Hong Kong and A share price-performance ratios have swapped, how far away is the "danger" and "crisis" turnaround in US stocks?

Hello everyone, I am Dolphin Analyst and the weekly market portfolio strategy is here again. The key information is as follows:

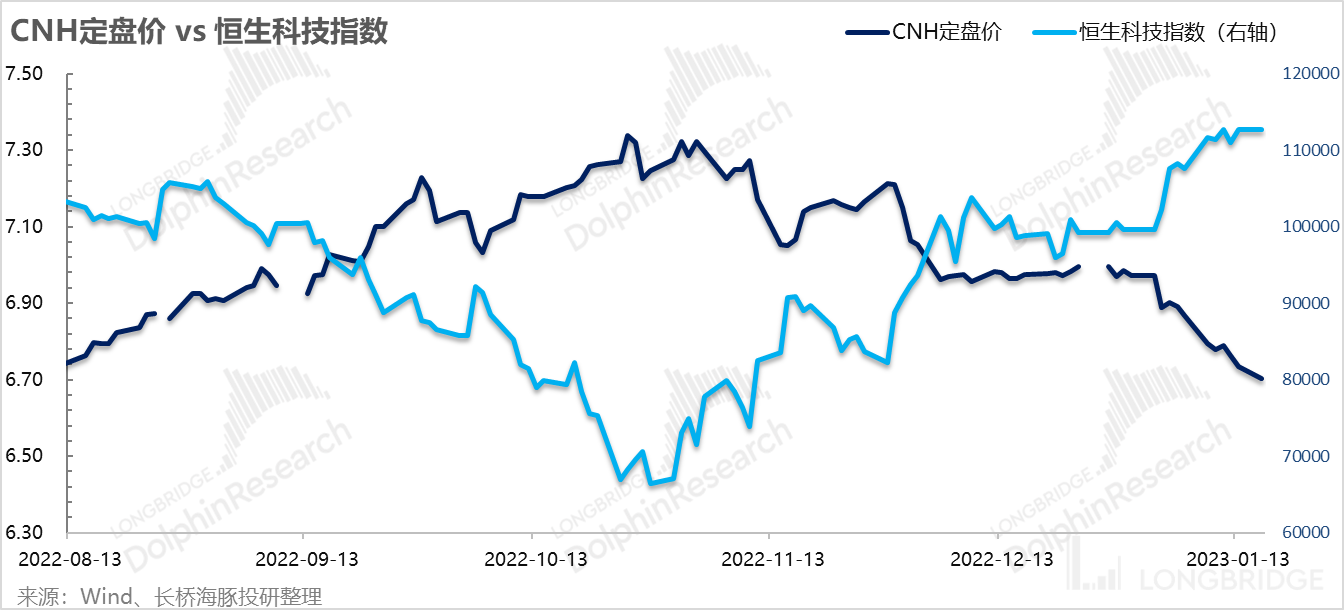

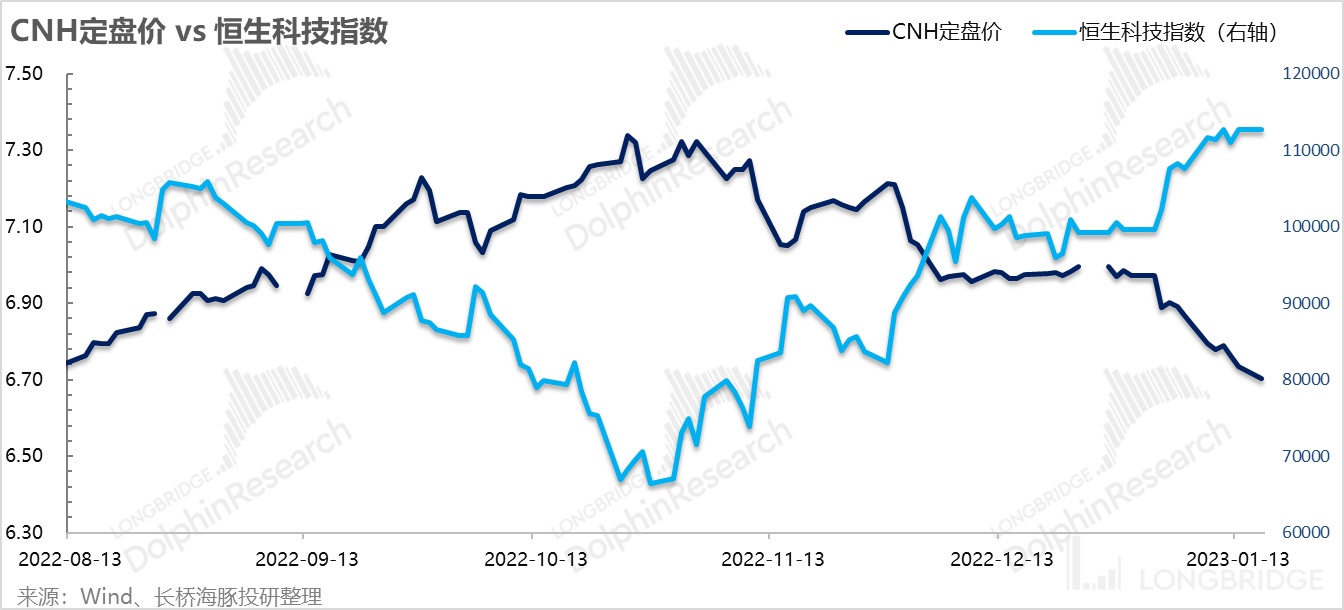

1) As mentioned in the report of the Dolphin Analyst last week, even though the RMB is still appreciating, the space for further increase is gradually limited as the Hong Kong stock valuation has exceeded historical average by over 50%. Meanwhile, as RMB continues to appreciate, the attractiveness of Chinese assets is still there, and foreign capital is beginning to shift their focus to A-share market leaders and blue-chip stocks which still offer value for money.

2) Regarding Hong Kong stocks, the Dolphin Analyst maintains the judgment of last week: as the valuation repair gradually comes to an end, attention needs to be paid to the risk of a pullback in previously trendy small-cap stocks when the performance is needed to support further stock price growth.

3) As for the US stock market, the Dolphin Analyst's views are beginning to change gradually: the marginal easing of human service-type prices in CPI + service PMI + wages may gradually soften the Fed's rigid attitude, and the high-interest rate residence may not last long + the arrival of interest rate cut expectations may mean that the US stock market opportunities may be gradually approaching after the earnings season and the end of the rate hike, for example, it may be worth preemptively targeting some undervalued stocks that are sensitive to interest rate changes but have a relatively stable industry position, such as Qualcomm among semiconductor stocks and Amazon among software technology. The Dolphin Analyst will make some timely adjustments this week, selling HSTECH ETF and adding some semiconductor leaders to the portfolio.

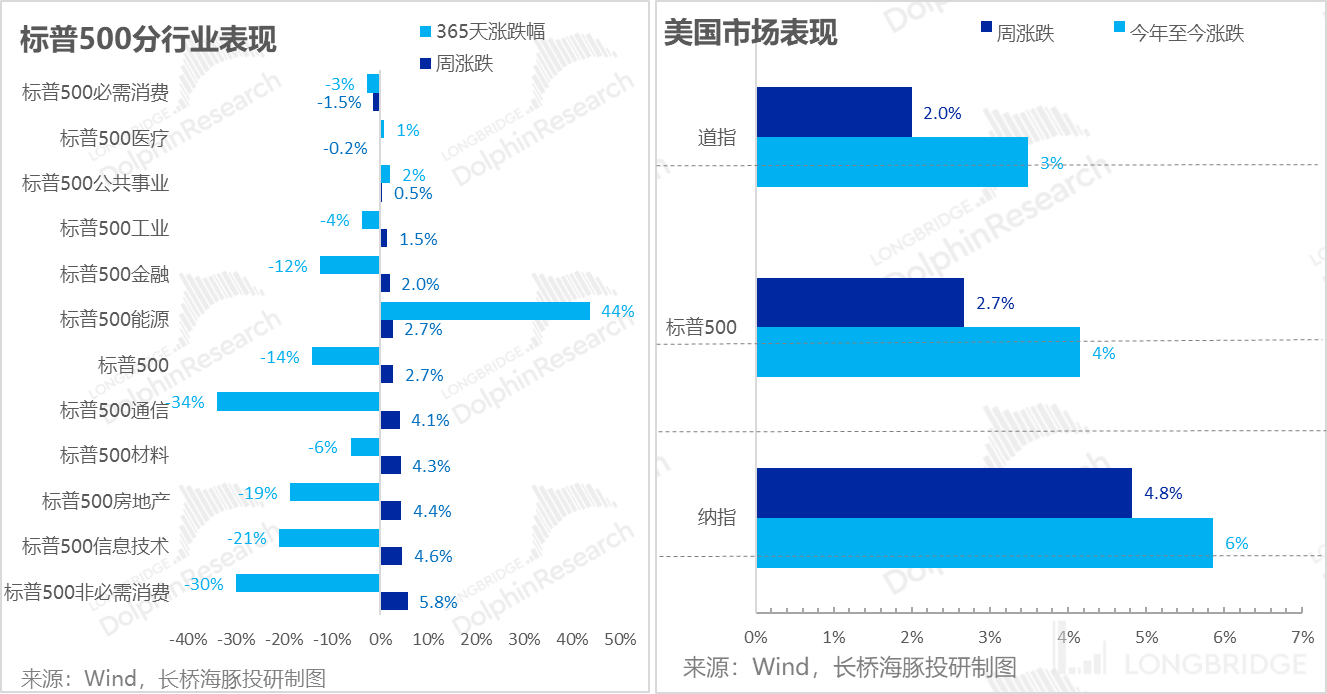

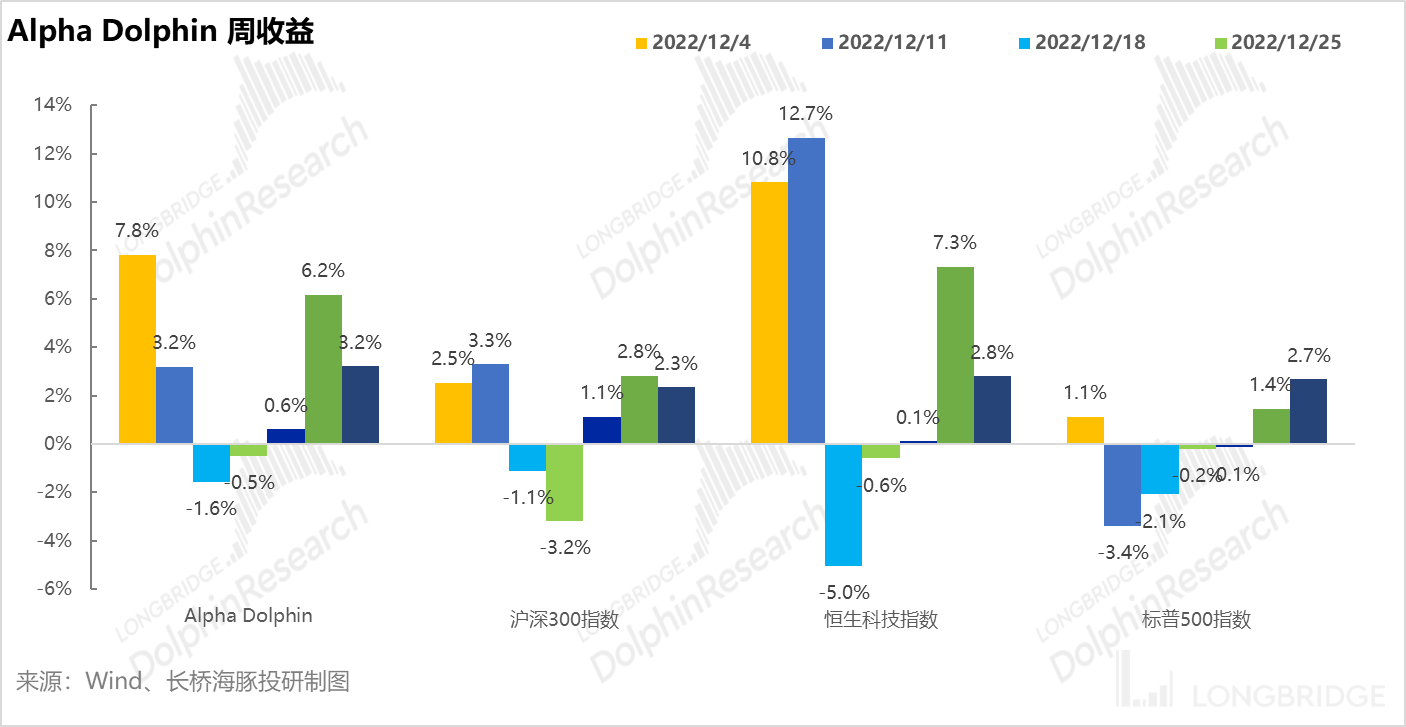

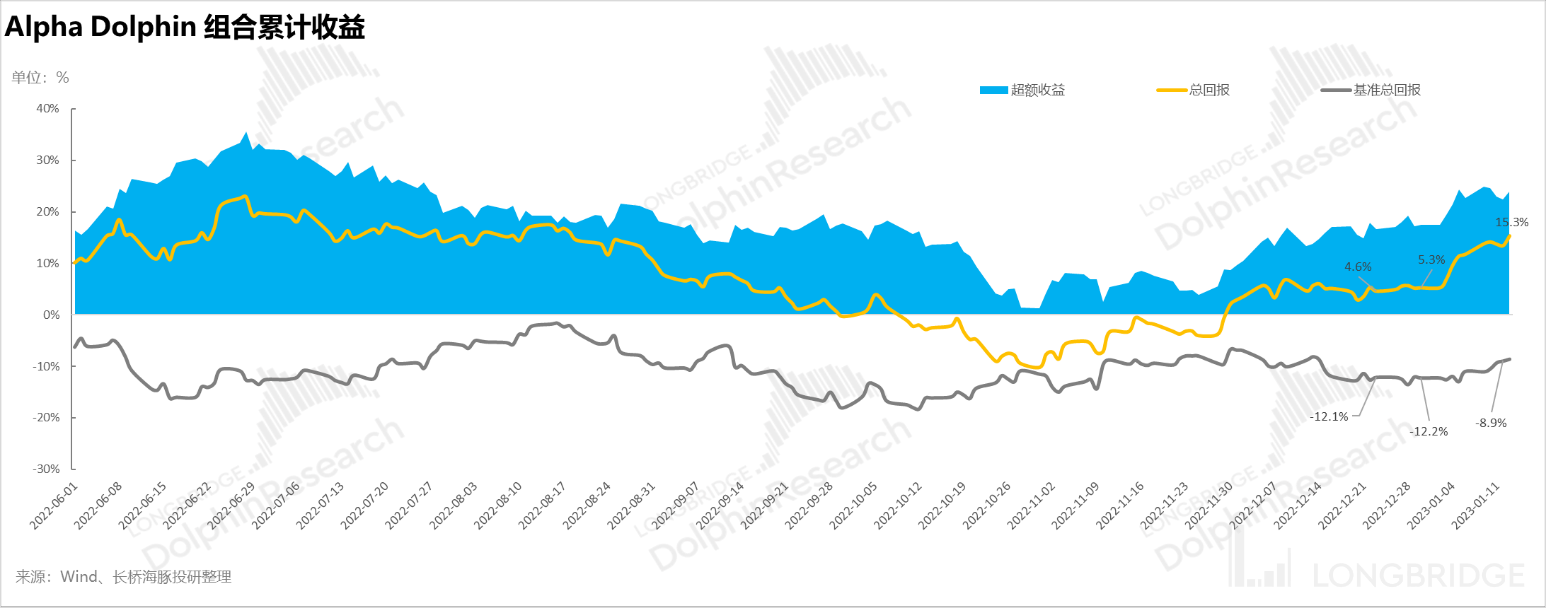

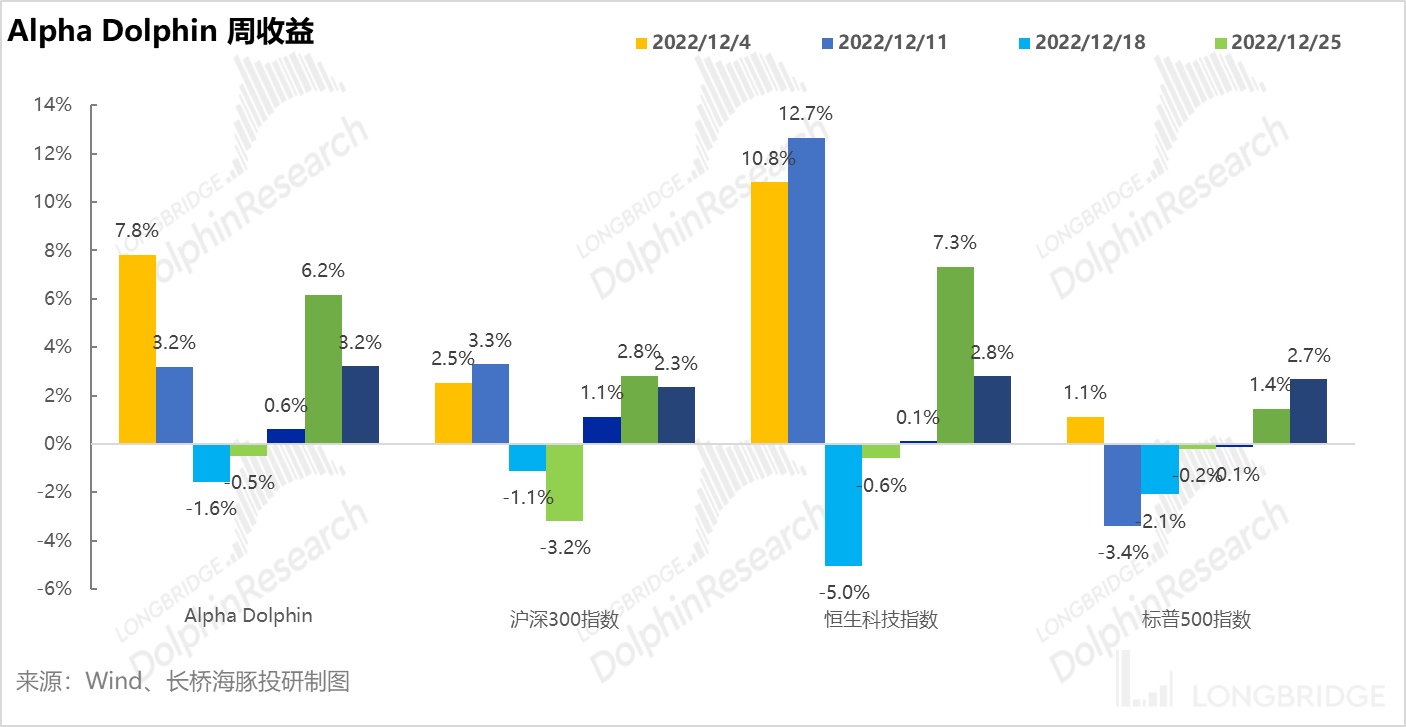

4) After Alpha Dolphin Portfolio suggested investing in Didi, they increased their holdings in Didi last week. Portfolio returns last week continue to outperform the benchmark index: Alpha Dolphin's virtual portfolio was up 3.2% (with equity up 3.6%), which was obviously better than the Shanghai and Shenzhen 300 (+2.3%), the S&P 500 (+2.7%), and the HS Technology Index (+2.8%).

Here are the details:

I. The driving force behind recession expectations: Is the US Service Sector Cooling Down?

Last week, the US CPI met market expectations as if by divine intervention, causing the CPI and CPI sub-items almost entirely consistent with market expectations, with zero expectation deviation, leaving the market clueless.

In fact, with regard to CPI data, the Dolphin Analyst believes that in situations where the trend is certain, only the marginal increment needs to be considered. In the core CPI, most of the sub-items, such as goods, cars, and housing prices, were already at a high level before, and their trend was downward almost certainty under the current interest rate level, without need for too much attention to monthly fluctuations.

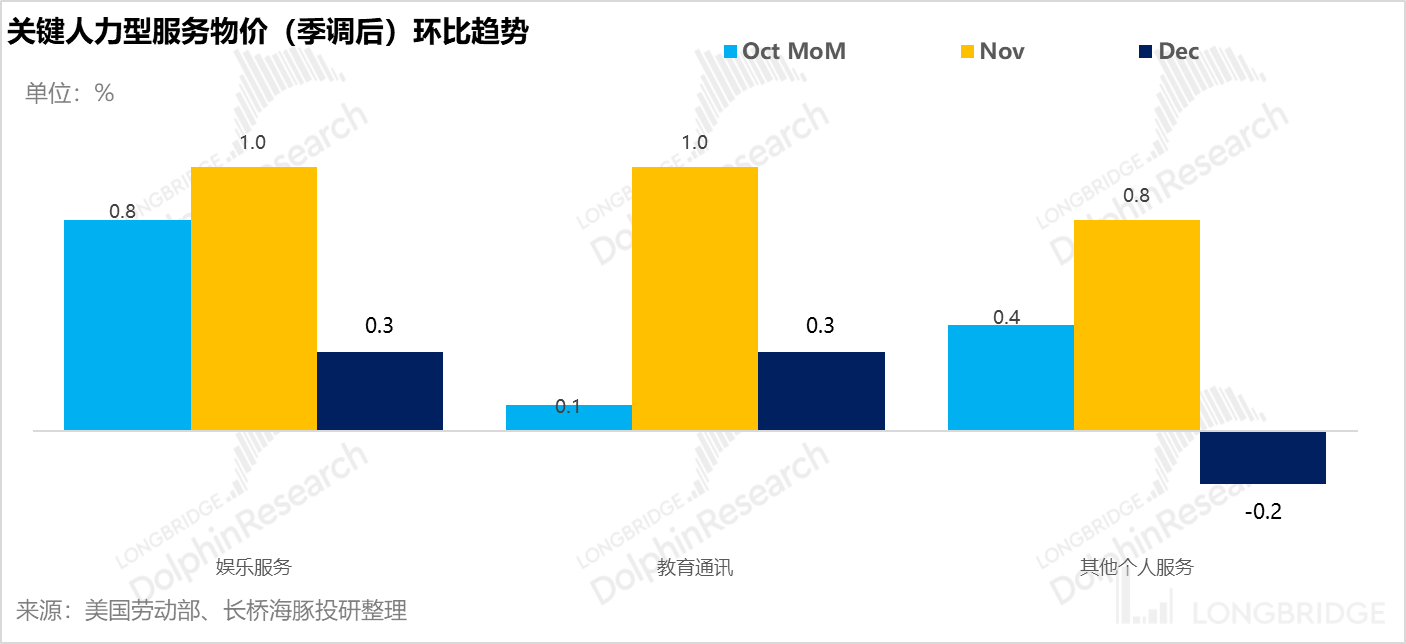

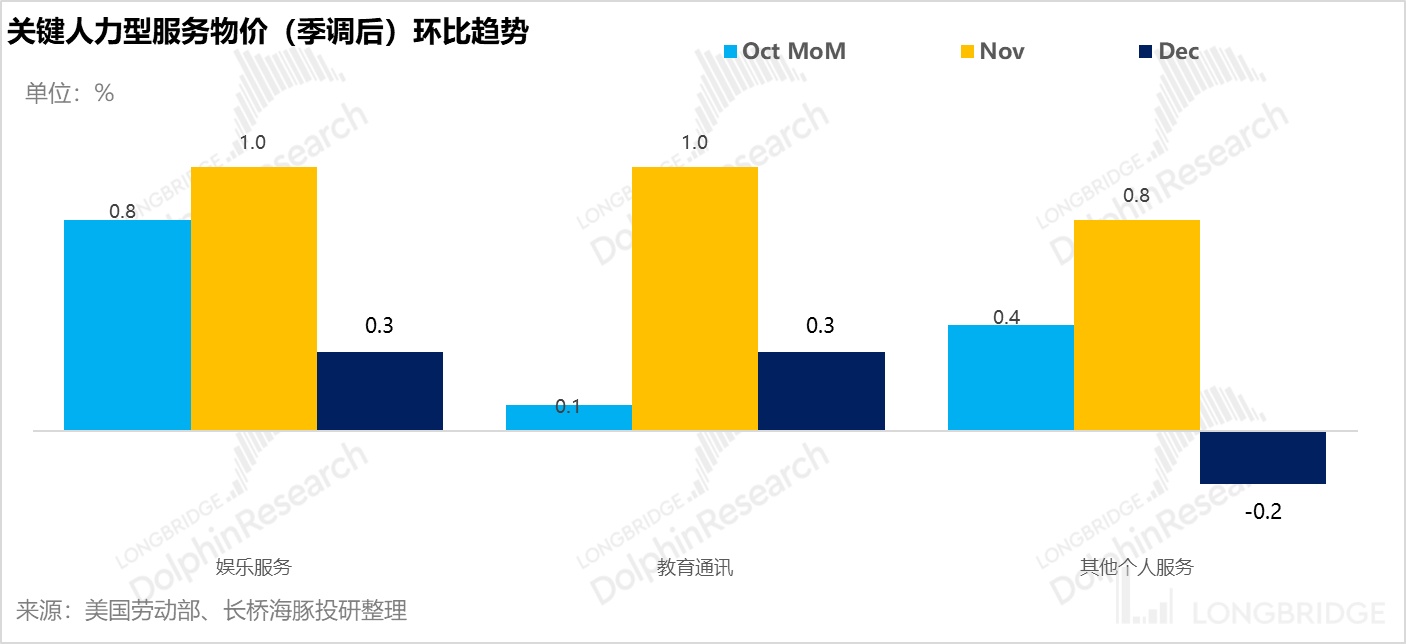

For CPI, the Dolphin Analyst truly focuses on the three subdivided items of CPI that are highly correlated with personnel cost investment factors-education communication, entertainment services, and other personal services (1.37%). Among them,

a) Education and Communication have a weight of 5.32% in CPI and are also the third largest service item in the EX-Housing Services CPI, apart from medical and transportation services. It is mainly related to various renewals from daycare, vocational education to university, and communication mainly includes postal and courier services and telephone conferences, internet and related services.

b) Entertainment Services account for 3.15% of the CPI, including specific projects such as video and music memberships, pets, photography, movie and sports event tickets, and personal training fees, among others.

c) Other Personal Services include personal care such as haircuts, legal services, funerals, laundry, finance and other miscellaneous services, with a CPI weight of 1.37%.

As shown in the figure below, the prices of these items skyrocketed in October and November, especially in November, with month-to-month increases ranging from 0.8% to 1%.

However, in December, the month-to-month growth of these three seasonally adjusted items has shown a slowing trend, with other personal services directly experiencing negative growth. All three data points indicate a rapid marginal decline in labor-intensive service prices.

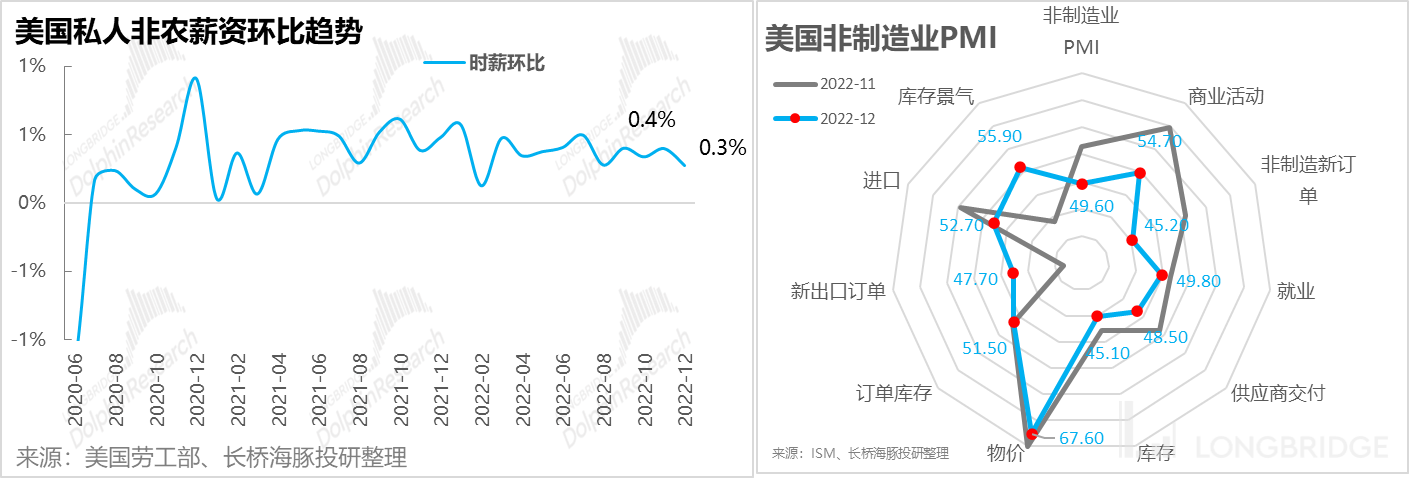

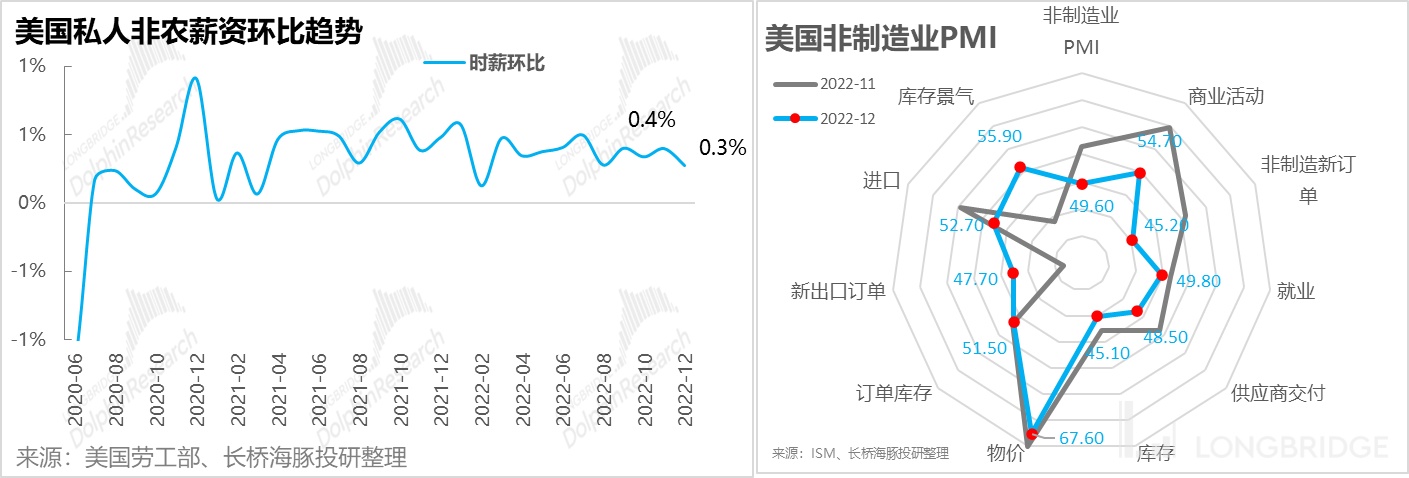

If we put this chart together with the two charts related to services that I shared earlier for comparison, it means that the two lagging indicators - service prices and non-farm wages - are both slowing on a month-to-month basis, while the forward-looking indicator - the non-manufacturing PMI - is rapidly declining into the contraction zone, implying a collapse in service consumption later.

At present, the core problem that troubles the high rate of interest rate hikes is that other price indicators related to manpower and the business climate of the service industry have fallen.

Therefore, with at most one more month's data to verify, the general result is that the dust has settled on the Fed's higher interest rate, and the rate path will either end with a 25 basis point hike in February or 25 basis points increase again in March, with the peak of this rate hike ranging from 4.75% to 5%.

As such, what funds should be thinking about next is when the rate cut expectations will come and the depth of this recession, corresponding to two scenarios:

1. Interest Rate Cuts + Mild Decline: Moving from expected interest rate hikes to expected interest rate cuts, the undervalued U.S. stock market will welcome an opportunity for easy money-making by undergoing a wave of valuation repairs. Following that, the recession's impact will be rather mild, and relatively lower-risk assets should be chosen, such as those that are first into and first out of recession, those with strong industry positions, and those with unaffected competition patterns, such as the Dolphin-covered Amazon, as well as Qualcomm and TSMC.**

2. Interest Rate Cuts + Deep Decline: In this scenario, after the valuation repairs, most stocks' EPS will deteriorate, and their performance will plummet. After the short-term valuation repair brought about by the interest rate cuts, when considering that the Fed is unlikely to release unlimited stimulus measures like it did in 2020, when the EPS collapses, share prices will still turn down even after repair. For these two scenarios, given the current trend of short-term structural labor demand, the probability of deep recession is small. Based on this financial report season, most companies are expected to have a mediocre performance in terms of both current and future results.

It might be a good idea to focus on the stock price drops during this financial season in the US market, and then invest in some undervalued stocks with good cost-effectiveness of overshooting, in tandem with the changes in macro data and the expectation of interest rate hikes.

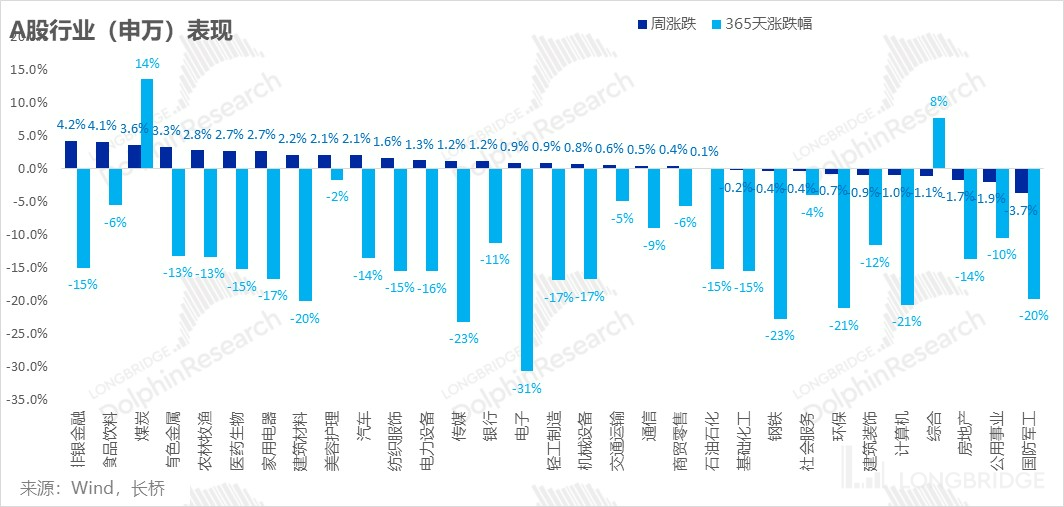

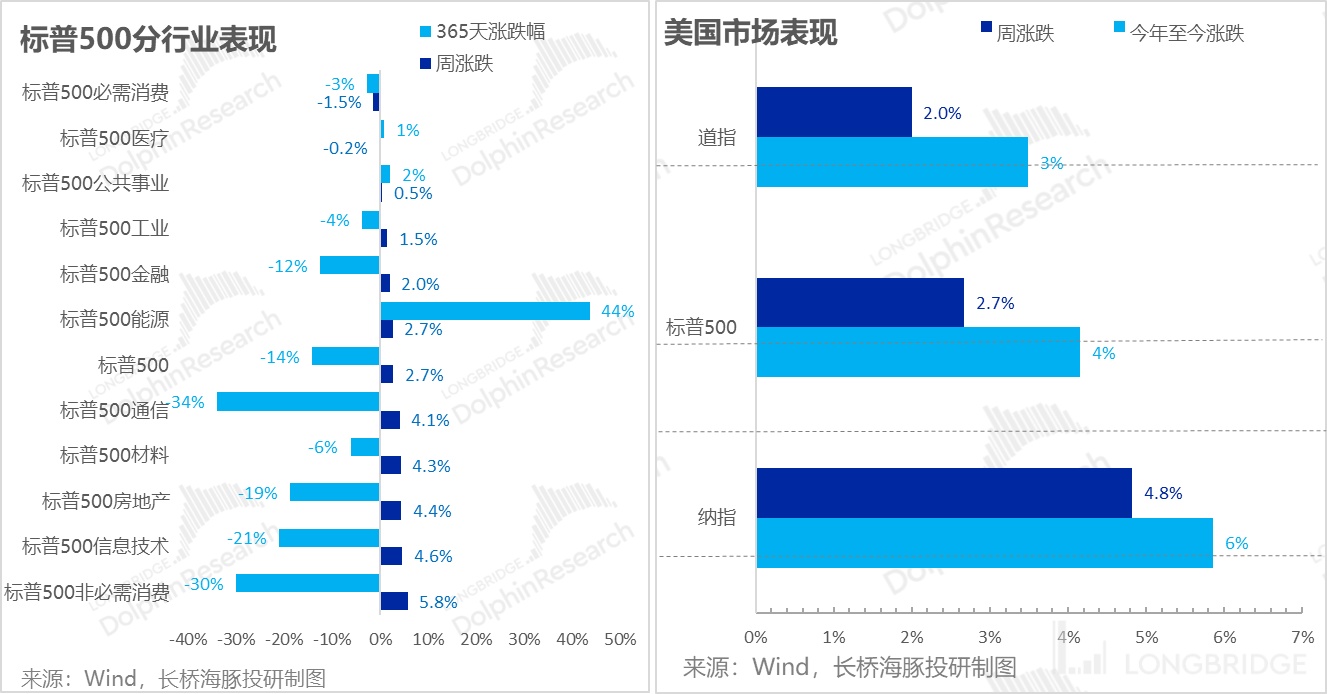

As for the market performance, the US market has now seen two consecutive weeks of valuation correction style: the growth-oriented NASDAQ outperformed the traditional industry-dominated Dow, while for the S&P 500 sector, the tech and discretionary sectors that experienced greater pullback and sensitivity to trends prevail.

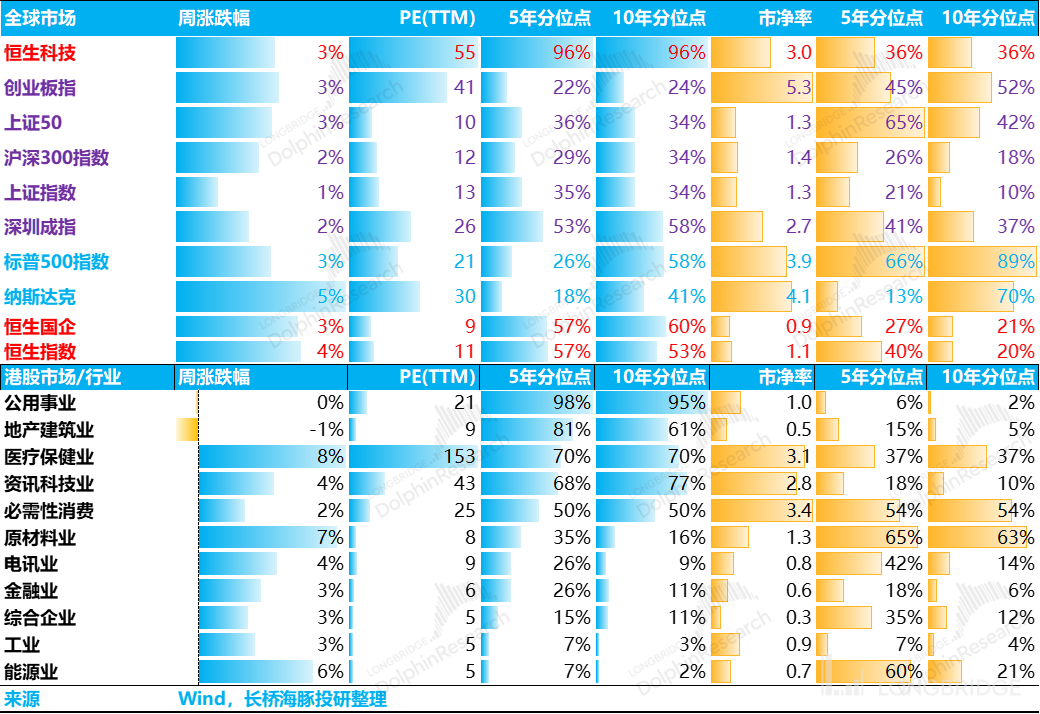

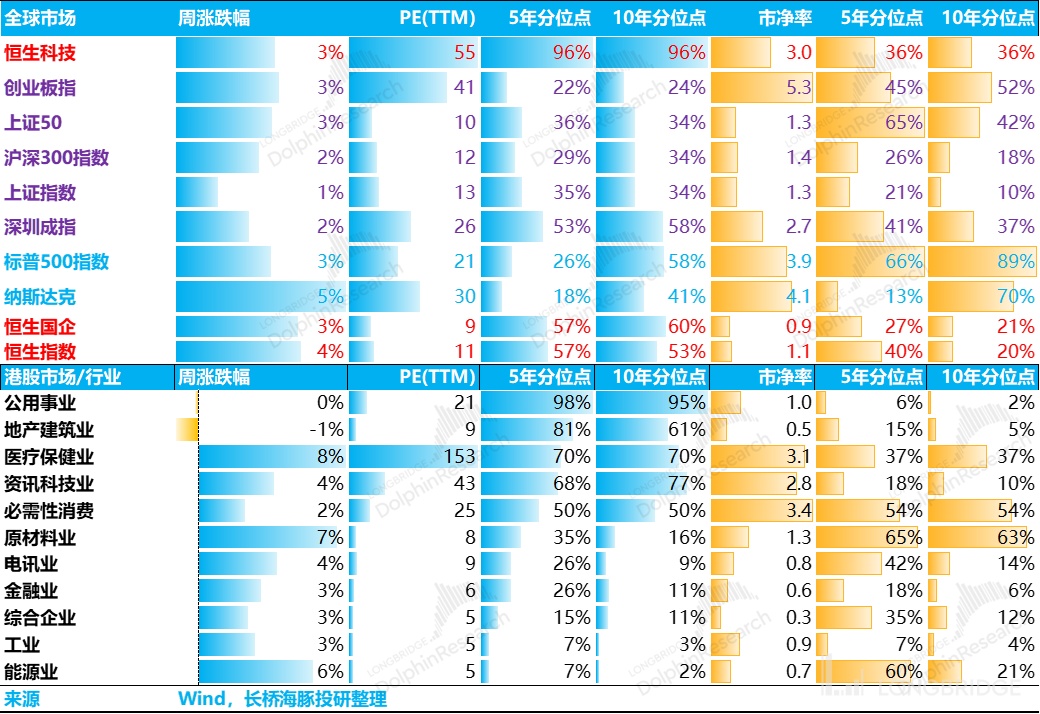

Secondly, there are fewer and fewer undervalued stocks in the Hong Kong stock market, and the upward trend still need to wait for better-than-expected economic recovery.

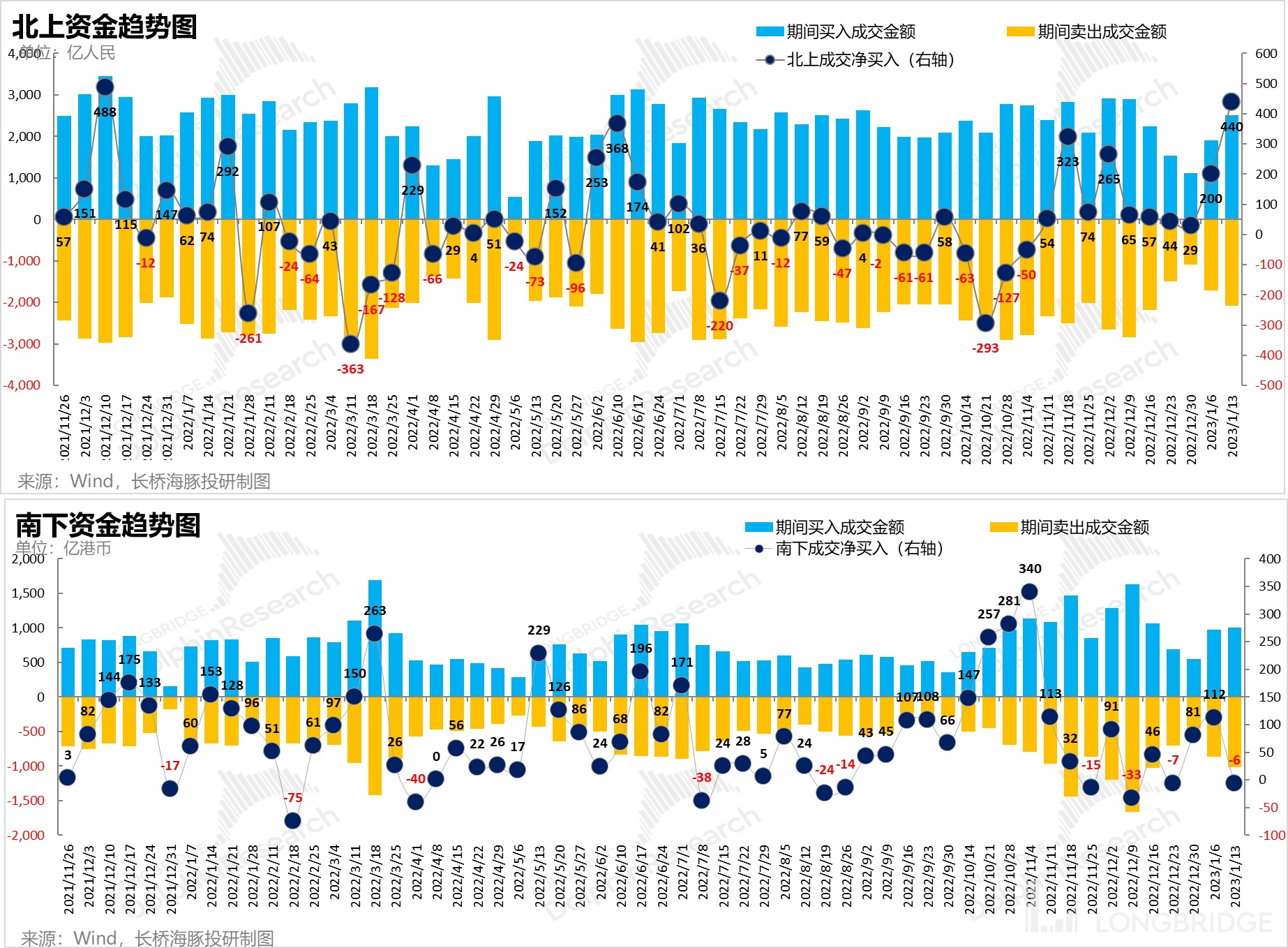

After Dolphin Analyst mentioned that the Hong Kong SAR's valuation correction had approached its historical average and opportunity was becoming limited, it was clear in these past two days that even if the RMB further appreciated, Hong Kong stocks have become sluggish and did not continue to rise rapidly with the sharp appreciation of the RMB.

At present, undervalued sectors in the Hong Kong stock market have become scarcer by sector. In terms of the five-year valuation percentile, cost-effectiveness is worse than A-shares, especially for leading and blue-chip stocks in the A-share market, which is reflected in the higher cost-effectiveness of the current CSI 50 and Shanghai-Shenzhen 300 indexes than that of Hong Kong stocks.

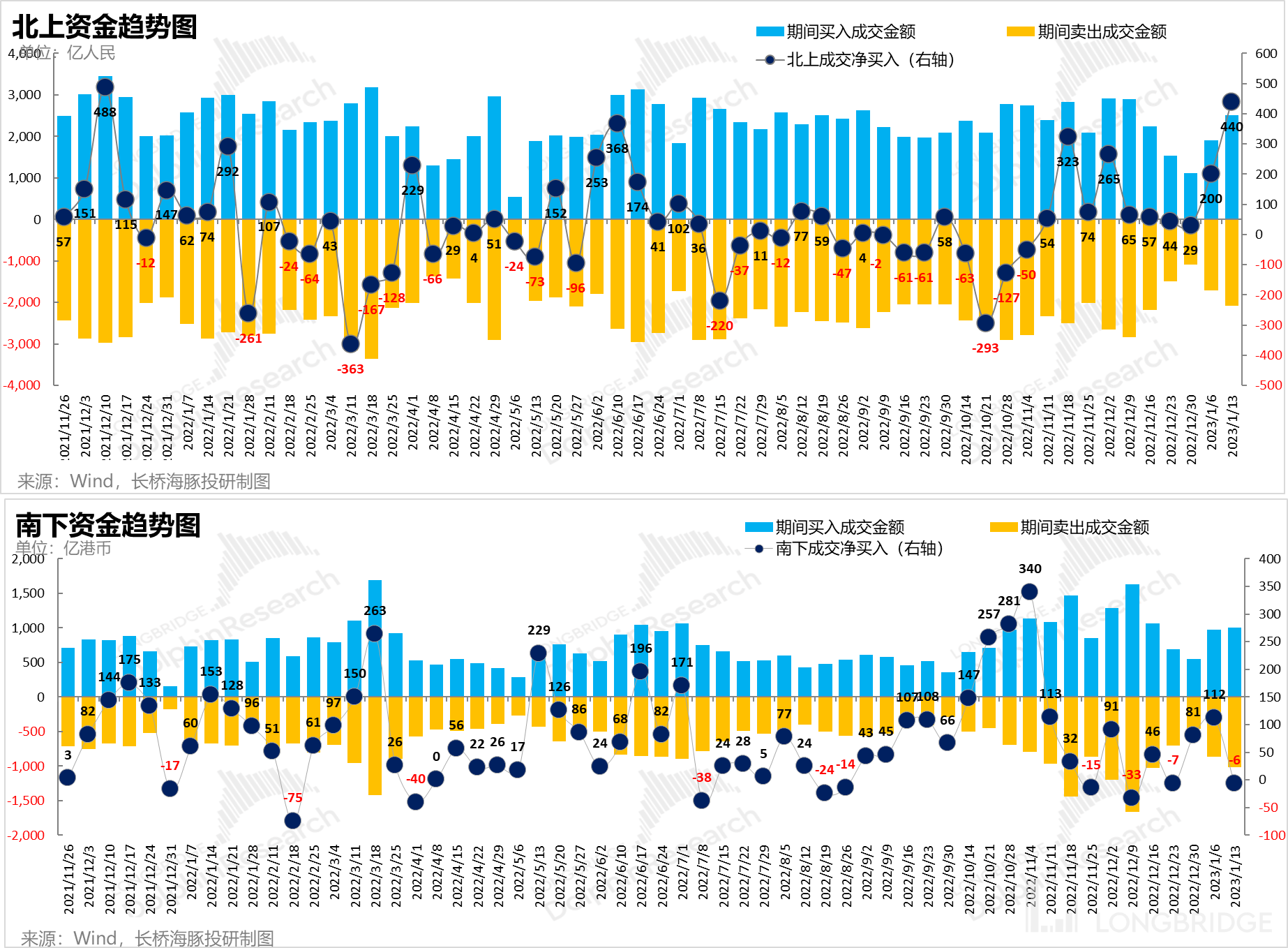

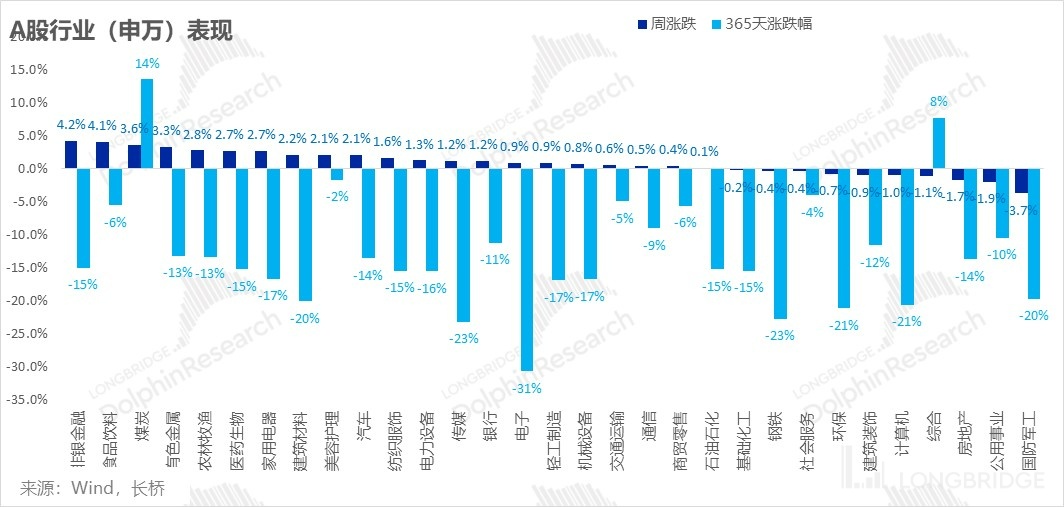

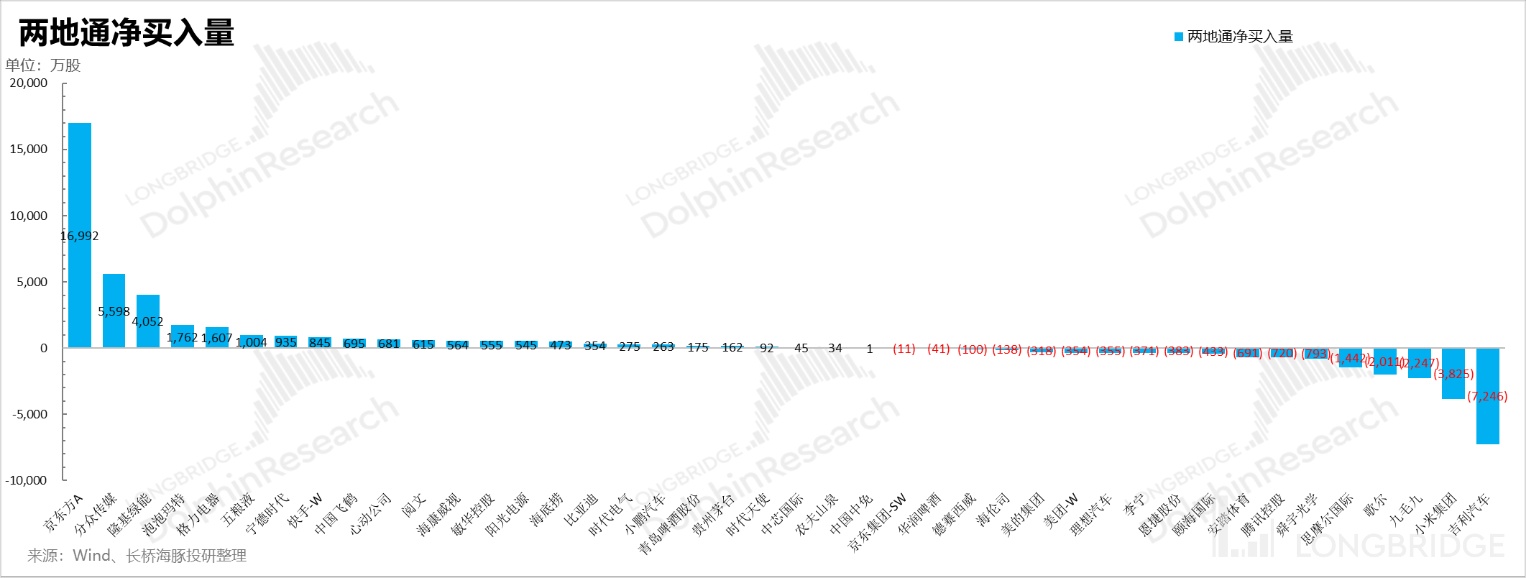

Obviously, as the RMB still continues to appreciate and the valuation of offshore Chinese assets has exceeded the five-year average, foreign capital has begun to flow into some relatively undervalued onshore Chinese assets. As a result, leading and blue-chip A-shares, such as undervalued financial and food and beverage stocks, have been gaining momentum and last week's northbound flows hit a new high for the year. Southbound funds have turned to net outflow due to the deterioration of cost-effectiveness in the Hong Kong stock market.

Overall, with regards to Hong Kong stocks, the Dolphin Analyst maintains his previous viewpoint: the risks of small-cap stocks with poor fundamentals and no industry status that previously rose sharply due to valuation recovery and then fell back are relatively high.

Overall, with regards to Hong Kong stocks, the Dolphin Analyst maintains his previous viewpoint: the risks of small-cap stocks with poor fundamentals and no industry status that previously rose sharply due to valuation recovery and then fell back are relatively high.

From the perspective of the five-year valuation percentile, the currently undervalued market is actually Nasdaq. As the market shifts from expected interest rate hikes to expected interest rate cuts, and with the US stock market tending to lightly step into recession, the Dolphin Analyst believes that after the completion of the earnings season thunderstorm, attention can also be paid to the US stock market.

3. Alpha Dolphin Portfolio Returns

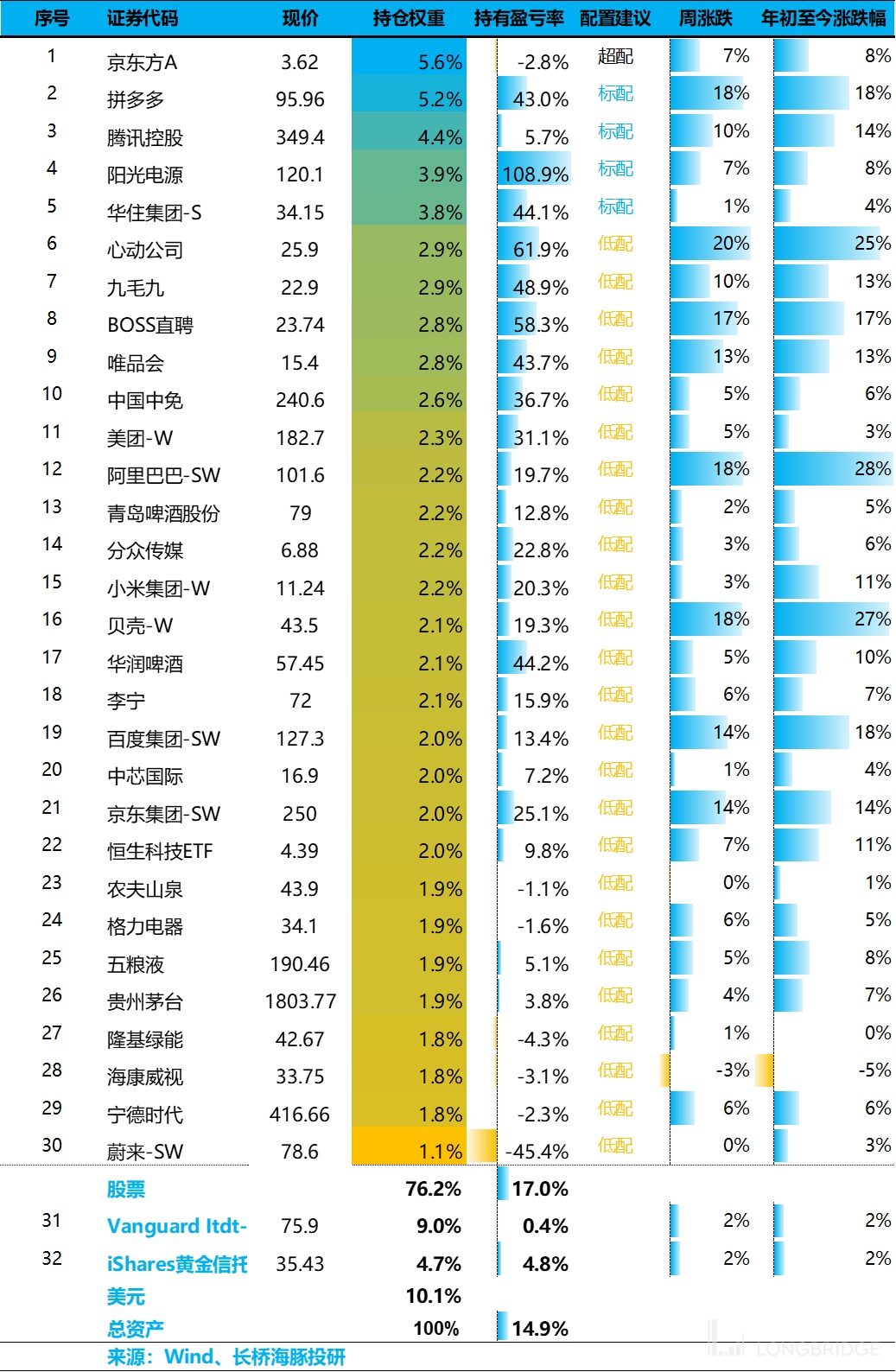

Last week, the Dolphin Analyst made only minor adjustments to the portfolio, based on Didi's industry status being unperturbed (see details here) and expectations of relaxed regulation, and shifted Didi from observation allocation to low allocation.

Alpha Dolphin portfolio went up 3.2% this week (where equity rose by 3.6%), clearly surpassing the Shanghai and Shenzhen 300 (+2.3%), outperforming the S&P 500 (+2.7%) and outperforming the Hang Seng technology index (+2.8%).

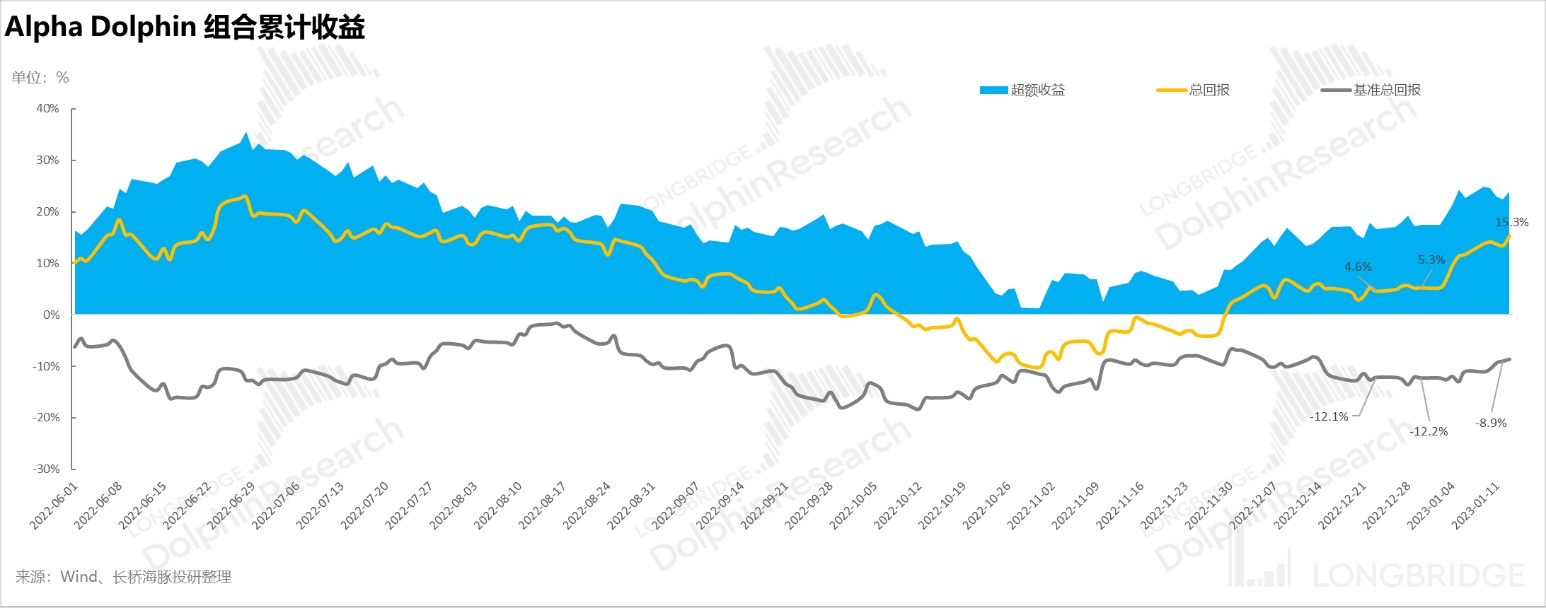

Since the start of the portfolio test until the end of last week, the portfolio's absolute return was 15.3%, and its excess return compared to the benchmark S&P 500 index was 24%.

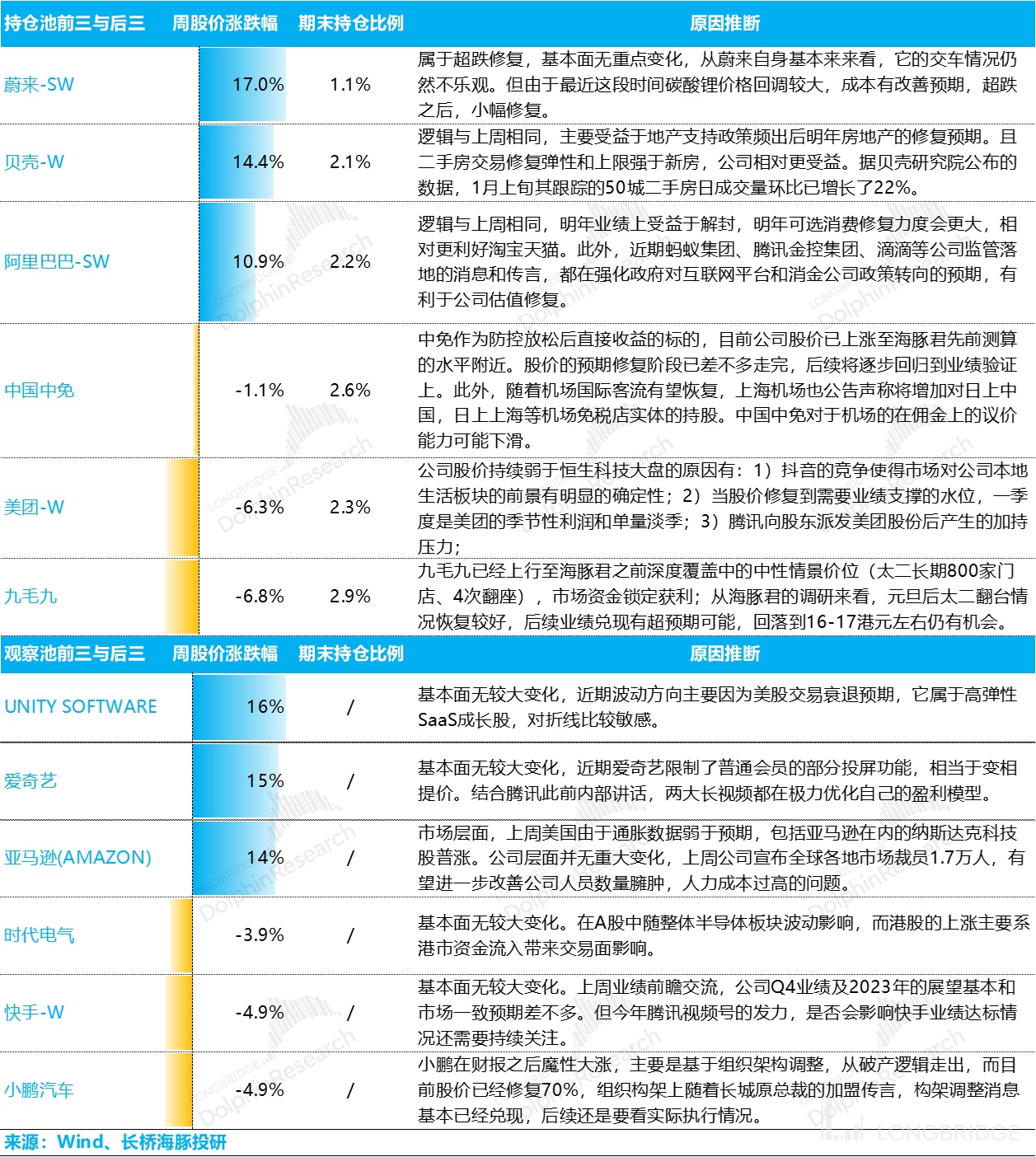

5. Individual stock performance: undervalued Chinese stocks still rising, while others show strong gains without falling back

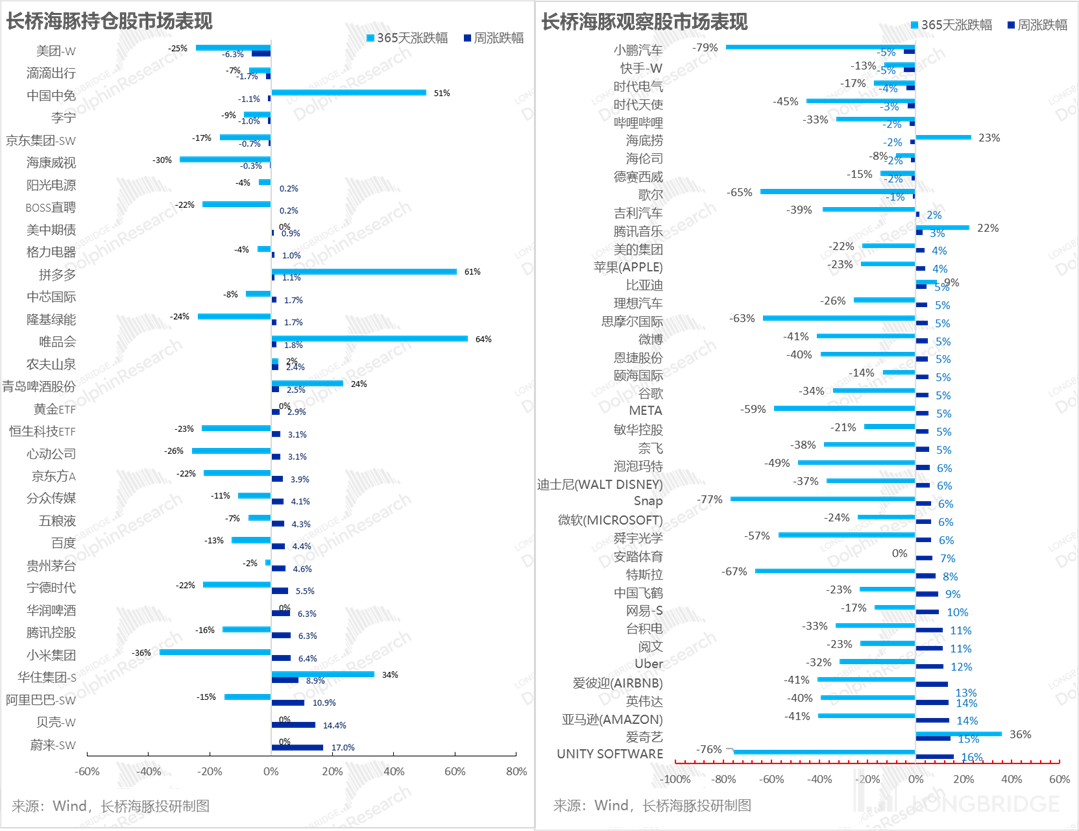

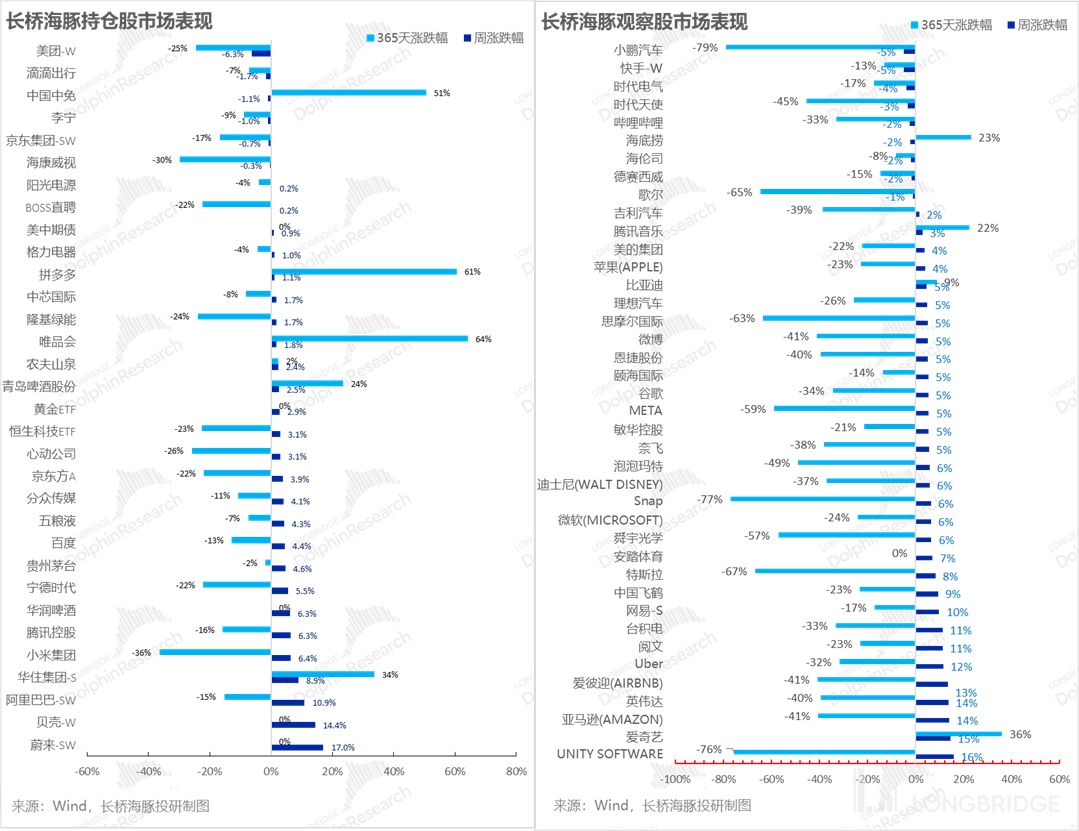

The reason why the Alpha Dolphin Portfolio outperformed the benchmark portfolio last week can be summarized as a push from the undervalued Chinese stocks, while other companies within the allocation pool basically did not fall back after rising.

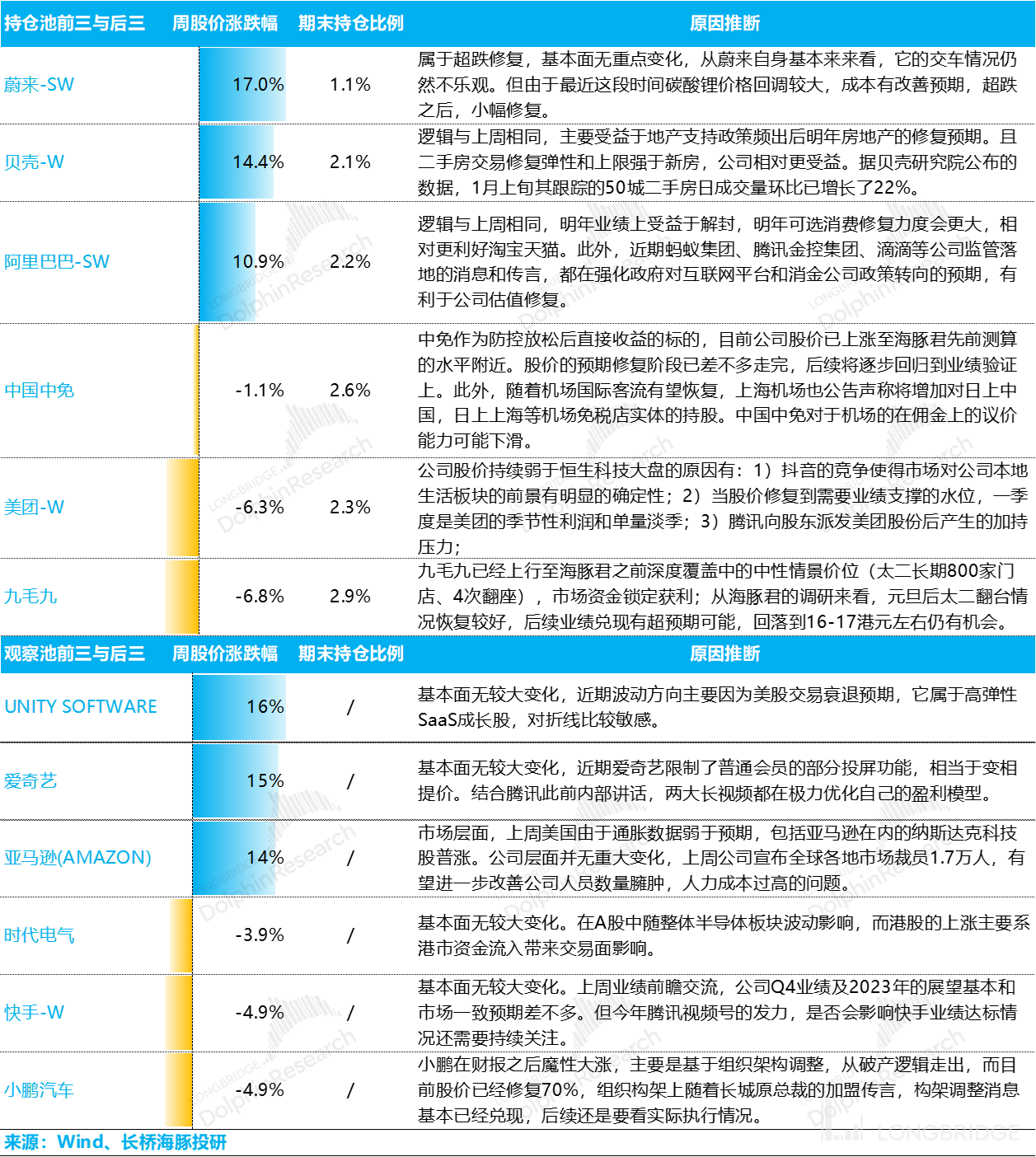

Regarding companies with large increases or decreases, the Dolphin Analyst has compiled the driving factors as follows for your reference:

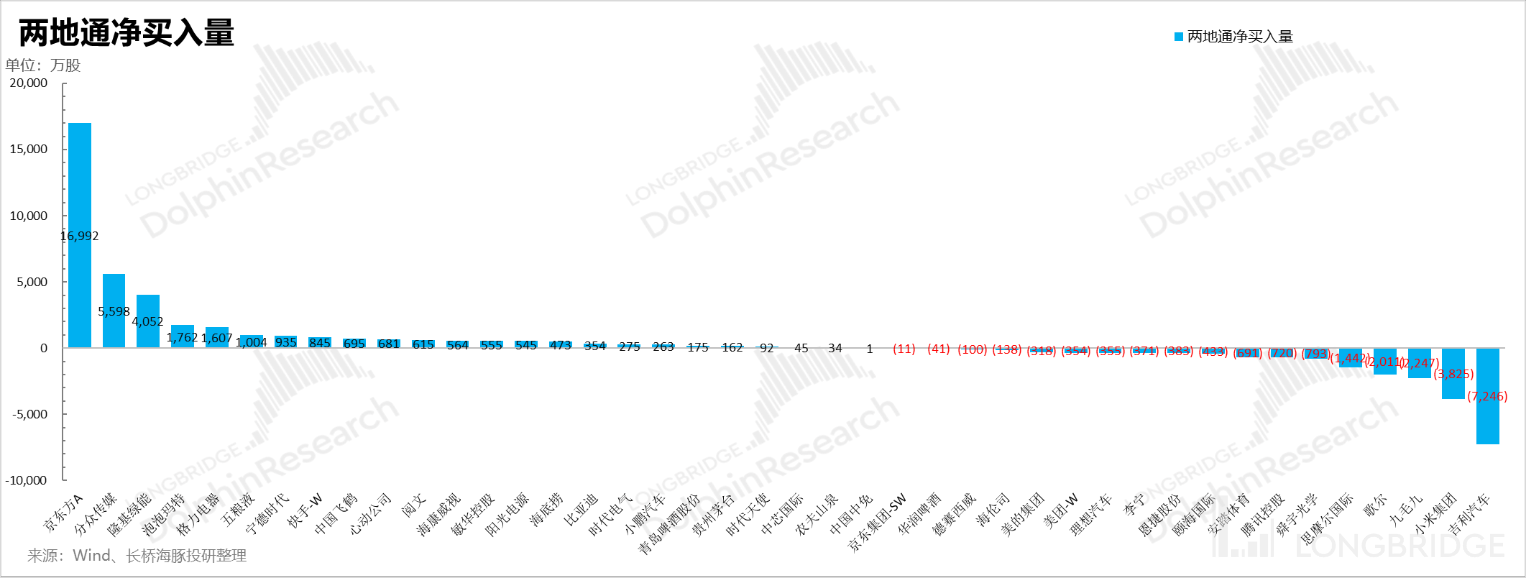

From the perspective of the northward and southward fund flows of individual stocks in Dolphin Analyst's pool, it is also evident that the stock prices of Hong Kong companies covered by Dolphin Analyst fell last week, while their characteristics were northward buying and undervalued +A consumption leading stocks.

From the perspective of the northward and southward fund flows of individual stocks in Dolphin Analyst's pool, it is also evident that the stock prices of Hong Kong companies covered by Dolphin Analyst fell last week, while their characteristics were northward buying and undervalued +A consumption leading stocks.

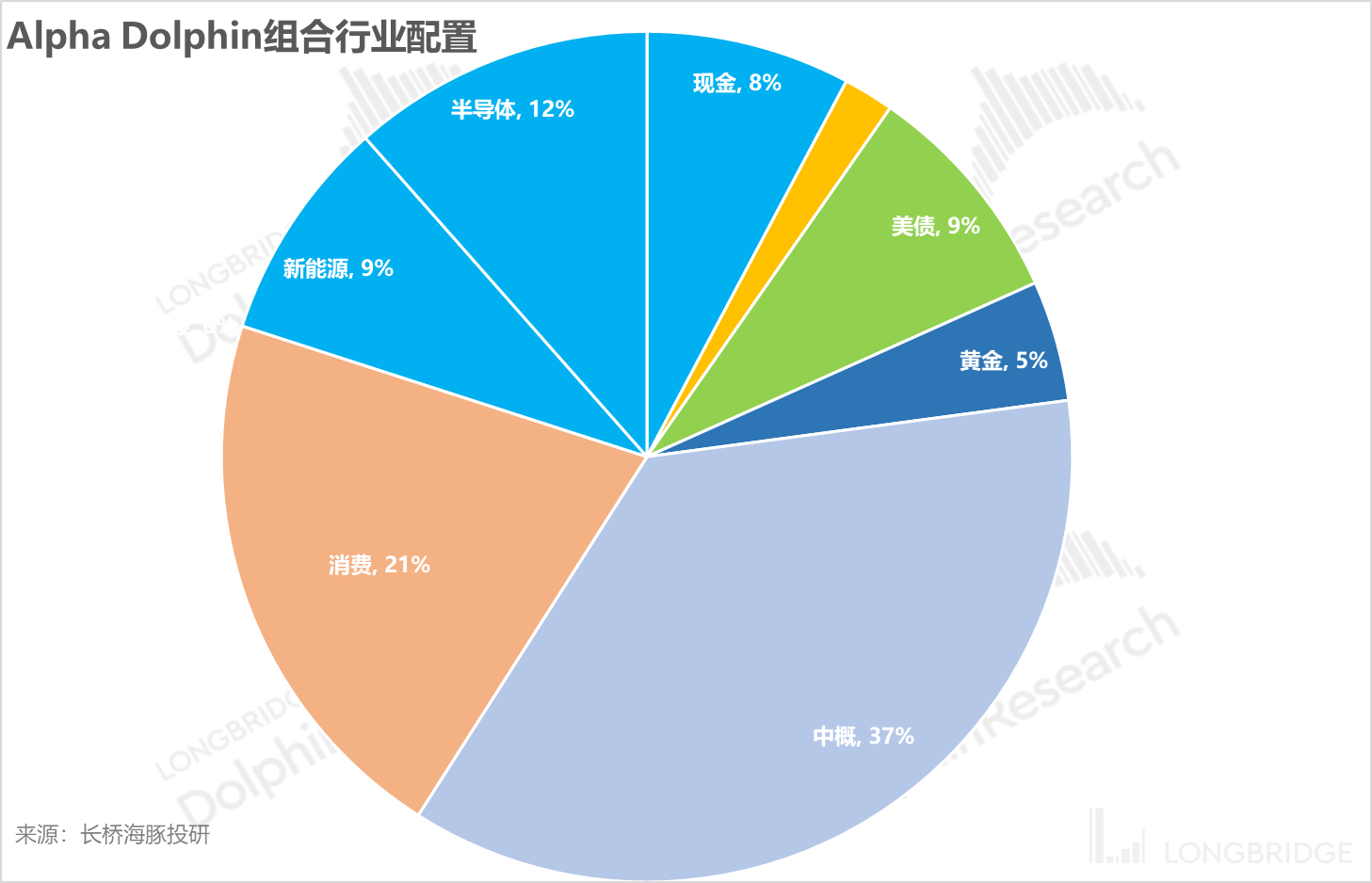

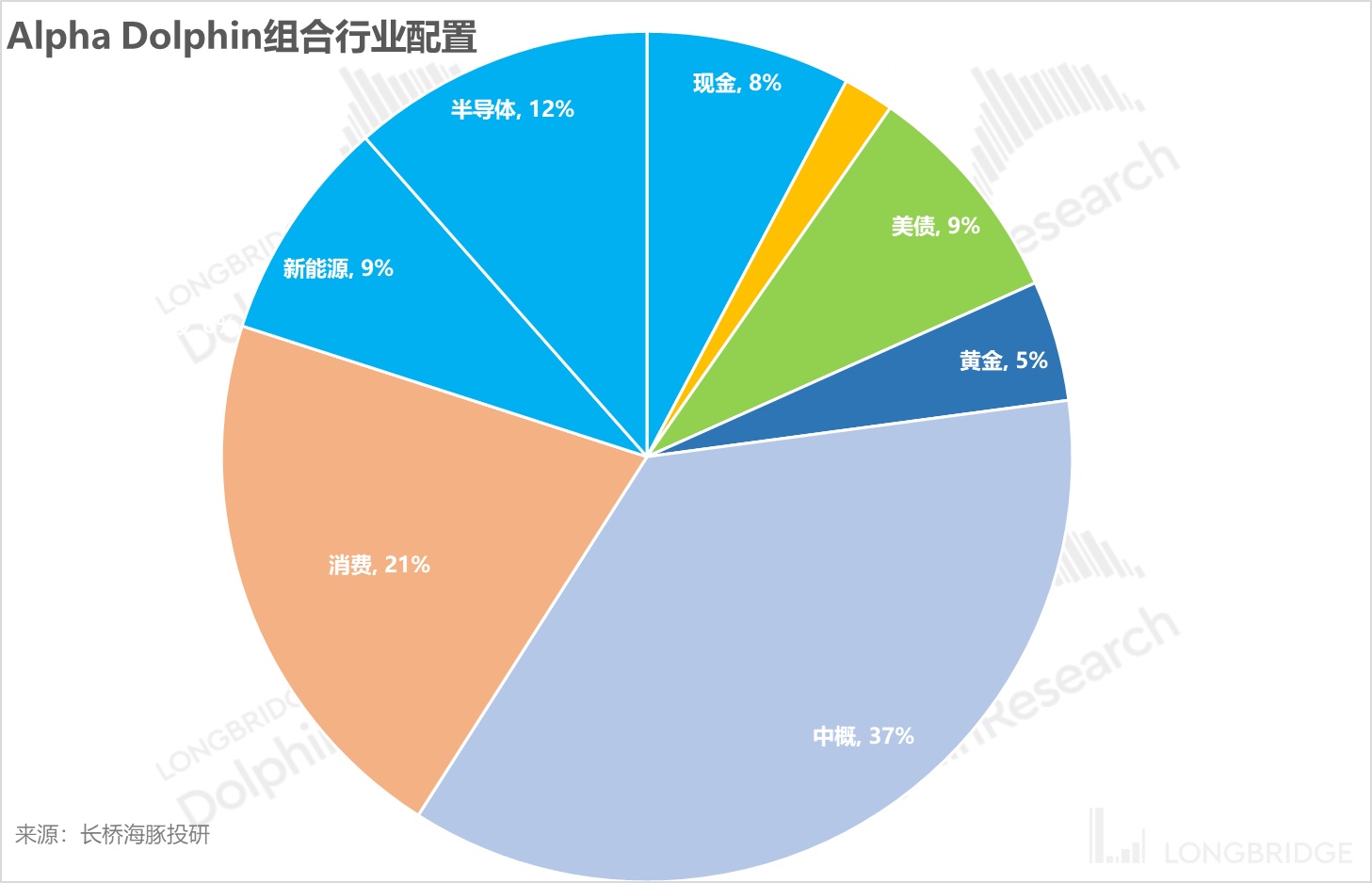

VI. Distribution of composite assets

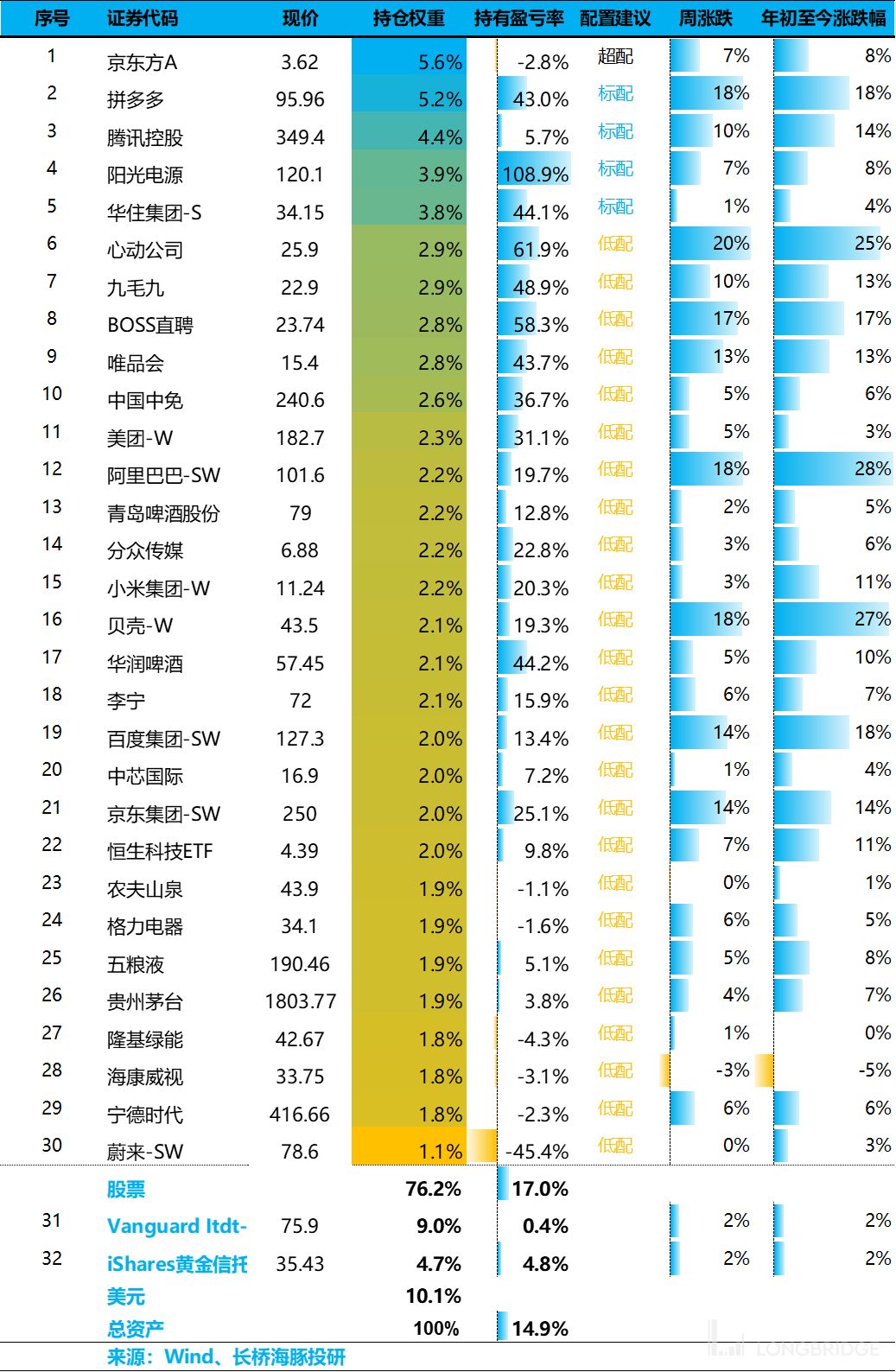

After Didi's inclusion in the portfolio, the Alpha Dolphin portfolio now holds a total of 31 stocks/indexes, with one being over-allocated, four being standard, and 26 being under-allocated stocks. As of the end of last week, the asset allocation and equity asset holdings of the Alpha Dolphin portfolio were distributed as follows:

As of the end of last week, the distribution of the major assets of the Alpha Dolphin portfolio was as follows:

VII. Focus of this week's events:

Among the companies that Dolphin Analyst is focusing on this week, Netflix and New Oriental have released financial reports, and the main points of focus are as follows:

< End of the text >

Please refer to the following Longbridge investment research portfolio weekly reports:

"Has the Spring for Chinese Assets Truly Arrived Behind Alibaba's Soaring Stock Prices?"

"Although the US stock market didn't have a red New Year, the Performance Hammer Is Just Around the Corner?"

"Scrutinizing the Root Cause of the Stagnating US Stock Market"

"Why Is the US Federal Reserve So Inflexible Despite the CPI's Decline?" 《Is it really easy to eliminate service inflation? Be careful of market overcorrection》

《Has Hong Kong stocks finally got the support? Independent market still has a way to go》

《The darkest moment before the dawn: mindset lies in darkness or dawn》

《 US stocks "sent back" to reality, how long can emerging markets bounce?》

《Global valuation repair? There are still hurdles for performance inspection》

《The violent hike of Chinese assets, why is there a world of difference between China and the US》

《Amazon, Google, Microsoft giant star fall? US stock "meteor shower" still needs to happen》

《Behind the policy shift expectations: is the "strong dollar section" GDP growth unreliable?》

《The moment of testing "determination" has come again: the southern acquisition vs the northern run》

《Slow down rate hikes? The American dream is shattered once again》

《 Rethinking a "Iron-blooded" Federal Reserve》

《 Tragic second quarter: "Eagle sound" is loud, but it is difficult to cross the collective river》 《Fall to Doubt about Life, Is There Still Hope for Reversal?》

《 Violent Hammer Inflation by the US Federal Reserve, Consumer Opportunities Comes in China?》

《 Global Dropped Significantly again, Labor Shortage Is the Root of US Economic Problems?

《The US Federal Reserve Becomes the Number One Bear, the Global Markets Crashes》

《USA to Left, China Swings Right, and the Cost Effectiveness of US Assets Returns》

《Too Slow to Lay Off Employees, USA Has to Continue to Be "Down"》

《US Stocks' funeral made grandly: Recession is a good thing, the most powerful rate hike is bearish》

《The Rate Hike Enters the Second Half, the “Performance Thunder” Opens》

《The Epidemic to Strike Back, the United States to Recede, and the Funds to Flip》

[《Current Chinese Assets: "No news is good news" for US Stocks》](https://longbridgeapp.com/topics/3035475? channel=t3035475&invite-code=032064)

“Has America really declined in the midst of growth?”

“Will America experience recession or stagflation in 2023?”

“Amidst American oil inflation, can China strengthen the electric car industry?”

“As the Fed speeds up rate hikes, will China investment opportunities emerge?”

“As US stock inflation explodes again, how far can we expect the rebound to last?”

“A down-to-earth approach to investing: Dolphin's portfolio is now open for subscription”

Risk Disclosure and Disclaimer for this article: Disclaimer and General Disclosure of Dolphin Research and Investment