Tencent: Making Money with WeChat is Easy for the Stock King Nearby input: ====== 注意!海豚君提示这些租房陷阱要避免 ====== output: Attention! Dolphin Analyst reminds you to avoid these Renting Traps

Hello everyone, I am Dolphin Analyst!

After Hong Kong stock market on November 16th Beijing time, Tencent Holdings Limited (HKG: 0700) released its 2022 Q3 financial report. From a market perspective, the financial report mainly focused on two points: 1) the recovery status of the business affected by the pandemic; and 2) cost reduction and efficiency enhancement increasing profits. The financial report continues the path of "income recovery and profit acceleration" and maintains a similar style as Tencent Music (NYSE: TME), which released its financial report yesterday.

In addition to the fundamentals, Tencent also announced another important news with the financial report. "Tencent will distribute most of its Meituan shares to its own shareholders—every 10 shares will receive 1 share of Meituan Class B shares." Based on the registered shareholding situation on November 16th, it is expected that Tencent will distribute 0.96 billion Meituan shares to its shareholders, which represents more than 90.9% of Tencent's holdings in Meituan. After the distribution, Tencent's shareholding percentage in Meituan will decrease from 17% to 1.5%.

Tencent's almost-clearance-type reduction of its holdings, which contradicts its two denials of selling earlier in August and October, is similar to the reduction activity by JD.com (NASDAQ: JD) and Sea Group (NYSE: SE) at the end of last year. Dolphin Analyst believes that the sale of equity assets under its subsidiaries could be the operation Tencent executed in order to meet the requirements for obtaining its financial license. Dolphin Analyst has warned several times this year about the risk of Tencent’s disposal of invested companies. In our comment "The Butterfly Effect of Ant Group: Will Tencent dump Meituan and Pinduoduo?" published at the beginning of this year, we also listed the names of companies that Tencent is expected to sell. Losing Tencent as a long-term shareholder is not a good thing for the invested company. However, for Tencent's shareholders, it is a "sunshine" benefit distribution.

Looking back at the contents of this financial report, in our previous review, we talked about Tencent's fundamental marginal turning point after the inflection point in the regulatory environment. The uphill road is right ahead. Furthermore, the management also indicated a timeline for the "return to growth" issue that more investors care about in the following conference call. Therefore, the significance of the Q3 financial report is to pay attention to the actual implementation progress of various business lines in the second half of the year.

Detailed results are as follows:

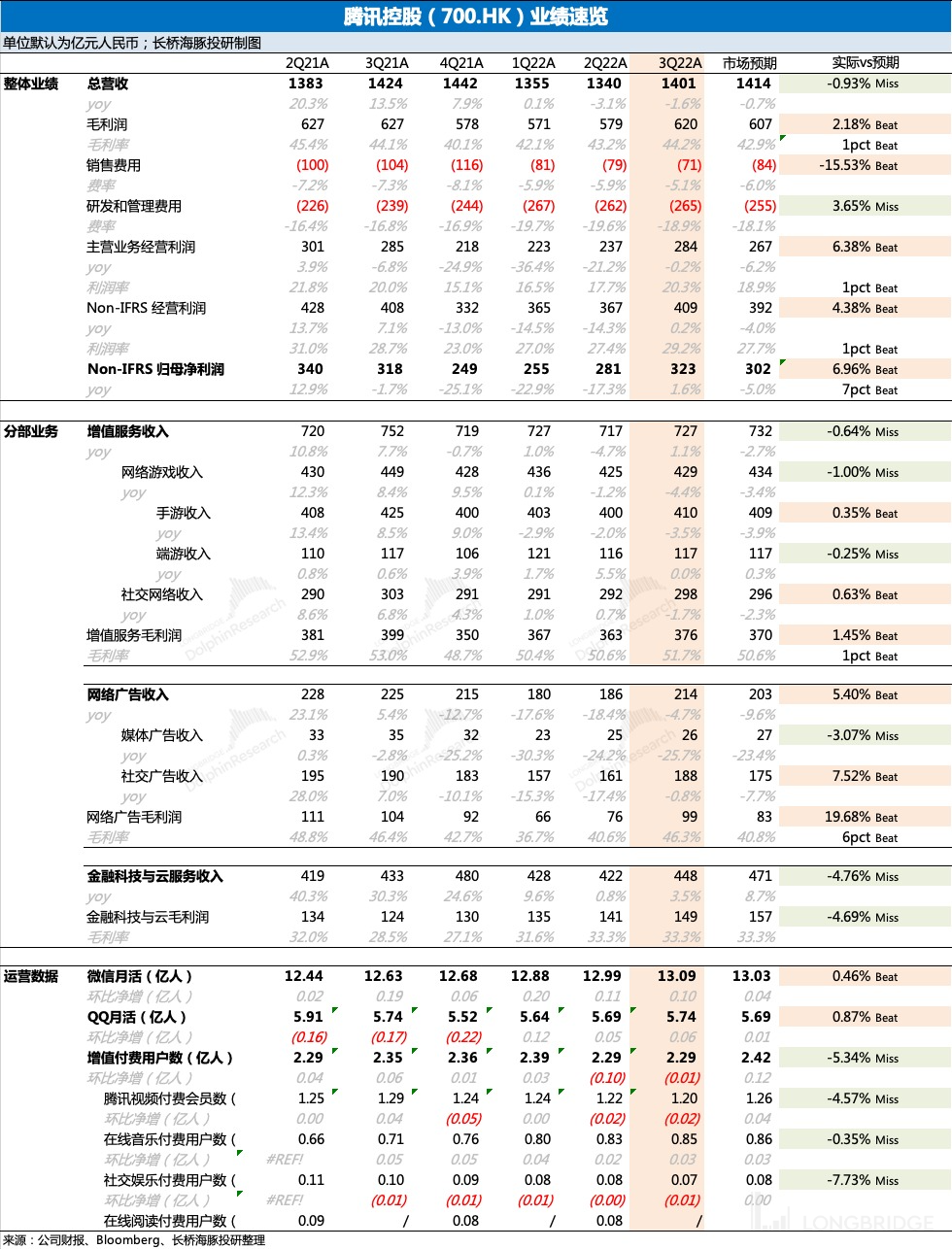

"1. Income recovery: The expected recovery of Q3 revenue, with a YoY decline of 1.6%, slightly lower than market expectations. The major highlight is "advertisement business recovery, with a YoY decline of 4.7%, significantly exceeding the expectations of most investment banks (-8% to -12%). Although the outbreak in Shanghai has ended, the scattered and repetitive outbreaks across the country still have an impact on the entire advertising market. This may be why the market remains slightly conservative about Tencent's advertising business. However, CTR data also showed that online advertising performed significantly better than offline advertising. In addition to the dividends that followed the industry's recovery, commercialization of the entire WeChat ecosystem, such as video ads and mini-program ads, is the main driving force behind exceeding expectations in advertising." 2. Profit Release: The profit in the third quarter was the highlight of the entire financial report. The adjusted net profit attributable to the parent has turned positive, and the speed of recovery has significantly exceeded market expectations. The rapid repair of advertising business is beneficial to improving the overall gross profit margin level. In addition, cost reduction and efficiency enhancement continue to be reflected in financial indicators. The key to increasing efficiency is still the massive reduction in promotion and marketing expenses. In addition, layoffs and streamlining also continue, with the number of employees in the third quarter decreasing by 1879 compared to the previous quarter, and employee welfare expenses rapidly decreasing to single-digit growth.

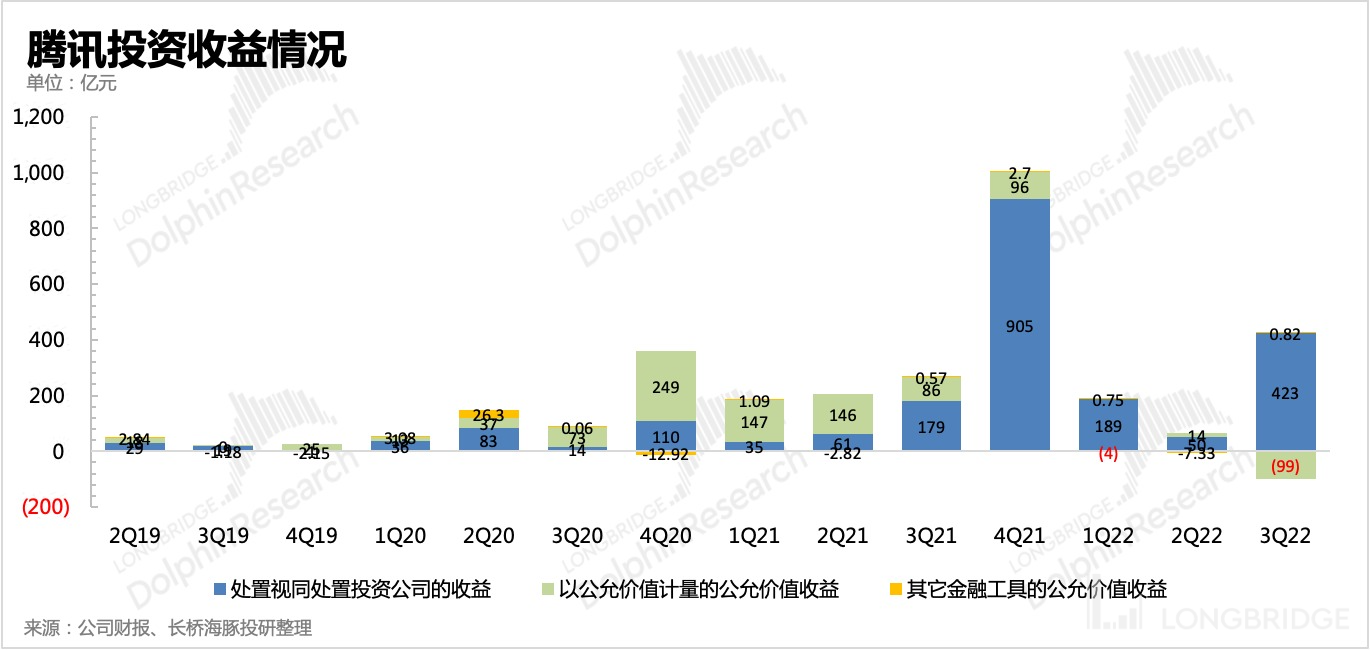

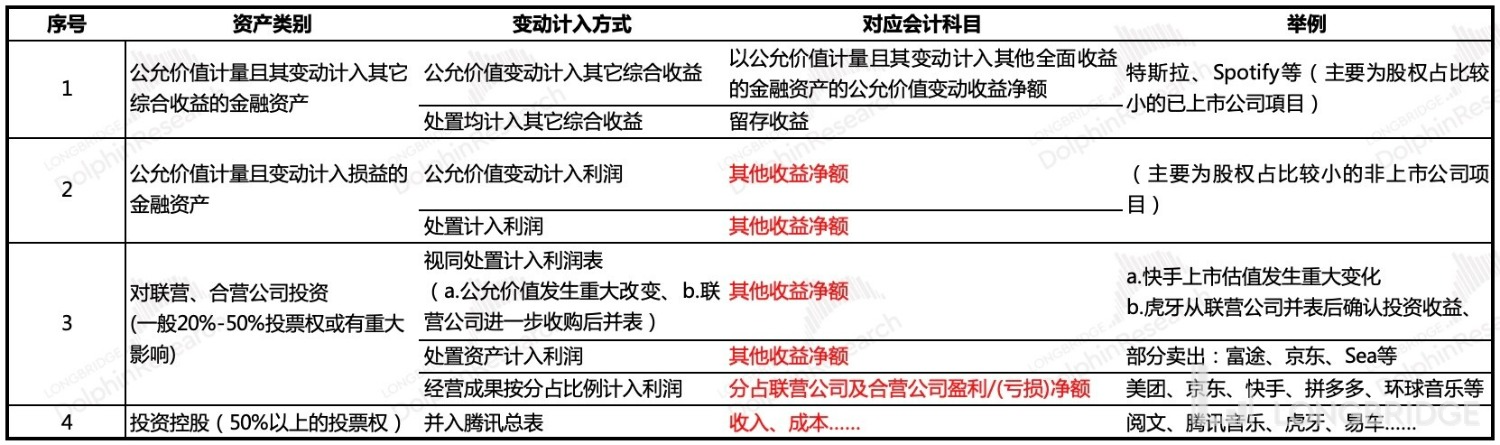

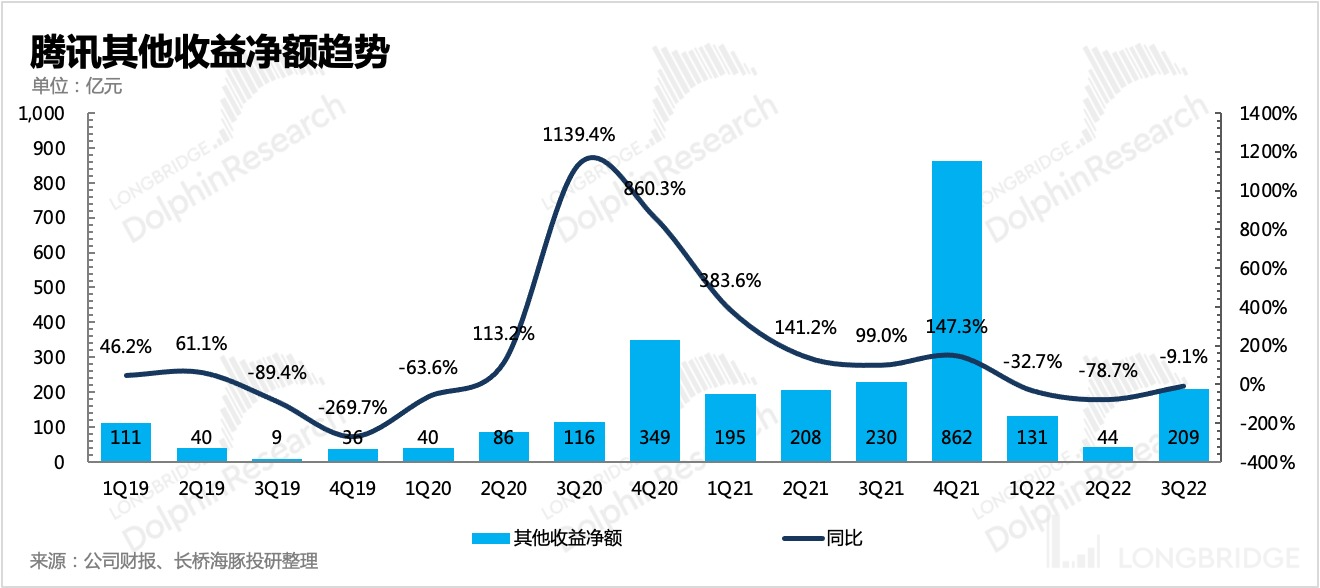

3. Investment Income: The main source of abnormal movement in the third quarter was the reclassification of equity assets. Anyu Xin resigned as a senior executive of Sea in the third quarter. From then on, Sea is no longer an associated company of Tencent's equity assets, but is classified as a general financial asset measured at fair value, which confirmed the profit and loss of the reclassification of RMB 41.3 billion. It is regarded as a disposal loss or gain and included in other net income, resulting in significant fluctuations in investment income in this quarter.

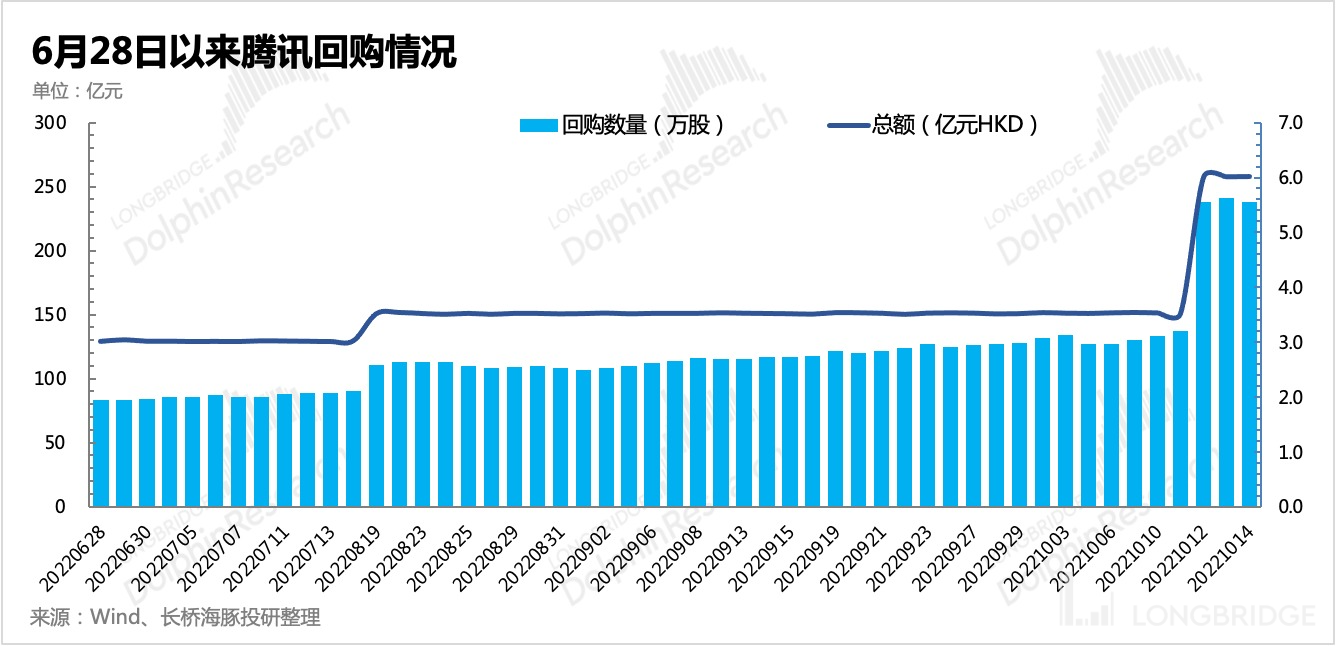

4. Repurchase and Shareholding Reduction by Major Shareholders: From June 28th to October 14th, Tencent has repurchased more than 60 million shares, with a total of over HKD 18 billion used, and Tencent may continue to repurchase shares after the sensitive financial report period. From June 28th to September 2nd, major shareholders reduced their holdings of Tencent shares by 76 million shares. At present, NAV and stock discount rates of major shareholders have narrowed.

5. Operating status of segmented businesses, highlighted by the Dolphin Analyst

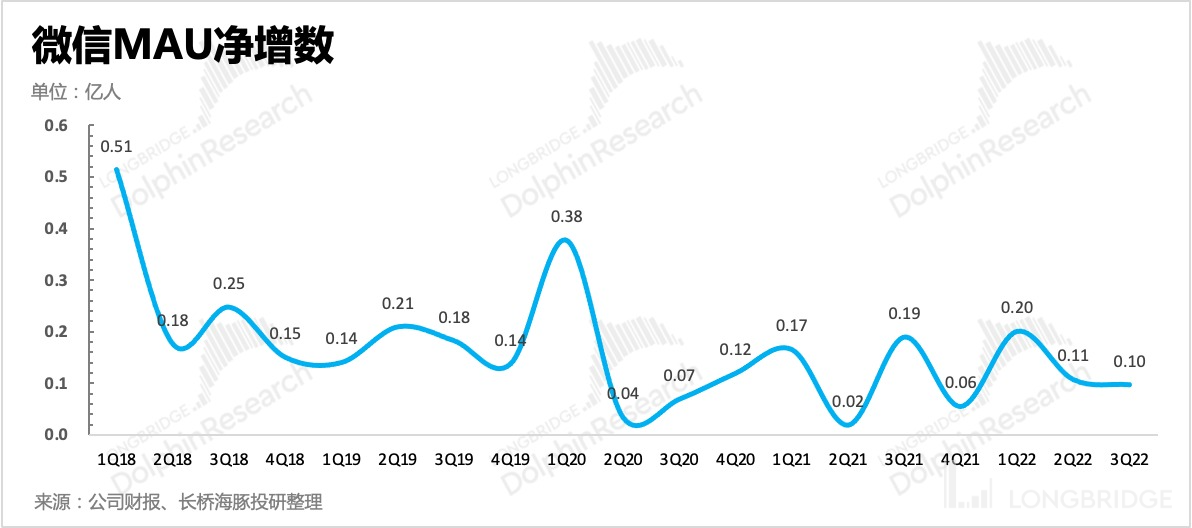

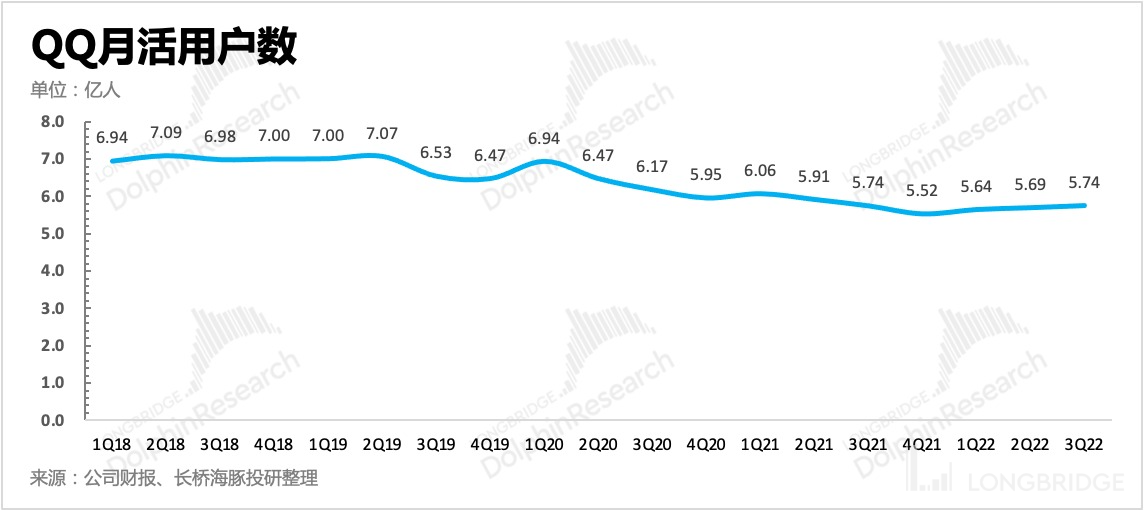

(1) User Ecology: The short video platform Video Number continues to grow, WeChat maintains steady growth as previously expected and surpassed 1.3 billion. In the third quarter, the QQ active user count continued to rebound slightly, mainly benefiting from the peak season during the summer vacation. In addition, Super QQ Show is also expanding its penetration and influence. According to third-party data, Tencent's total share of time spent remained basically stable, but WeChat's time spent increased significantly in the third quarter. The Dolphin Analyst is optimistic about the long-term value of Video Number, Mini Programs, and the entire WeChat ecosystem.

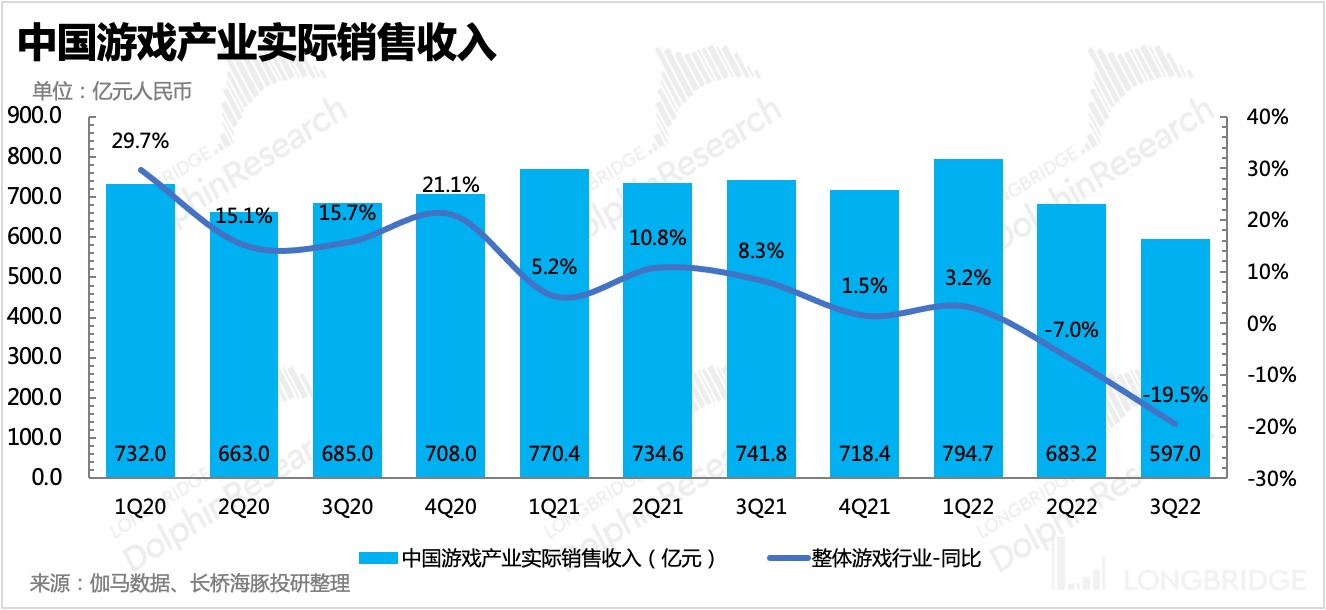

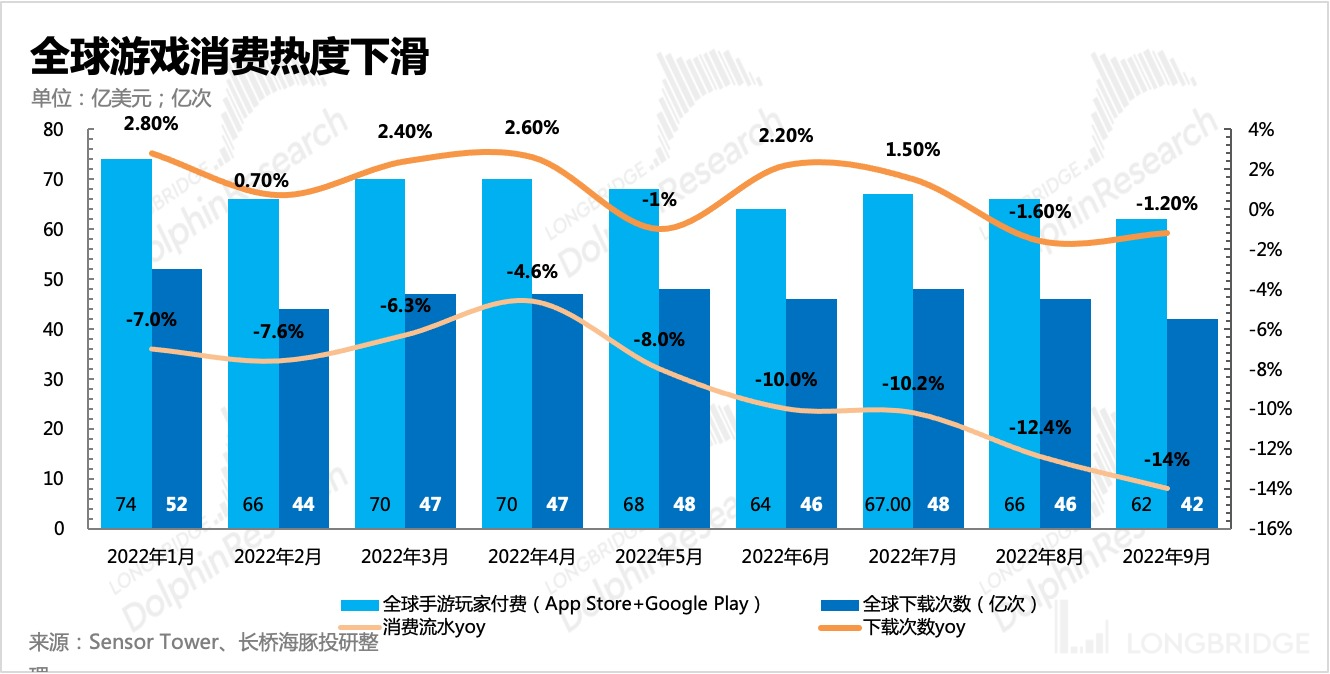

(2) Gaming: The global cold winter is an indisputable fact. Under the sluggish demand, gaming companies need to rely on their own product cycles to survive. In the third quarter, Tencent launched mainly proxy games, and only three self-developed games. Due to the few new releases, and the impact of high statistical base of the under-aged protection policy in July and August, domestic games saw a year-on-year decrease of 7%, slightly lower than market expectations.

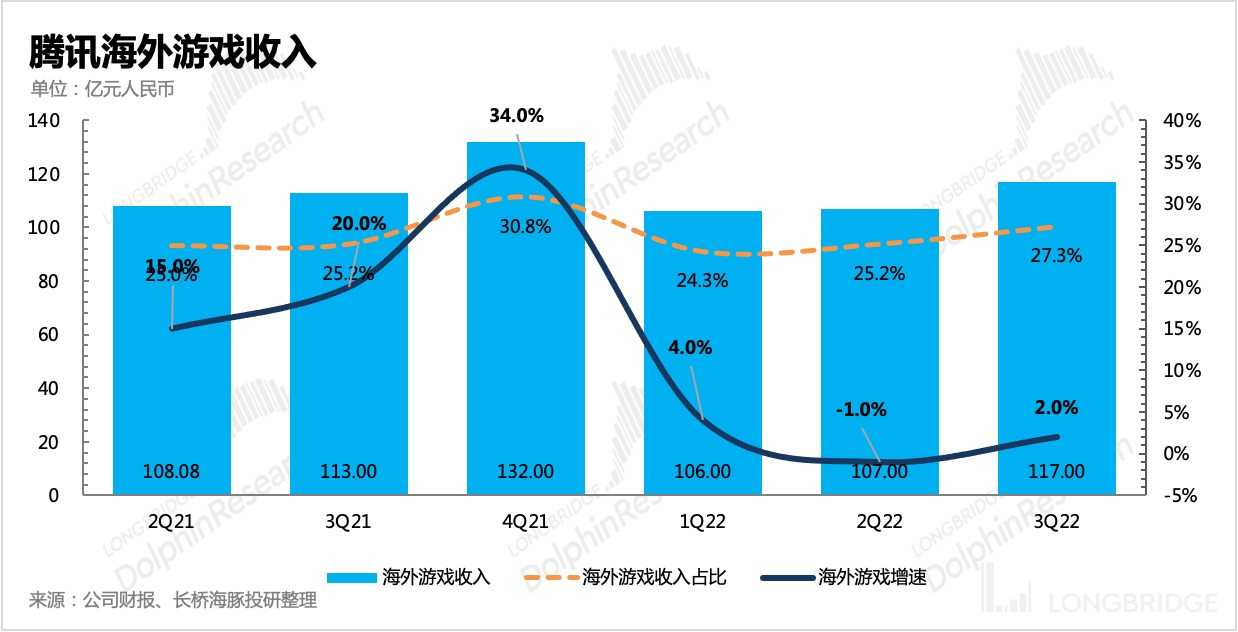

However, the overseas market performance was impressive. Although "PUBG Mobile" declined significantly, due to the launch of "Perfect World" (developed by Perfect World Mobile) overseas in August, and the increasing heat of major updates in "Clash of Clans", as well as new breakthroughs in "VALORANT", Tencent's overseas gaming revenue increased by 2% despite the global decline of nearly 20%.

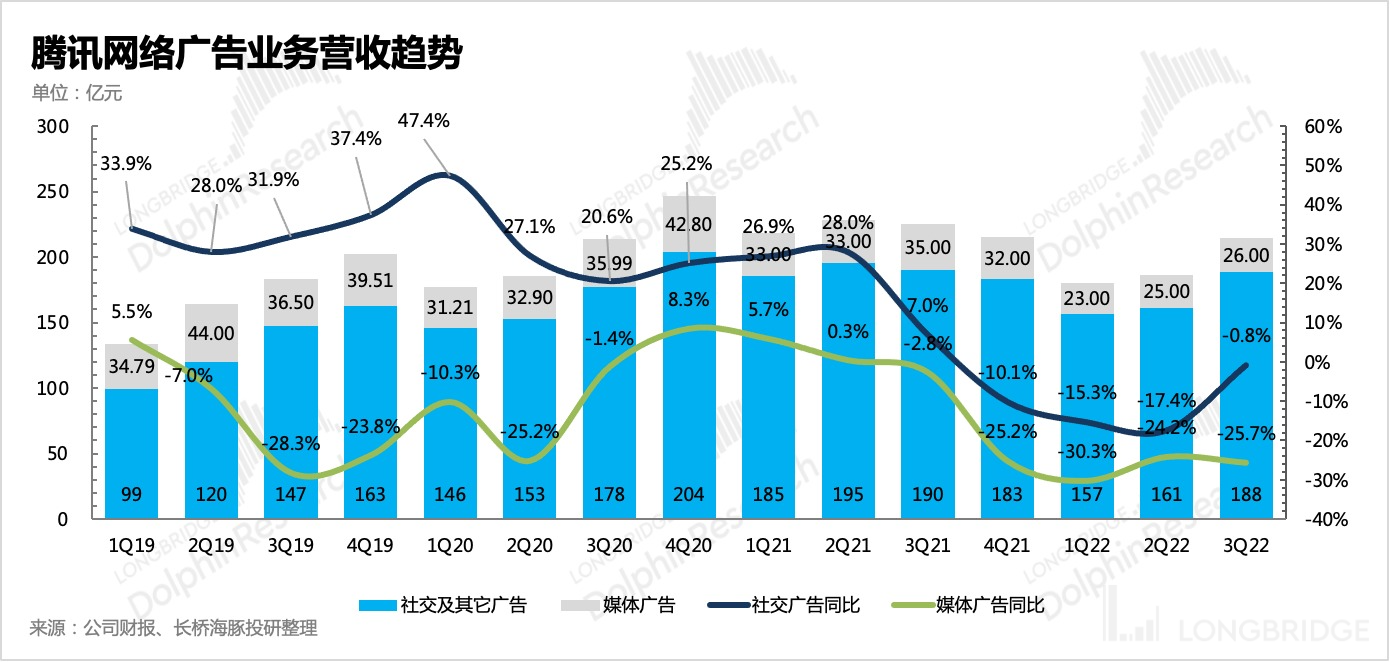

(3) Advertising: The third quarter showed a better-than-expected recovery, with a nearly 5% decline compared to a 18% year-on-year decline in the second quarter. Especially in social advertising, it has almost caught up with last year's revenue, showing the strong commercial potential of the WeChat ecosystem. On the one hand, the impact of low baselines, and on the other hand, from a month-on-month perspective, the third quarter has shown a relatively strong recovery. However, the overall industry performance in the third quarter was not good, with online outperforming offline. Compared with media and social advertising, the third-quarter advertising restoration more reflects the commercial power of WeChat ecology.

Due to the strict control of mobile alliance advertising relying on external traffic and turning to more self-owned channels such as WeChat, the overall advertising gross profit margin has significantly increased to the level of the first half of last year.

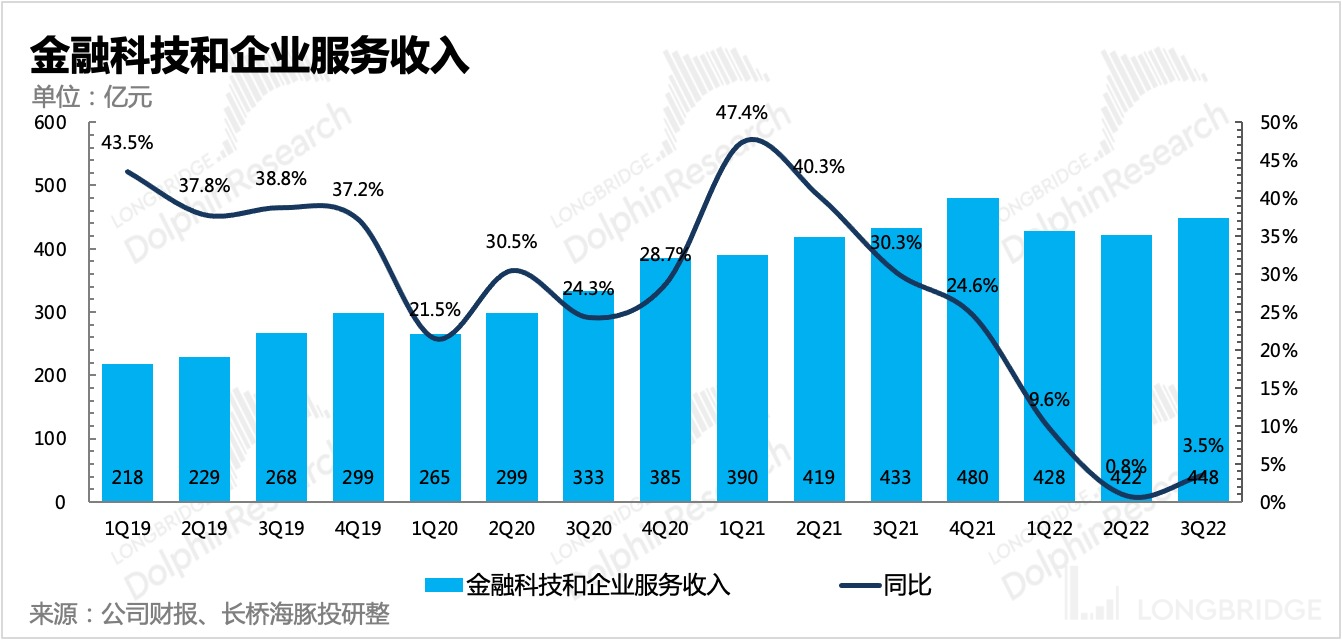

(4) Kingsoft and the Cloud: 4% year-on-year growth, lower than market expectations. In addition to the impact of the epidemic on the use of WeChat offline payment scenarios in the third quarter, despite this, commercial payments in the third quarter still showed double-digit growth. Dolphin Analyst is relatively confident about Tencent's payment competitive advantages, and payment will rebound quickly as the epidemic is relaxed.

The merged cloud business is probably the main reason for dragging down overall revenue growth. Currently, the cloud business is still in a strategic adjustment stage, reducing targeted and subcontracted products and focusing on optimizing the profitability of the business itself.

It is expected that this year's fourth quarter will still be affected by this, but with the adjustment of epidemic policies and improving economic expectations, the degree of decline will be reduced. In the last quarter's conference call, management also gave guidance that the cloud business will resume its growth next year.

(5) Digital Content The entire sector is in a state of business contraction and optimized profit models, so a decline in revenue is inevitable. Tencent Music, which released its financial report yesterday, mainly faced pressure from the weakening of paid demand for live streaming and K songs. The number of paid users for Tencent Video lost 2 million month-on-month in the third quarter, but the overall profit of this sector has improved due to the slowdown in content cost growth and the decrease in live streaming revenue-sharing. The gross margin of value-added services in the third quarter increased by 1 percentage point month-on-month.

Detailed comparison of detailed indicators and market expectations are as follows

Dolphin Analyst's viewpoint

Overall, the operating conditions and trends reflected in the third-quarter report are what investors want to see. Although some investment banks may have expected higher performance in some businesses, overall, the problem is not very serious. The unexpected release of profit exceeding expectations and the distribution of Meituan's stocks are also surprises.

More importantly, the marginal changes in the environment, the clearance of policy risks, the shift in the wind direction (the People's Daily comments positively on the Internet, the opinions of the People's Daily Finance on the value of video games, and the deep cooperation between Tencent and state-owned enterprise operators), and the market's expectations of economic improvements under more scientific epidemic prevention and control measures, all help Tencent's performance to accelerate its recovery and valuation to rebound and repair.

Finally, Dolphin Analyst still needs to remind that due to the requirements of the financial control license, Tencent's actions of selling its equity assets may continue, and companies such as Kuaishou (competing with Video Account) and Pinduoduo (mature assets) pose considerable risks and need to be monitored at all times. Also, the Dolphin Analyst has reviewed several discussions on this topic earlier this year:

December 23, 2021 "Tencent "bye-bye" JD: happy breakup or painful separation?"

January 5, 2022 "Is Sea's threat hurting Tencent's younger siblings in "mini-Tencent"? The meaning of this matter is different."

January 12, 2022 "Revisiting the value of Tencent's "half-life" divestments."

January 17, 2022 "The Butterfly Effect of Ant: Will Tencent dump Meituan and Pinduoduo?"

Detailed interpretation of the financial report this time

I.

User ecology: Tencent's stable and expanding ecology is the cornerstone of growth.

In the third quarter, WeChat continued to steadily expand with the help of video accounts, with a net increase of 10 million users in a single quarter. As of the end of September, the monthly active users reached 1.309 billion, easily surpassing the 1.3 billion mark, while QQ also increased by 6 million users due to the peak summer season. From third-party data, Tencent's share of usage time is gradually stabilizing, but WeChat's usage time has increased rapidly in the third quarter. The long-term value mining of the entire WeChat ecosystem is still the market's highest expectations for Tencent's medium- to long-term growth momentum.

I.

Game: Under the industry's downturn, growth depends on richer product cycles.

In the third quarter, network game revenue was 42.9 billion yuan, a year-on-year decrease of 4.4%. The global gaming market is all in a harsh winter. ("The Winter of Games has Come. Is There a Warm Spring Anywhere?")[^fn1]

[^fn1]: This English sentence is not part of the actual input text but is added for reference and should not be translated.

In the third quarter, regardless of the domestic market in China, Chinese gaming companies going global, or the global gaming market, all are accelerating their decline. Hence, the only way to overcome the cyclical downturn in the industry is to rely on a more diversified product line.

Furthermore, minor protection policies will be implemented starting from September 1, so the impact of the high base effect will still be felt for two months in the third quarter. In July, Tencent's gaming minors' amount of time spent has decreased by 97% YoY and the proportion in total game user time spent is already very small.

The number of hand games Tencent launched in the domestic market in the third quarter is mainly through agent-assisted, with only three new self-developed games, two of which have IPs, "League of Legends Esports Manager" and "One-Punch Man". However, "League of Legends Esports Manager" is average in performance and is not as popular as its IP, indicating that Tencent still needs to improve its planning and operations in non-MOBA mobile games.

As for older games, they are relatively stable as a whole, but due to the implementation of minor protection policies and weakened willingness of users to spend due to the economic downturn, the originally expected income surge during summer vacation in Q3 did not manifest.

Thus, the final revenue of the domestic gaming market was 31.2 billion, a decrease of 7% YoY.

In contrast, the overseas market has performed relatively well, growing by 3% against the trend, and its revenue share in the overall game has risen to 27%. Although "PUBG Mobile" has declined quite a bit, Tencent's overseas games have shown quite good anti-pressure ability especially with the launch of "Fantasy Tower" (perfect development) in August alongside "VALORANT" hitting a new record, and the blockbuster return of "Clash of Clans". Consequently, despite the global YoY reduction of nearly 20%, Tencent's overseas games' resistance is quite good. Upcoming self-developed games include "Clash Mini", "Arena of Valor International Edition", "ValorantM," as well as the adaptation of "Avatar: Return to Pandora" (Dragon Quest Development).

In overseas actions, Tencent did not stop investing in the third quarter. The biggest move is the acquisition of 16.25% stake in From Software, the game developer of the high fever annual game "Elden Ring".

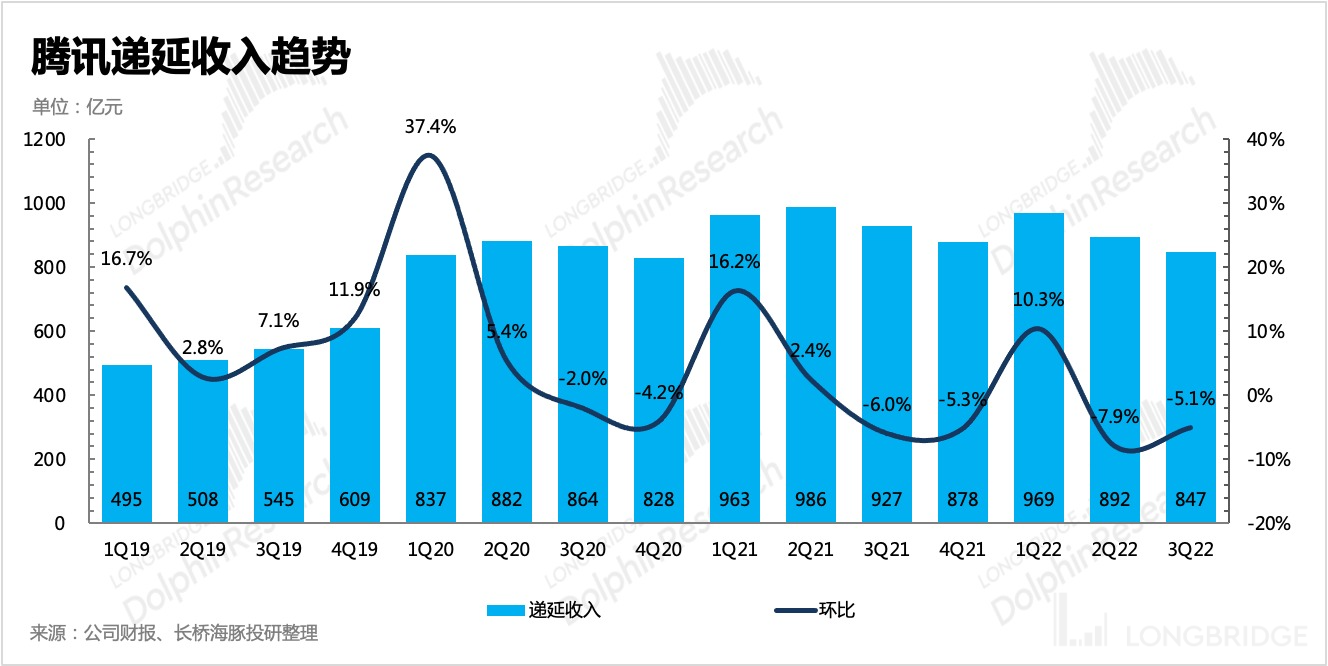

In the short-term, the headwinds in the game industry are still high-pressure. Tencent's deferred income and revenue are still declining month-on-month. Although the fourth quarter had no high base effect, the weakening of paid user demand for global games is also a fact. The pressure on game revenue will continue to spread to other businesses, especially the release of advertising revenue.

Advertisement: Warmth is Coming, essentially mining value in WeChat ecosystem.

Advertising revenue has once again significantly exceeded expectations. The stable Tencent-based ecosystem is the cornerstone of the recovery of commercialization of advertising. Although the third quarter emerged from the Shanghai epidemic, there were still many high-risk areas of the epidemic across the country. The overall advertising disclosed by CTR is still declining year-on-year. Most investment banks are relatively cautious, predicting a year-on-year decline of about 10%. However, Tencent's actual advertising only fell by less than 5%. Looking in-depth, social advertising has almost been flat compared to last year, but media advertising is still mired in an economic cycle quagmire.

This means that in the third quarter, social advertising dominated by WeChat began to exert force. In addition to the contribution of the newly added video ad, the possible action may also include releasing more advertising inventory in the WeChat ecosystem, alleviating the impact of eCPM pricing due to weakened demand by increasing advertising load rates. On the other hand, the low base effect of last year is also a factor in easing the decline.

Looking ahead to the fourth quarter, Dolphin Analyst expects this kind of major leap in recovery to continue. Next year, video advertisements will officially commence commercialization and the trend of Tencent's traffic being migrated externally may accelerate and even counterattack. Third-quarter reports show that the daily active users (DAU) of mini-programs have exceeded 600 million, an increase of 30% year-on-year. The average daily usage frequency has also increased by 50% year-on-year, indicating that the usage frequency of individual users is deepening. As the stickiness of the WeChat ecosystem increases, a complete traffic monetization plan can be applied and create value within the WeChat ecosystem.

Three

Gold and Cloud: Paying for Recovery, Cloud Business Transitioning "Pains"

In the third quarter, commercial payments quickly recovered as the Shanghai pandemic ended. During last quarter's conference call, management revealed that commercial payments had improved monthly, with a growth rate of over 15% in June. However, in the two months following the third quarter, various parts of the country have suffered pandemic rebounds, and offline activities in many cities were still affected. As a result, there has been some pressure. Looking at the reserve fund scale of payment institutions disclosed by the central bank, the year-on-year growth rate in the third quarter has slowed compared to the second quarter. Nonetheless, the financial report showed that commercial payment income, which accounts for nearly 70% of financial technology, still achieved double-digit growth.

Therefore, the overall growth rate of Gold and Cloud revenue was 3.5% year-on-year, mainly due to the drag on cloud business. Similar to last quarter, aside from the headwinds caused by the capital expenditure contraction of internet, entertainment-type consumers, the key factor affecting the contract scale is its own transformation towards "high-quality growth," primarily by reducing low-profit margin bespoke and subcontracting contracts while turning to SaaS, PaaS services with higher profitability.

Looking ahead to the fourth quarter, Dolphin Analyst expects payment businesses to continue to recover and grow strongly, along with the transitional pain of cloud business reflecting on performance, but is optimistic about the possibility of recovery and growth next year as offline activities resume and the economic outlook improves.

Four

Digital Content: Continuously Optimizing the Profit Model during the Headwind Period

The digital content business, which is mainly composed of music, online literature, and long video subscription income, is an optional consumer service. During the economic downturn, purchasing power has significantly weakened. Combined with Tencent Music's financial report yesterday, the main pressure on income is still the decline in paying users, especially facing traditional live broadcasting business competition in a poor environment.

However, since the beginning of the year, the strategic plan of the digital content sector has been in a contraction phase. Both Tencent Video and Tencent Music have reduced or cautiously invested in low-return projects, slowed expense spending for acquiring customers, and turned to mining the pay potential (i.e., ARPPU) of existing core users to optimize the previously dismal profit model. Looking ahead at the short- to medium-term future, Dolphin Analyst expects that the improvement in profits from digital content will continue to contribute to the overall profitability of the group, while a new expansion period will need to wait for a significant improvement in the economy.

V.

Investment income: Executive exits Sea's board, asset reclassification leads to profit and loss confirmation

The net amount of other income in the third quarter was abnormally high due to the significant increase in investment company disposal income, mainly due to Ren Yuxin's exit from Sea's board, which resulted in Sea being reclassified from a Tencent associated company to a financial asset, resulting in deemed disposal gains.

Tencent has always adopted a cautious and conservative accounting treatment for its large-scale investment assets. For large-scale investments in listed companies with a high shareholding percentage, Tencent mainly classifies them as associated company assets, only recognizing the profits of the invested company calculated according to the shareholding percentage (included in the shared company income), but the profit and loss brought about by stock price fluctuations is not included in the current quarter's profits and losses, and only disposals or deemed disposals will be recognized.

Therefore, JD and Sea, which reduced their holdings at the beginning of the year, both confirmed disposal gains for the quarter, and today's announced clearance-style reduction of holdings by Meituan will also be reclassified from associated company assets to financial assets measured at fair value, and disposal gains are expected to be recognized in the dividend-paying quarter (i.e., the third case in the table below).

VI.

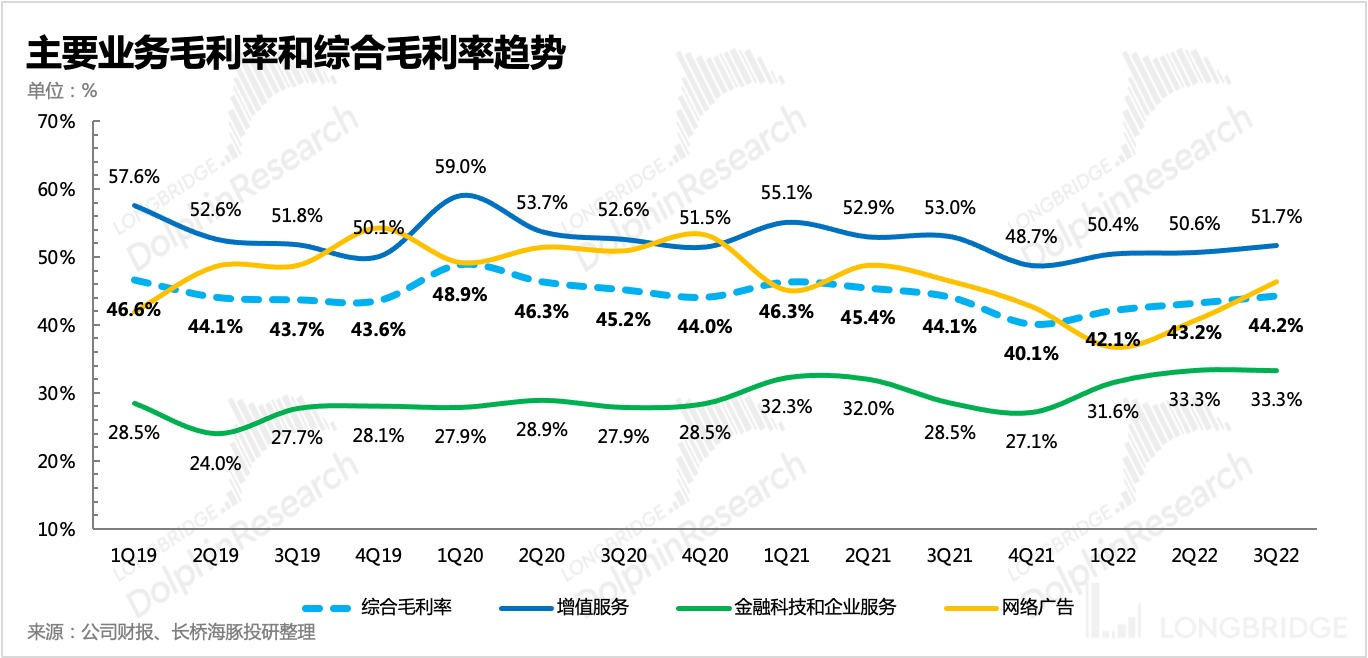

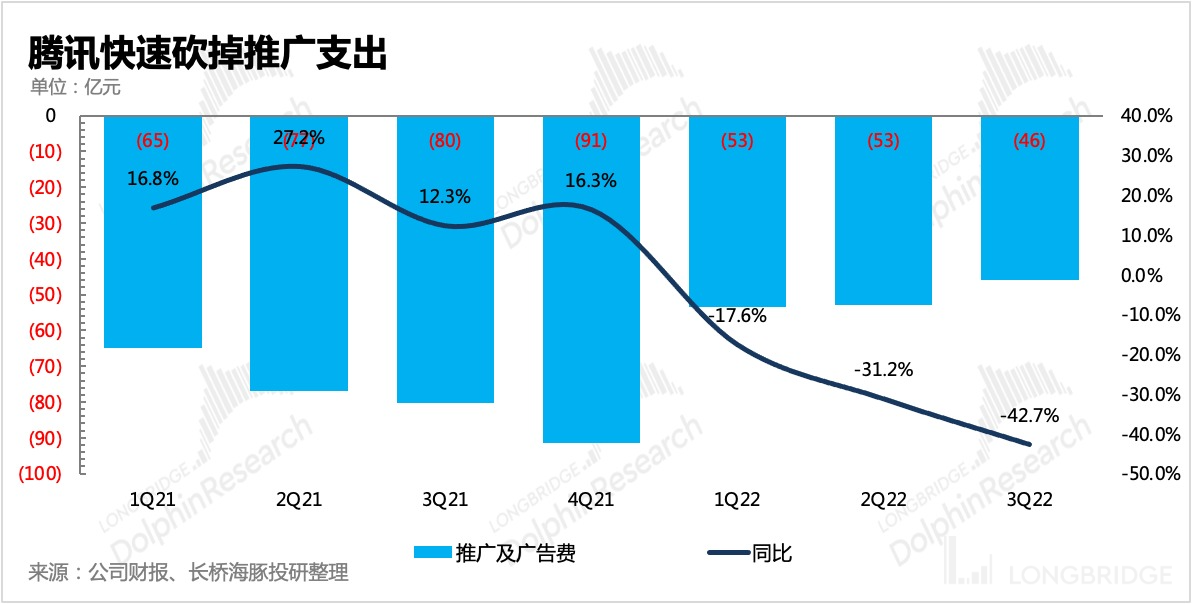

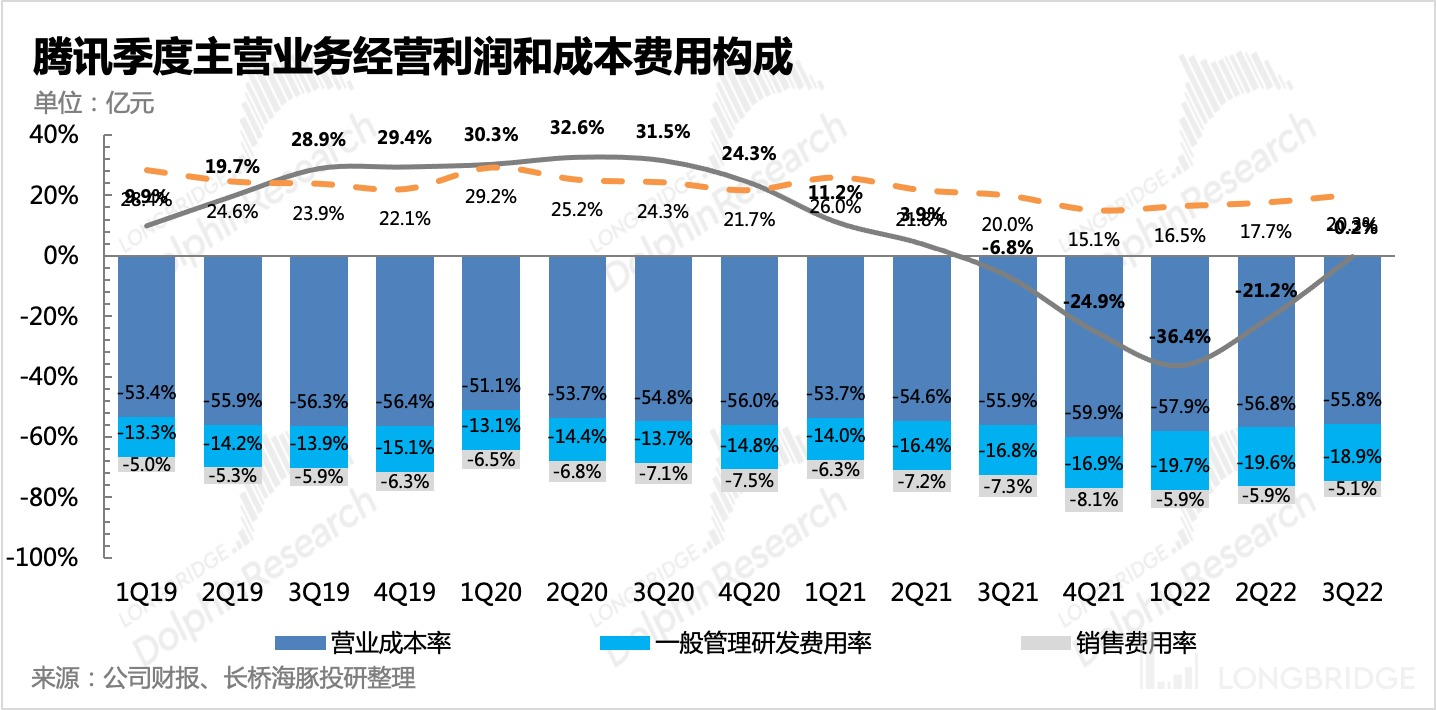

Profits: Advertising drives gross margin, promotion expenses continue to be significantly reduced

Finally, let's look at the profit situation. In the third quarter, Tencent's core operating profit, which represents the main business operations, has basically contained the downward trend, rebounding rapidly from the first and second quarters. This is mainly reflected in the fact that the gross profit margins of the three major main industries have all increased compared to the previous quarter, especially the gross profit margin of the advertising business, which has been significantly improved after the accelerated monetization of video accounts and further release of WeChat's ecological advertising inventory. Updated Progress of Share Repurchase and Reduction

Due to the significant impact of major shareholder reduction on Tencent's short-term share price performance, Dolphin Analyst believes it is necessary to update the current situation of reduction and Tencent's repurchase actions during the same period.

From June 28 to October 14, Tencent has repurchased more than 60 million shares, with a total of over HKD 18 billion used, after the sensitive period of financial reporting. Tencent may continue its repurchase actions.

From June 28 to September 2, the major shareholders reduced 76 million shares of Tencent's stocks and stopped reducing thereafter, but they are still continuously repurchasing their own stocks. Currently, the NAV and stock price discount rate of the major shareholders have narrowed.

Dolphin Analyst Tencent Holdings-related Articles:

Financial report season (last year)

August 18, 2022 Telephone Meeting: "Decreasing costs and increasing efficiency will continue in the second half of the year, and "video numbers" are highly anticipated (Tencent 2Q22 Telephone Meeting Summary)"

August 17, 2022 Financial report review: "360 degrees without blind spots disassembling Tencent: Is it really that bad?"

May 18, 2022 Telephone Meeting: "This year's growth guidance depends on the epidemic situation (Tencent Telephone Meeting)"

May 18, 2022 Financial report review: "Tencent: The King of Stocks is still crossing the robbery"

March 23, 2022 Telephone Meeting: "Under the industry's slowdown, high-quality and healthy growth comes first (Tencent Telephone Meeting Summary)"

March 23, 2022 Financial report review: "Tencent: The Stock King is still "squatting"? The moment of testing faith has arrived"

Depth

September 28, 2022: "Returning to Tencent and exploring the "bottom" of the King of Stocks (Dolphin)"

January 5, 2022: "Did the fear of "little Tencent" scare Tencent's younger brothers? Sea's significance is different"

June 28, 2021: "Behind the "chicken ribs" Tencent: After all, it still targets payment! | Dolphin investment research"

June 20, 2021: "Tencent's next stop: trillion-dollar market value? (Part 2)|Dolphin Investment Research" On June 10, 2021, Tencent's Next Stop: A Trillion-Dollar Market Cap? was released.

On May 19, 2021, Tencent faced enormous pressure before regulatory landing, can it withstand the pressure? | Giant's Foresight was published.

On May 5, 2021, the flow property rights war: merchants enter the game and Tencent triumphs | Research Summary was released.

Hot Topics

On January 17, 2022, the butterfly effect of Ant Group: Will Tencent leave Meituan and Pinduoduo behind? was released.

On January 12, 2022, a discussion was made on the other "Half-Life" value of Tencent that had been transferred.

On December 23, 2021, Tencent "Goodbye" JD: happy breakup or painful surgery? was published.

On December 14, 2021, the stock price of Tencent may have hit bottom as regulatory turning point approaches.

Live Streaming Events

On August 17, 2022, Tencent Holdings (00700.HK) 2022 Q2 earnings conference call.

On May 18, 2022, Tencent Holdings (00700.HK) 2022 Q1 earnings release.

On March 23, 2022, Tencent Holdings (00700.HK) 2021 Q4 and annual earnings release.

On November 10, 2021, Tencent Holdings (00700.HK) 2021 Q3 earnings release. August 18, 2021 "Tencent Holdings (00700.HK) Q2 2021 Earnings Call"

May 20, 2021 "Tencent Holdings (00700.HK) Q1 2021 Earnings Call"

Disclosure and statement of risks: Dolphin Analyst disclaimer and general disclosure