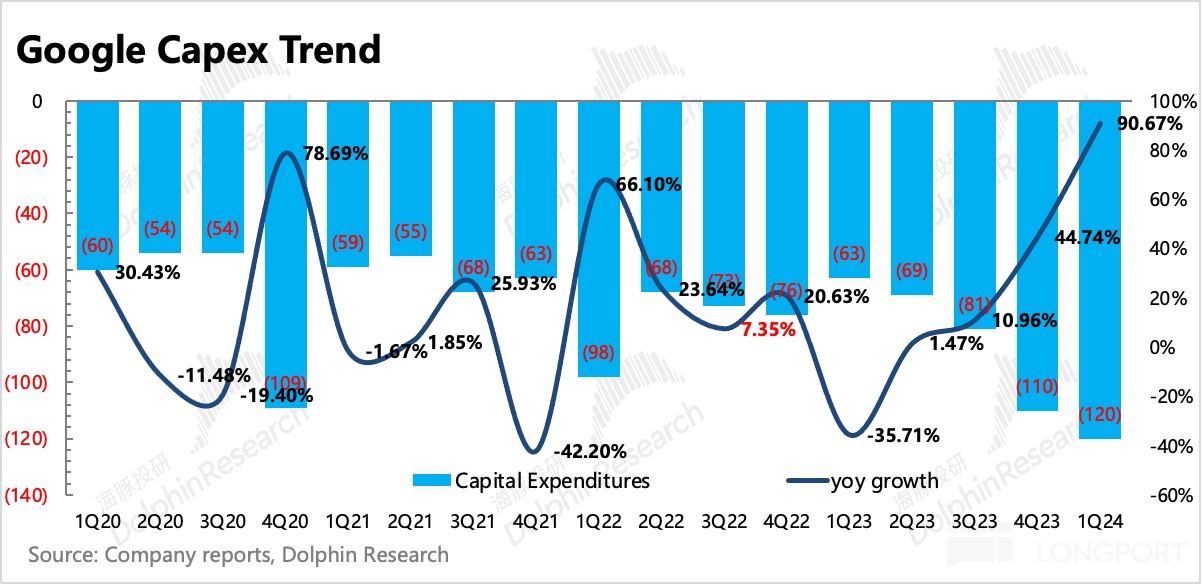

4. Capital expenditure is increasing as planned: Due to the demand for AI investment, Google's capital expenditure started to surge last quarter, and the management also indicated that there will be a "significant" growth this year. Capital expenditure increased quarter-on-quarter in Q1, almost doubling year-on-year.

5. Focus on core issues in the conference call

Google's financial reports generally provide little explanation of changes in business metrics, mainly explained during conference calls. Therefore, analyzing the specific operating conditions, its conference call is quite important.

Considering Meta's warning yesterday, including the significant slowdown in growth in the second quarter, there should be many common issues with Google (such as the weakening of Temu's advertising placement in the U.S.), so it is necessary to pay attention to the management's outlook on advertising during the conference call. In addition, will the company's expectations for increased capital expenditure due to future AI investments accelerate the end of the efficiency improvement cycle, returning to investment like Meta? Also, there may be some progress in certain regulatory issues in the second half of the year, so see how the management evaluates the impact of risks.

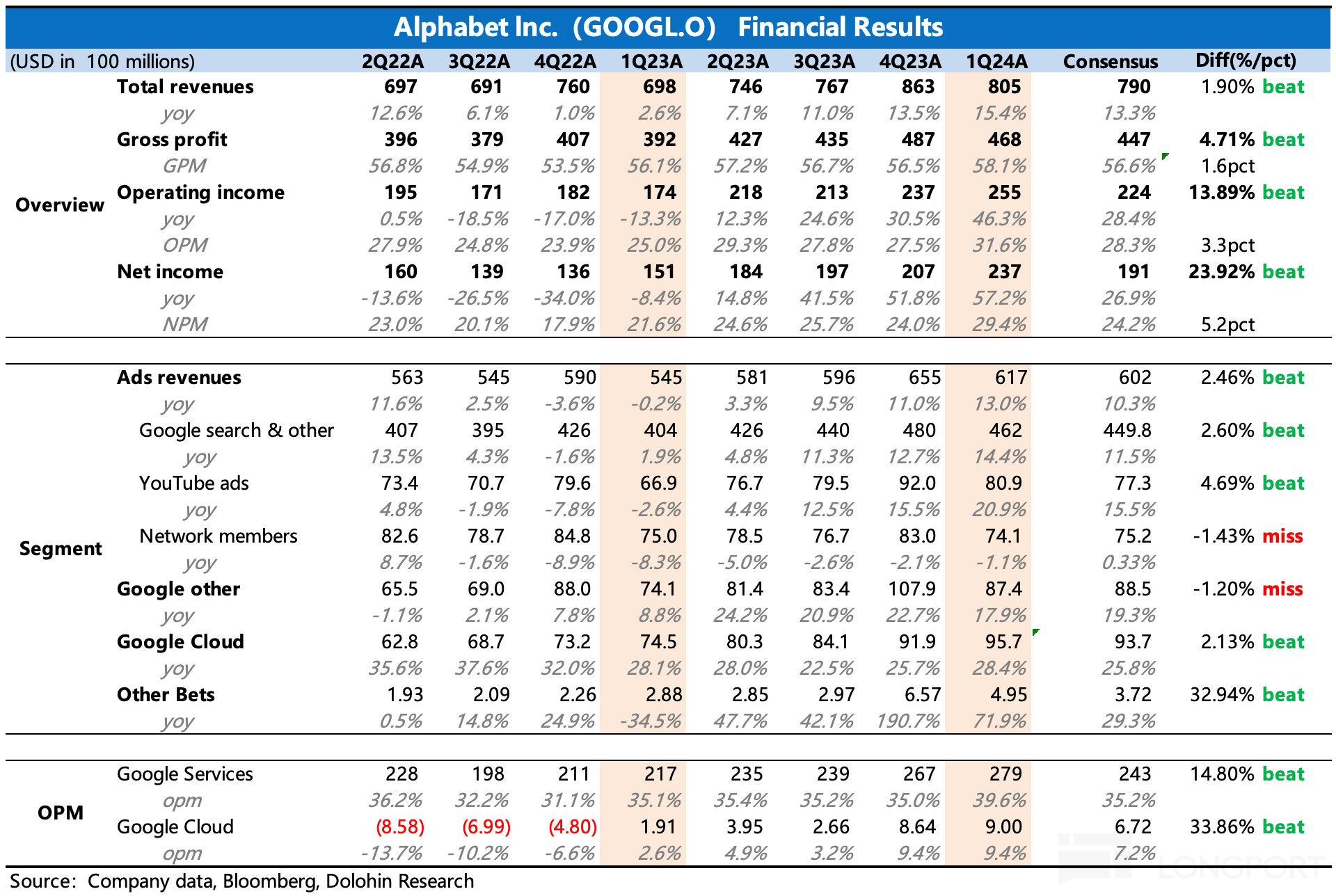

6. Comparison of key indicators and expectations

Dolphin's Viewpoint

The biggest positive in the first quarter is actually similar to Meta's shareholder bonanza in the previous quarter: a $70 billion buyback + first-time dividend. Of course, the performance itself did not disappoint, but the surprise behind it is actually a correction of expectations—due to the shadow of Q4 23 and concerns about AI replacing search entry points, the market's expectations for Google were generally low before the financial report, and in the same low base + strong macro background, it did not show the same accelerated growth as Meta, instead showing a trend of slowing growth ahead of time (the advertising industry's base will be raised in the second half of this year).

However, core institutions have significantly raised their expectations in the past month, especially on the profit side. This is also the reason why the stock price returned strongly after a small dip caused by the Gemini "racial gate" incident at the end of February.After-hours trading pushed the market value to 2.15 trillion, further narrowing the valuation repair space brought by the expectation gap (based on previous expectations, implied PEs for 24/25 years were 24x/22x respectively. If market sentiment reverses after 1Q earnings, profit expectations increase by 15%, then PE for the next two years will drop to around 21x/19x, similar to Meta's valuation after the plunge). Although cloud business growth will be strong under AI + low base, and cost-cutting will help profitability, Google Ads also face high base pressure in the second half of this year. Moreover, Capex investment in AI will significantly increase this year. Compared to Meta, Google still faces mid-term growth concerns about search entry erosion in its advertising business. Perhaps Google's collaboration with Apple in Gemini and the boost from AI in cloud business can alleviate some concerns, but in the long term, Apple also has self-developed capabilities, and Google's cloud business product competitiveness is not leading.

The above questions suggest focusing on the conference call, specifically on management's growth expectations, investment outlook, and progress in cooperation with Apple.

Below is a detailed interpretation of the financial report

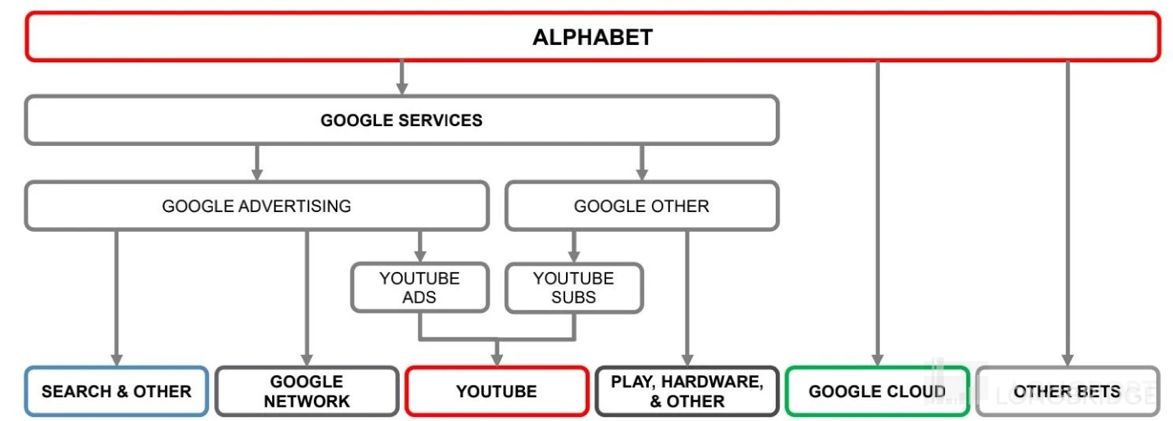

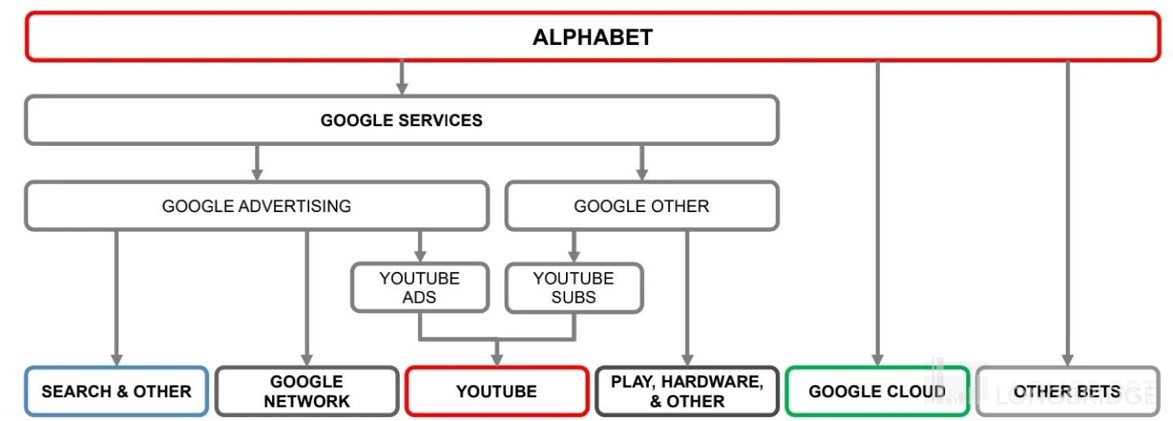

I. Google Overview

Google's parent company Alphabet has a diverse business portfolio, and its financial report structure has changed multiple times. For those unfamiliar with Alphabet, you can first take a look at its business structure.

To briefly explain the long logic of Google's fundamentals:

a. Advertising business, as the main revenue driver, contributes significantly to the company's profits. Search advertising faces a crisis of being eroded by information flow ads in the medium to long term, with high-growth streaming media YouTube filling the gap.

b. Cloud business is the company's second growth curve, having turned losses into profits and showing strong recent momentum in signing deals. With advertising continuously affected by weak consumer spending, the development of cloud business is becoming increasingly important to support the company's performance and valuation imagination space.

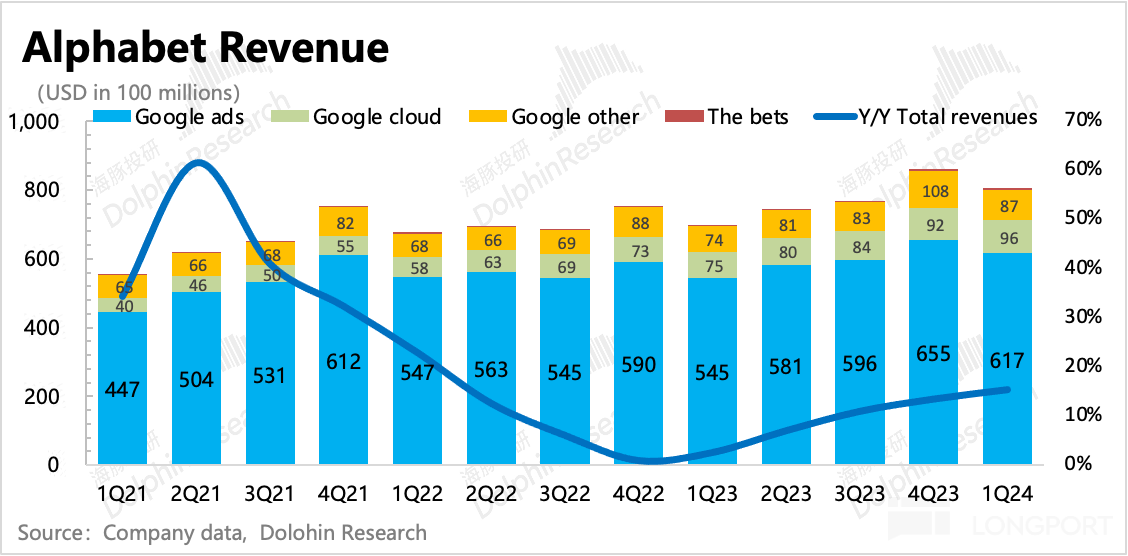

II. Three major revenue pillars all exceed market conservative expectations

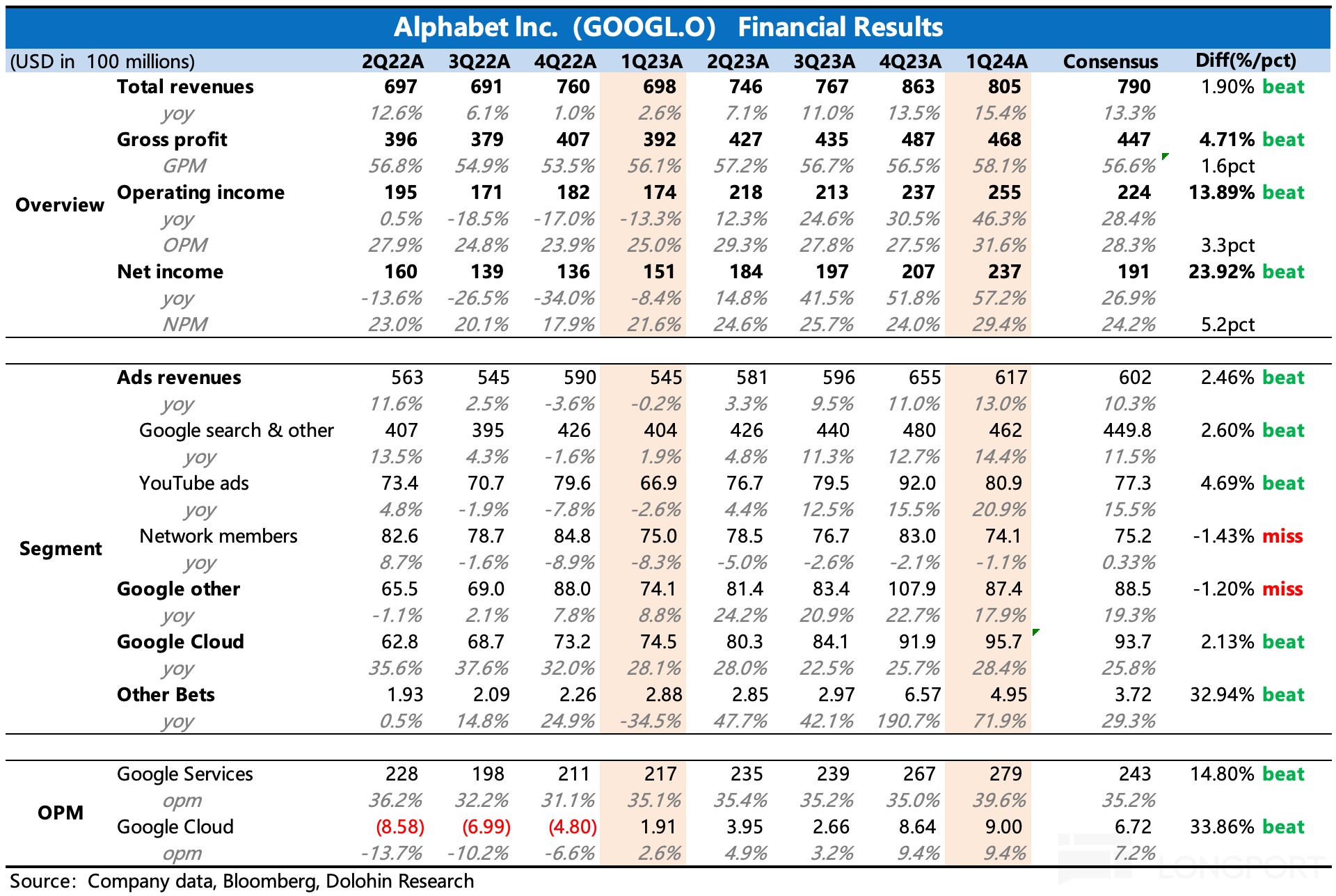

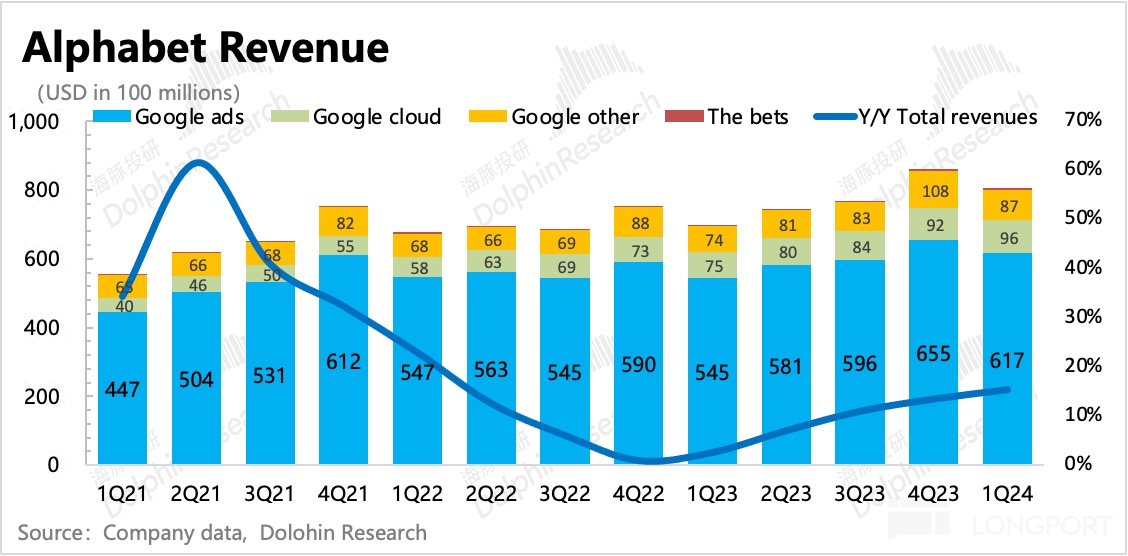

In the first quarter, Google's overall revenue was 805 billion, a year-on-year increase of 15.4%, exceeding the market consensus of 790 billion. Low base + strong consumption support Google's advertising revenue to continue accelerating year-on-year growth.

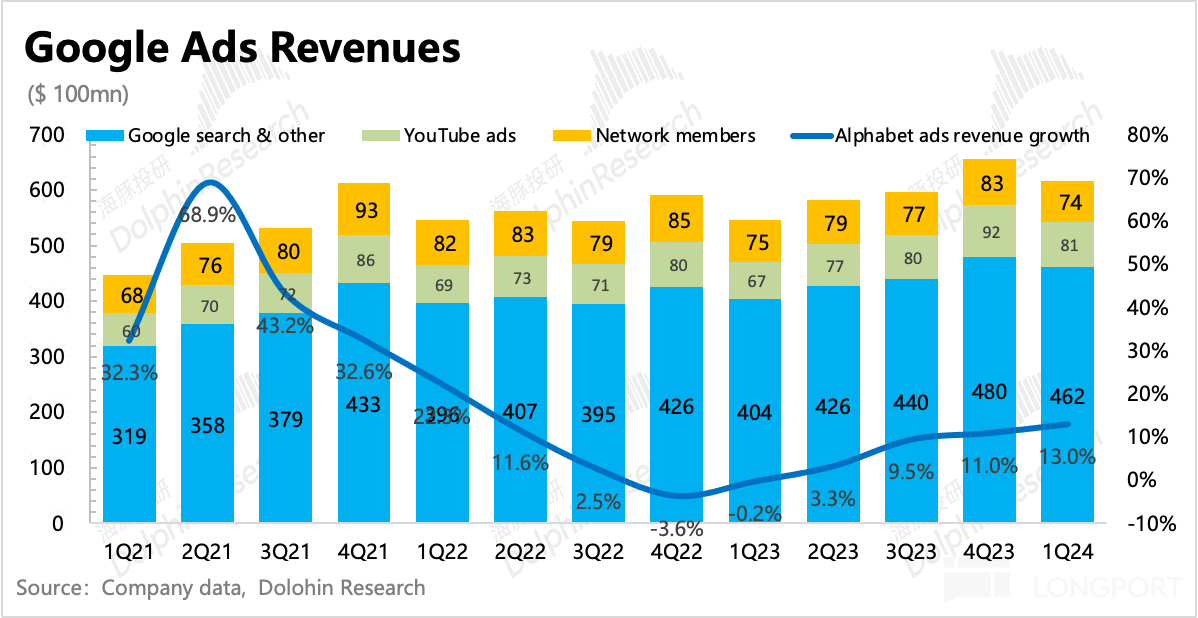

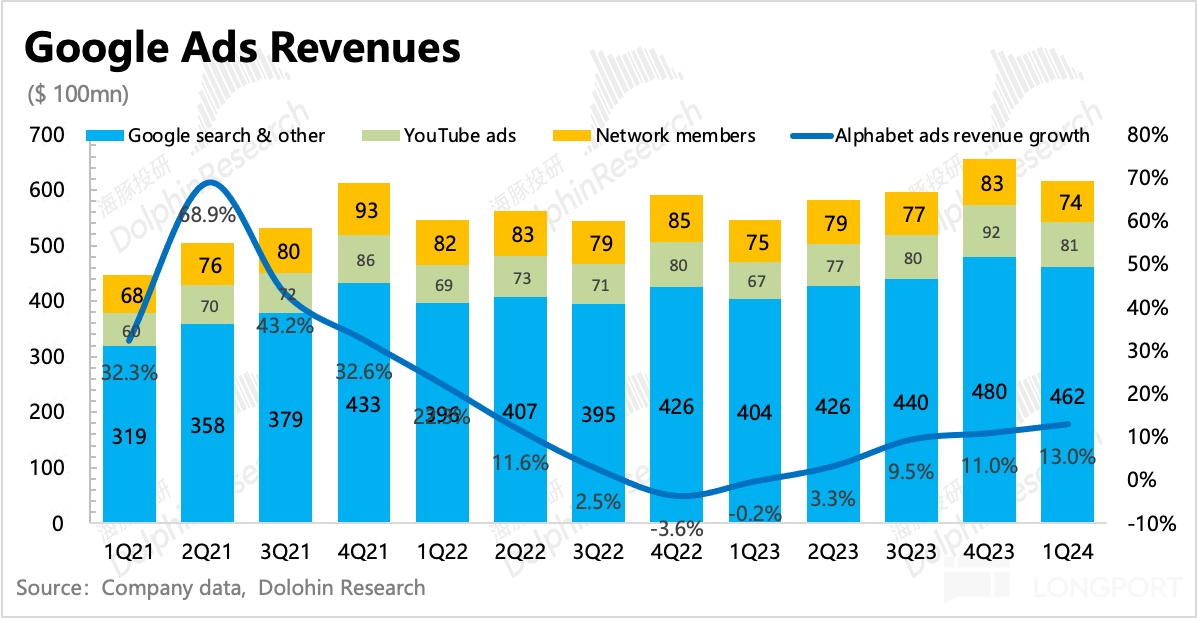

(1)Advertisement: YouTube Strong, Search Defying Doubts

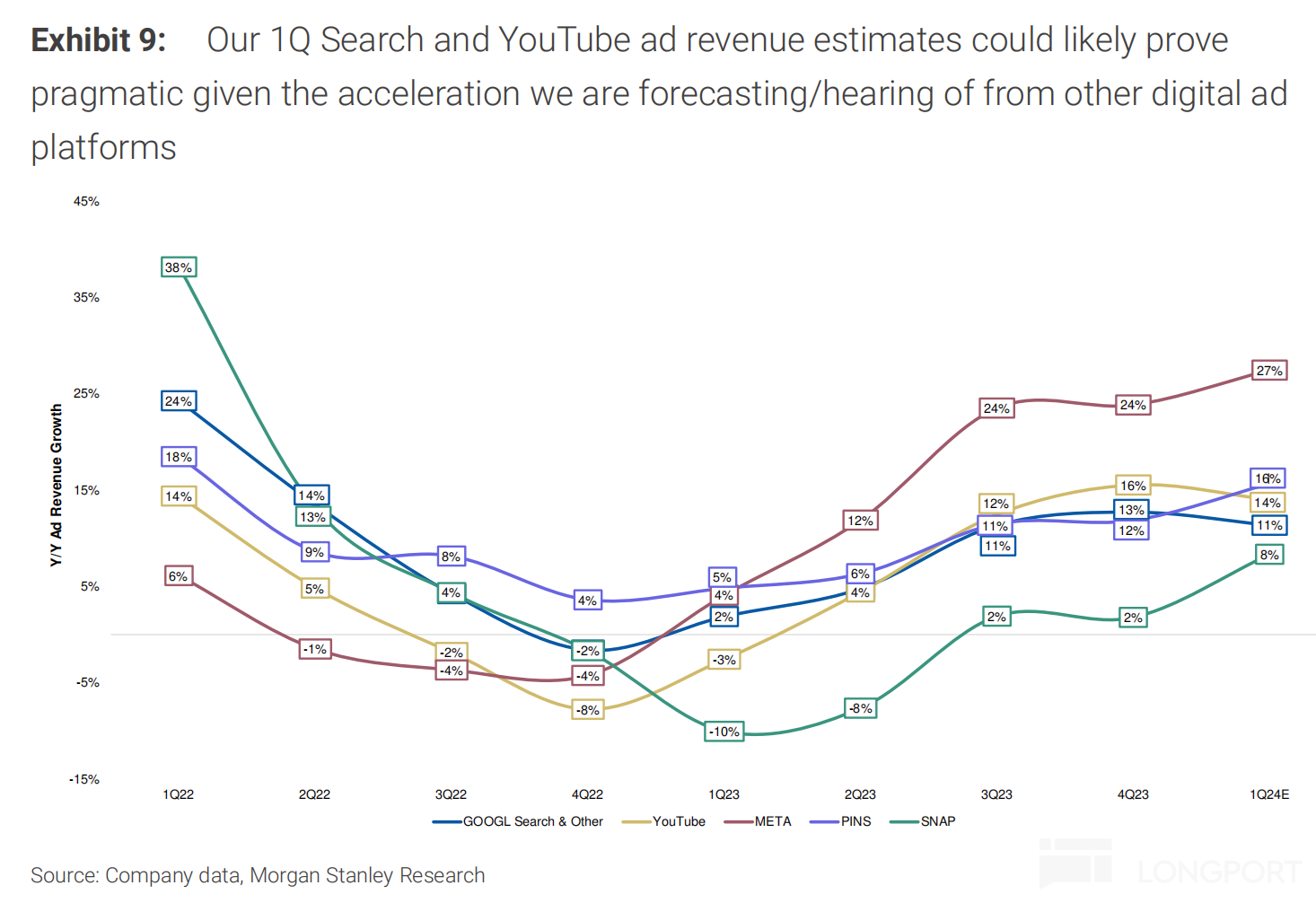

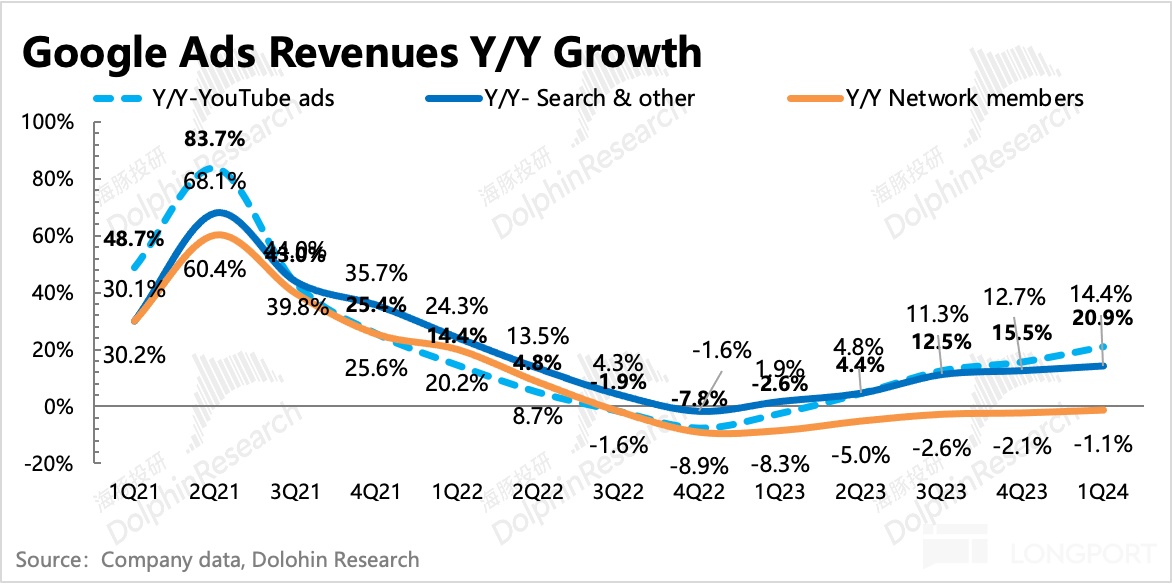

In the first quarter, advertising revenue reached 61.7 billion, with an overall growth of 13%, showing a certain acceleration compared to the previous quarter due to a low base. This aligns with the strong macro environment and the overall industry performance. However, market expectations are somewhat conservative (believing that Google's marginal trend is weaker than its peers), leading to a slight decrease in growth expectations for YouTube and search compared to the previous quarter. Later, after seeing good performance from third-party data platforms on YouTube, the growth rate was only raised by 1 percentage point, keeping the growth rate stable compared to the previous quarter.

YouTube has the highest growth rate due to its low base, and in terms of quarter-on-quarter improvement, it also has the largest magnitude, with a year-on-year growth rate of 20%, while market expectations were only at 15%.

In fact, third-party data shows that YouTube user data has been performing well recently. For example, according to Nielsen, YouTube's share of streaming TV in the United States increased by 2 percentage points year-on-year in March, possibly due to the lack of content from the film and television industry. At the same time, according to Sensor Tower, YouTube's user growth on the app side in the United States was more stable than its peers in the first quarter. Although some institutions have raised their revenue expectations for YouTube in the past month, the actual performance is still better.

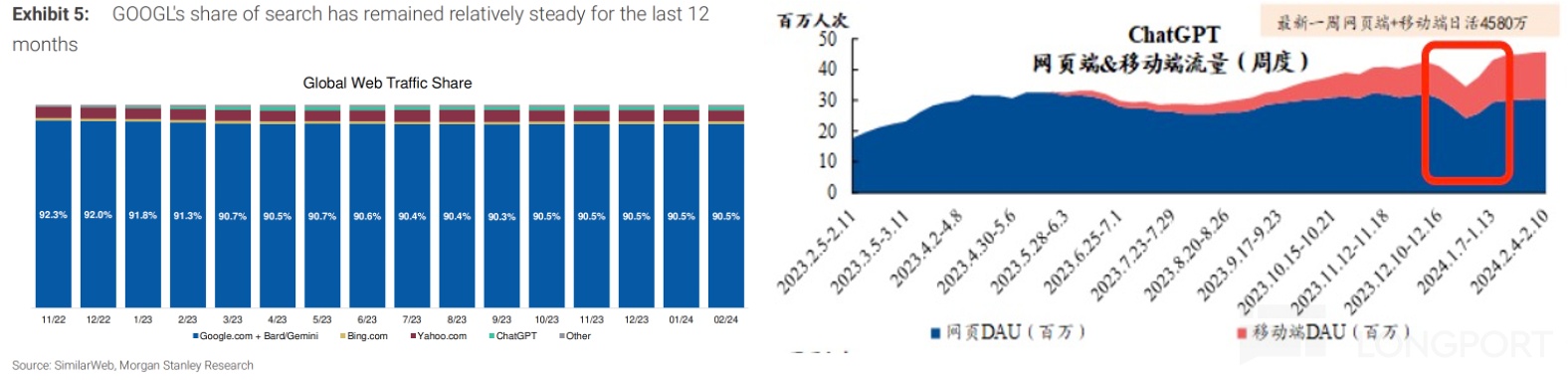

Search is where market expectations are relatively conservative. Search advertising grew by 14% year-on-year in the first quarter, while market expectations were only at 11-12%, possibly due to concerns about the erosion from new AI entries.

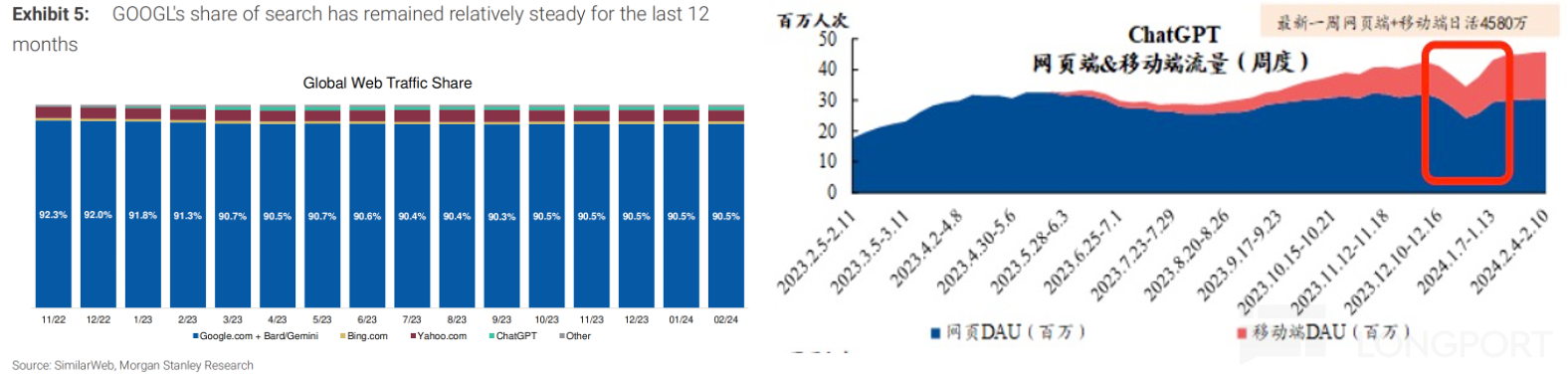

In the long run, this issue may ultimately be unavoidable. However, in the short term, Google still has defensive capabilities (leading global AI technology), and the migration of advertising budgets also involves a process that requires balancing user scenarios, user stickiness, and advertising conversion effects. Currently, according to Similarweb, Google's search market share remains relatively stable.

**Currently, AI question-and-answer platforms led by GPT are mostly used in office and learning scenarios (GPT traffic will quickly decline during holidays), and the commercialization space for advertisers is temporarily limited. However, due to the rapid development of this round of AI industry transformation, it is still necessary to closely monitor marginal changesCloud: With real AI dividends, it achieved a revenue of 9.6 billion in the first quarter, a year-on-year growth rate of 28%, and a sequential increase. Although there are some base effects, cloud services do not show obvious seasonality. Customer demand is consistent (with generally high renewal rates under no major changes), coupled with some recent introductions by management at the Next conference in early April, Dolphin believes that there should be a lot of AI bonuses for the accelerated growth in Q1.

Cloud business is B2B, so long-term trends may be related to its own product competitiveness, but short-term changes are more likely to be affected by changes in the scale of new signed contracts in the current or previous period.

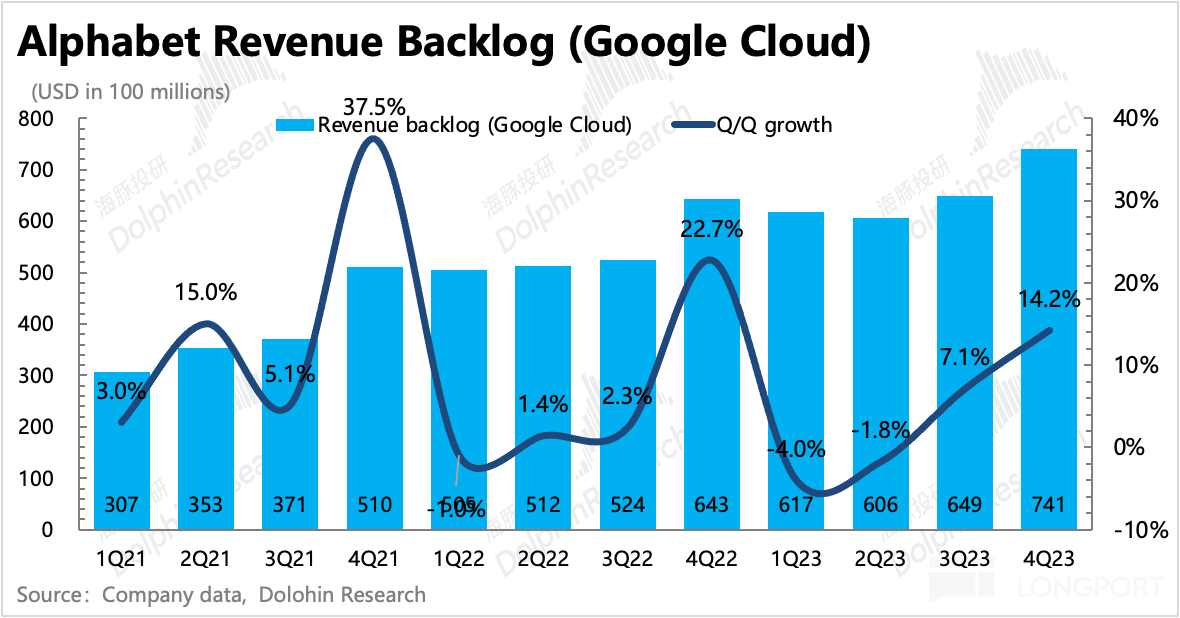

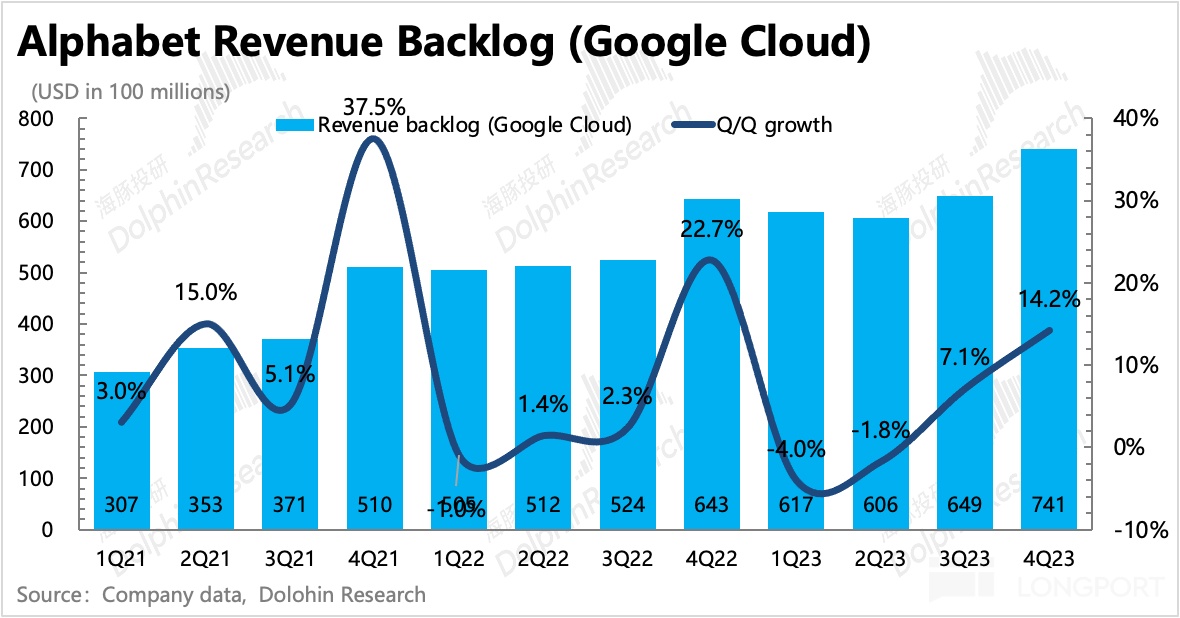

Therefore, Dolphin generally uses Google's Revenue Backlog indicator to assess short-term trends. Most of this indicator comes from cloud business, so its trend can also be seen as the trend of unfulfilled contracts in cloud business.

As of the fourth quarter (first quarter data needs to be found in the complete quarterly report from the SEC, although the data is lagging, the overall trend can still be seen), Google Cloud's backlog contracts continued to increase by 14.2% on a sequential basis, combined with industry changes, the AI bonus is very obvious.

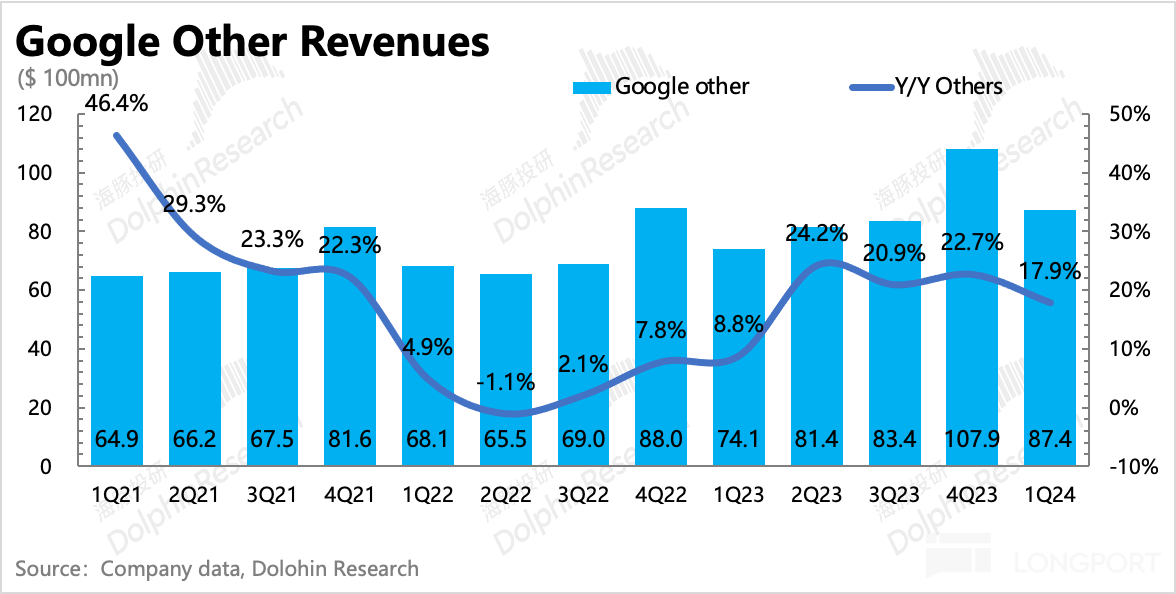

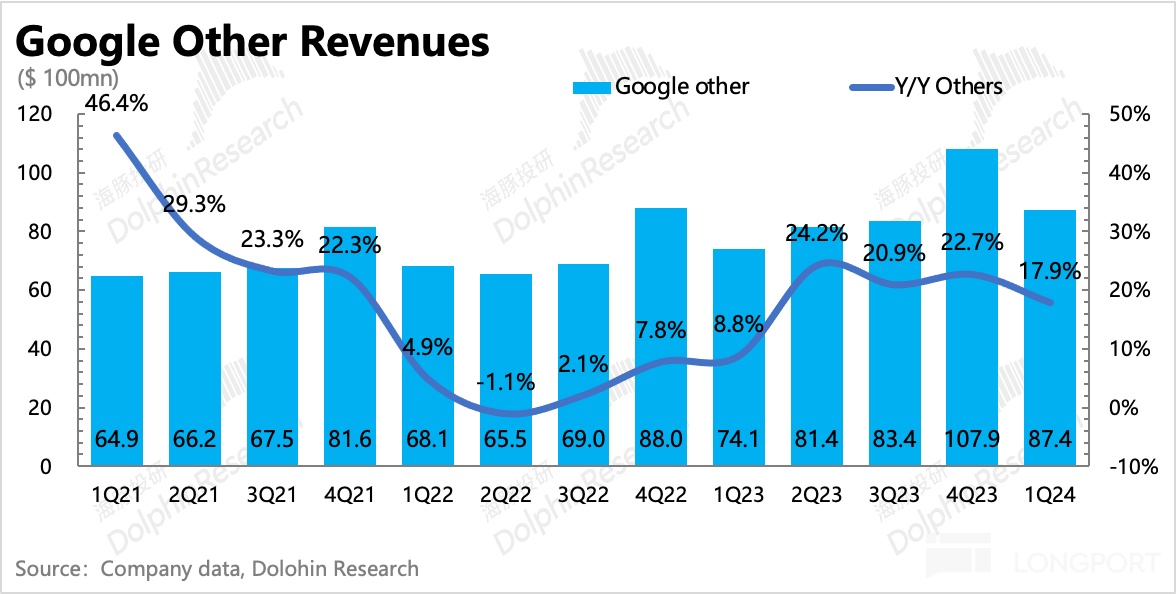

Other businesses: Unexpectedly slowed down in the first quarter, with a year-on-year growth of 18%. This part of the revenue is mainly composed of YouTube subscriptions (TV, music, etc.), Google Play, Google, One, hardware (Pixel phones and smart home appliances Nest), etc. Dolphin speculates that this may be mainly related to the impact of current Google Play revenue after the reduction in revenue sharing, and the flat sales of hardware.

However, YouTube subscriptions (TV & Music) should still be doing well. Third-party Nielsen data shows a significant increase in YouTube's TV share in MarchThree, Layoffs Continue "Broadly", Capital Expenditure Doubles

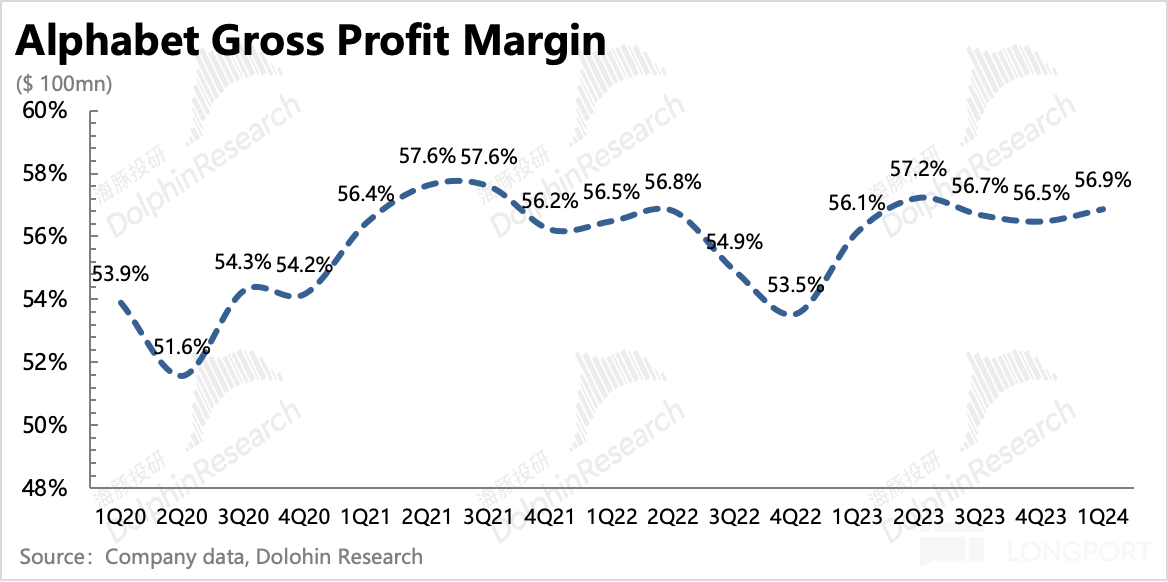

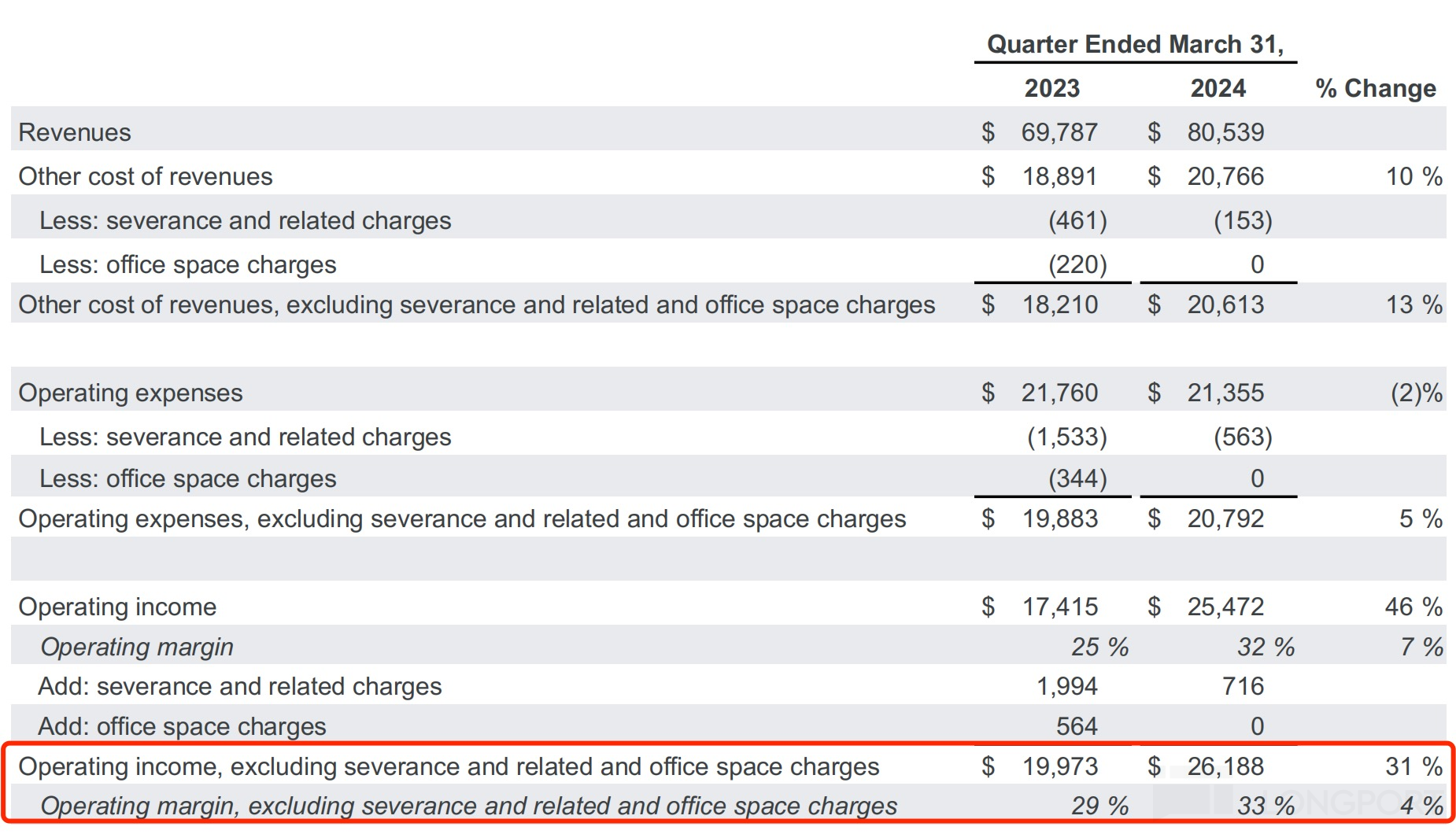

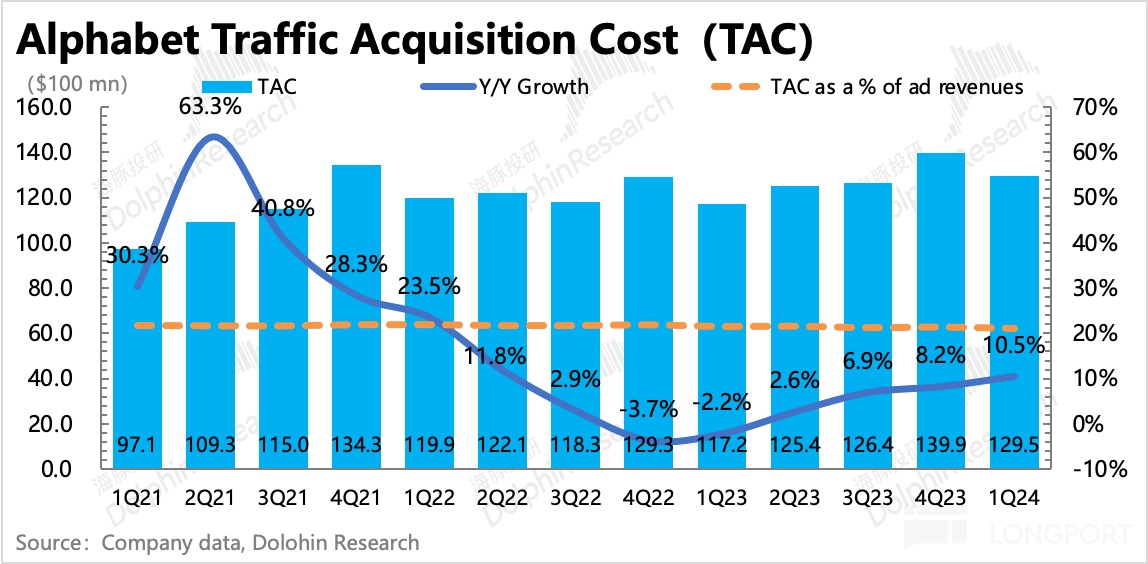

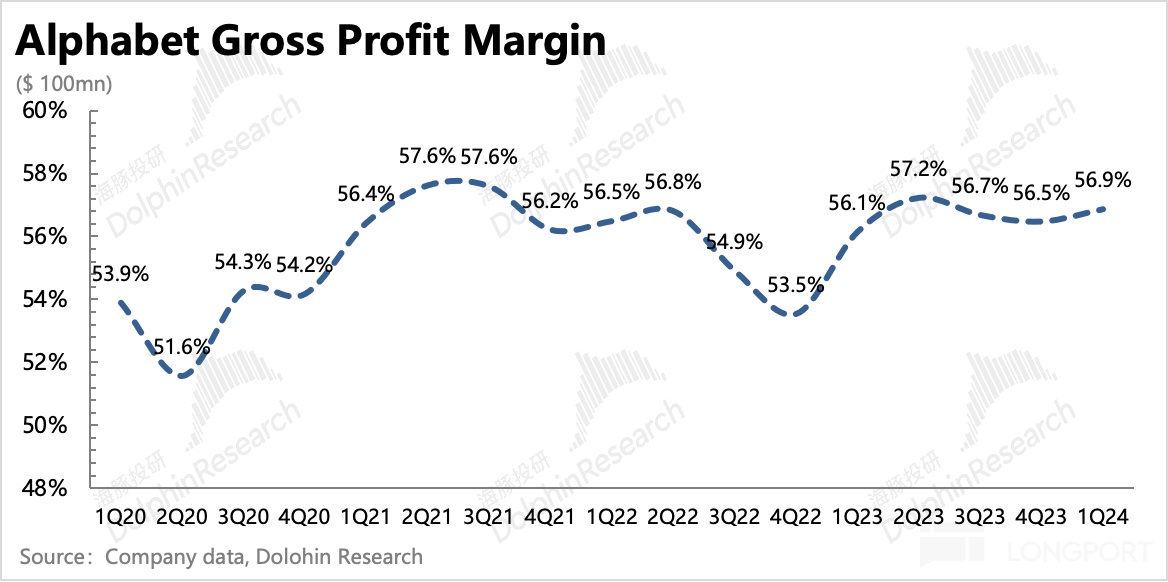

In the first quarter, driven by revenue growth and changes in business structure (weaker growth in low-margin alliance advertising), optimization of traffic costs, Google's gross margin increased by 2 percentage points (the dividend period of server depreciation adjustment ended last quarter). At the same time, the layoffs that were postponed last quarter continued in the first quarter, resulting in a decrease of 1600 employees compared to the previous quarter.

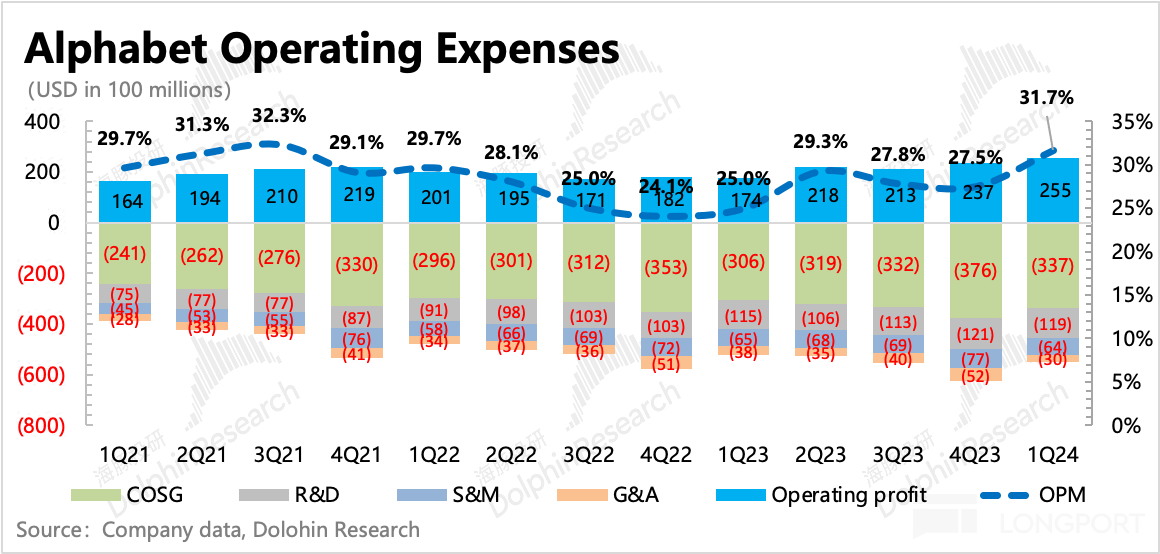

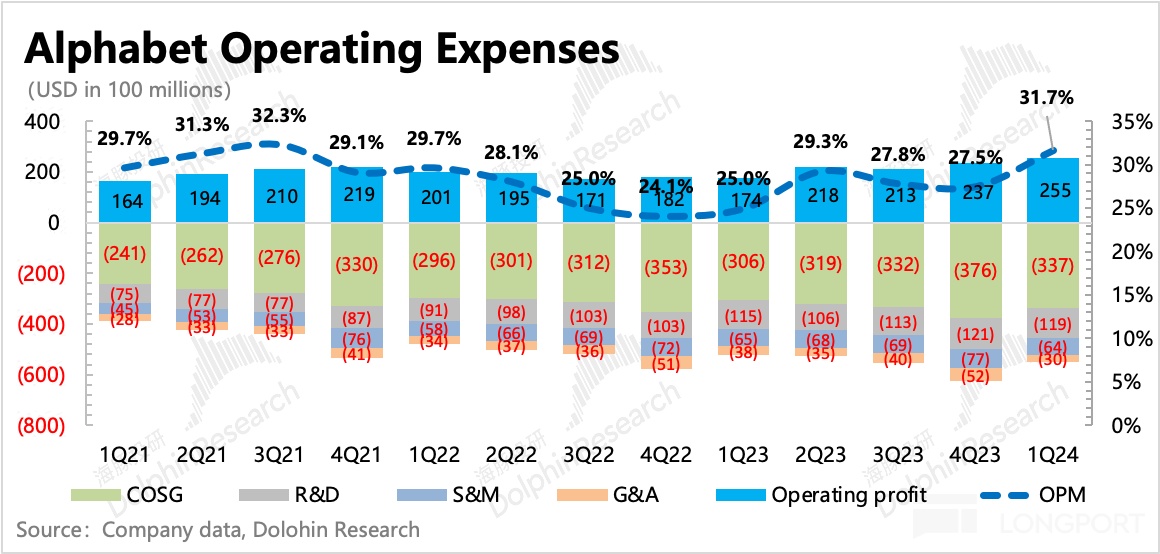

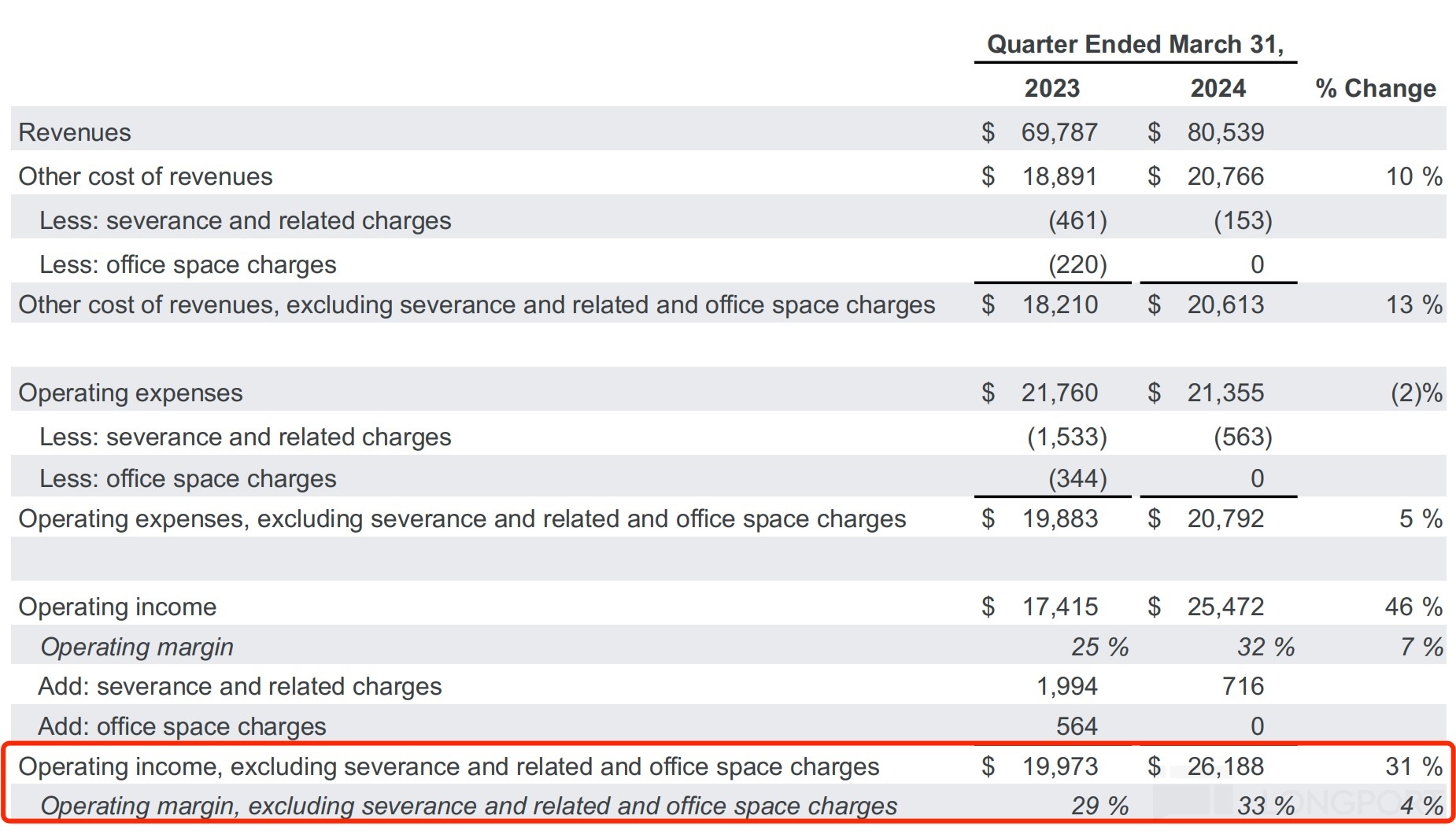

Looking at the changes in expenses, it mainly reflects the optimization of sales and administrative personnel, with sales expenses decreasing by 2% year-on-year and management expenses decreasing by 20% year-on-year. The final operating profit was 25.5 billion, with a profit margin of 31.6%. After excluding the expenses of layoffs compensation, the actual operating profit margin has reached 33%.

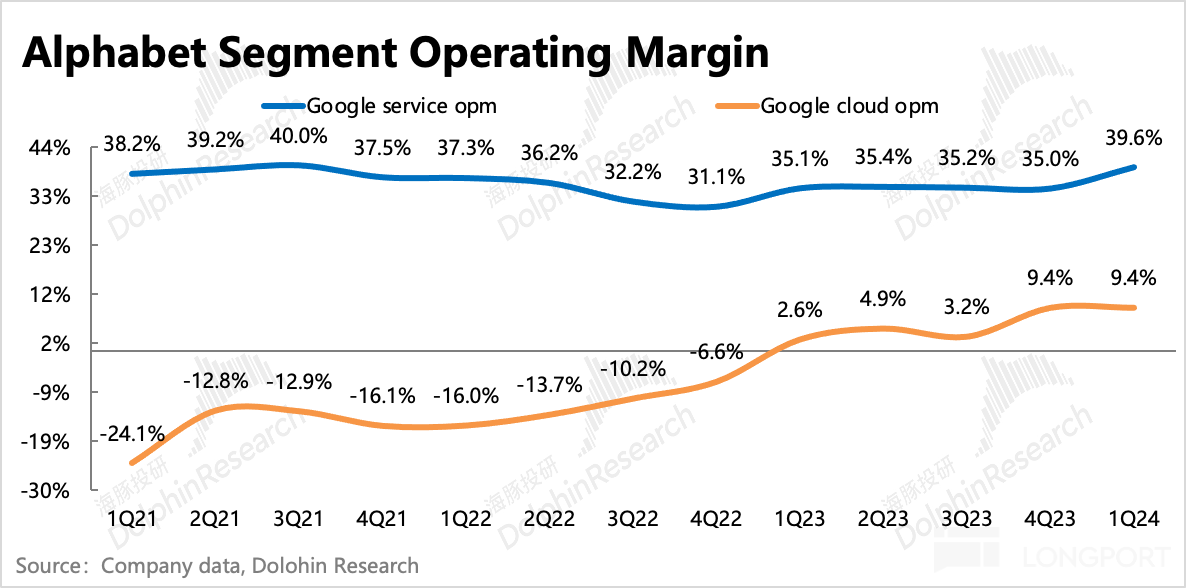

In terms of business segments, the profit margin in the first quarter exceeded expectations, mainly reflected in Google's advertising-based service business, with an operating profit margin approaching 40%. If we consider the impact of layoffs compensation, the actual profit margin has definitely reached a new high.

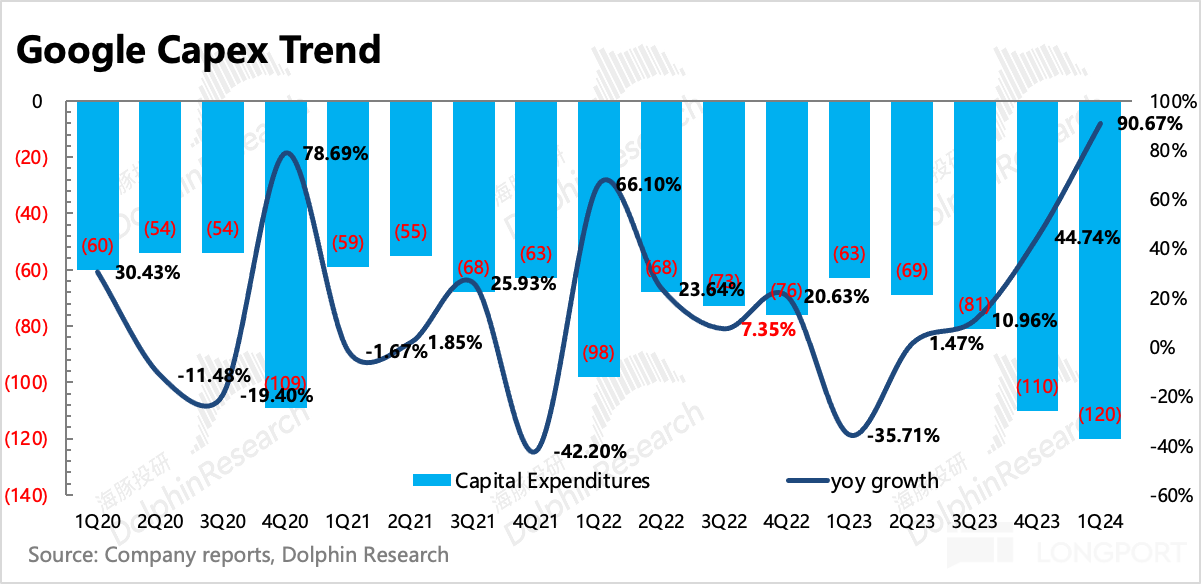

In terms of medium to long-term infrastructure investment, it was already evident last quarter that due to the industry's shortage of computing power, the company significantly increased its investment in AI—capital expenditure has increased significantly. During the fourth quarter conference call, management also expressed a clear plan to significantly increase Capex this year, as a new investment cycle brought by AI will restart. As expected, Google's Capex in Q1 reached 12 billion, nearly doubling year-on-year

Dolphin Research on Google Historical Collection:

Earnings Season

January 31, 2024 Earnings Call " AI Management Efficiency, AI Product Innovation, AI Expenditure... (Google 4Q23 Earnings Call Summary)"

January 31, 2024 Earnings Review " Google: Expectations Too Enthusiastic, Top Dog Pours Cold Water"

October 25, 2023 Earnings Call " Google: Cloud Slows Down Due to Enterprise Customer Capex Optimization, Signs of Stabilization Seen (3Q23 Performance Call Summary)"

October 25, 2023 Earnings Review " Google: Ads Still Dominant, Cloud Slowdown Due to "AI Incompetence"?"

July 26, 2023 Earnings Call " Google: Investing in AI, Benefiting from AI (2Q23 Performance Call Summary)"

July 26, 2023 Earnings Review " Google: Breaking Doubts, Will the Ad Leader Rise Again?"

April 26, 2023 Earnings Call " AI Competition Never Stops, Focus on Search and Cloud Implementation (Google 1Q23 Earnings Call Summary)"

April 26, 2023 Earnings Review " Google: Exceeding Expectations Against the Trend? Joy Comes with Concerns"

February 3, 2023 Earnings Review " Focus on Revenue Growth Rather Than Simply Cutting Costs (Google 4Q22 Earnings Call Summary)"2023 年 2 月 3 日财报点评"Short-term pressure is not small, Google needs to learn from Meta"

2022 年 10 月 26 日电话会"Short-term optimization of resources, opportunities still lie in search and YouTube (Google 3Q22 conference call summary)"

2022 年 10 月 26 日财报点评"Google: Decline approaching, the king of advertising has fallen"

2022 年 7 月 27 日电话会"Google: Economic highs in the second half of the year with 'uncertainty', focusing investments in areas with better long-term prospects (conference call summary)"

2022 年 7 月 27 日财报点评"Google: 'Tough exam' under the expectation of a thunderstorm"

2022 年 4 月 27 日电话会"Management avoids discussing TikTok, but the emphasis on Shorts still reflects intensified competition (Google conference call summary)"

2022 年 4 月 27 日财报点评"Google: Facing headwinds, the big brother is also struggling"

2022 年 2 月 2 日电话会"Increasing investments, accelerating hiring, Google actively seeks expansion (conference call summary)"

2022 年 2 月 2 日财报点评"Blinding performance, rare stock split, Google is set to soar again"

In-depth

2023 年 12 月 20 日"Google: Gemini can't solve the 'little devil' entanglement, next year won't be easy"

2023 年 6 月 14 日"In-depth article: Is ChatGPT the 'Thanos snap' that kills Google?"February 21, 2023 " US Stock Ads: After TikTok, is ChatGPT about to start a new "revolution"? "

July 1, 2022 " TikTok wants to teach the "big brothers" how to work, Google and Meta are about to change "

February 17, 2022 " Internet Advertising Overview - Google: Watching the changes "

February 22, 2021 " Dolphin Research: Breaking down Google - Has the recovery trend of the advertising leader ended? "

November 23, 2021 " Google: Performance and stock price soaring, strong recovery is the theme of this year "

Risk Disclosure and Statement of this Article: Dolphin Research Disclaimer and General Disclosure